Circle (Trans): New Bill Nears Passage; Arc to Drive Future Growth ---

Dolphin Research compiled the FY25Q4 earnings call transcript for $Circle(CRCL.US). For the earnings take, see 'Circle: Beating the bears with results — can the No.1 stablecoin stock stay stable?'.

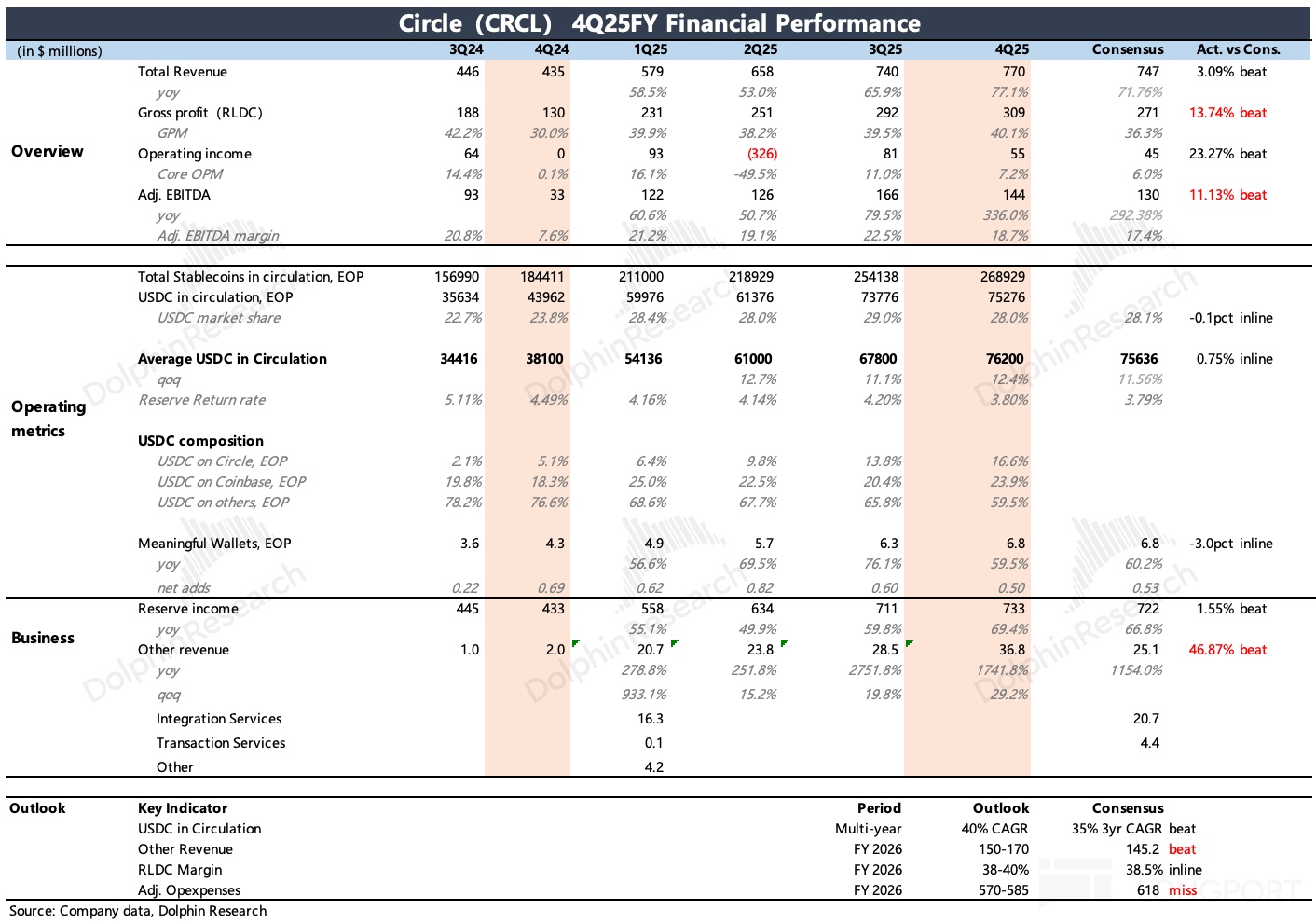

I. Key financial recap

II. Earnings call details

2.1 Executive highlights

1. Macro outlook

Convergence of tech shifts: we are at the very beginning of a deep transformation of the global economic system, driven by blockchain/stablecoins, accelerating tech, and AI converging. The world will have tens of billions, if not hundreds of billions, of AI agents that interact over the internet and perform economic functions. Rise of the internet of value: we are moving from the internet of information to the internet of value. Blockchain platforms and an internet-native money layer centered on stablecoins have emerged.

2. Platform progress and product updates

Platform expansion:

- Arc blockchain network: testnet is live with 100+ leading firms across banking and capital markets participating. Testnet transaction value exceeded $166 mn, with Avg. settlement time of half a second, and mainnet is targeted for 2026.

- New products: beta launches include Stable FX (on-chain FX) and xReserve (extending USDC across multi-chain ecosystems). These broaden utility and interoperability of the stablecoin stack.

- Interoperability infra (CCTP): CCTP volume grew 3.7x YoY to over $41 bn in Q4. Its share of cross-chain bridge volume surpassed 50% and reached 62% in Jan, and with the acquisition of Interop Labs, Circle is building new features to help asset issuers leverage this infra.

Digital assets and services:

- USDC: supported on 30+ blockchain networks. After Visa analytics de-noising, USDC's share of real-economy activity rose from 39% in Q3 to nearly 50% in Q4, underscoring growing utility.

- EURC: Q4 reached €310 mn, up 3.8x YoY, and had risen to €389 mn as of Feb 20. It is the largest regulated euro stablecoin.

- USYC (tokenized money market fund): AUM was approx. $1.5 bn at year-end and has continued to grow past $1.7 bn. Demand is driven by use as collateral at exchanges.

Applications:

Circle Payments Network (CPN): registered FIs rose from 29 in Q3 to 55. As of Feb 20, annualized TPV was $5.7 bn, up approx. 68% vs. the Q3 print, and service markets expanded to 14 across the Americas, EMEA, and APAC. The footprint is set to add 11 new markets in the coming months, supporting broader adoption and flow. This underpins the build-out of institutional-grade rails.

Stable FX: a beta is live in production, enabling 24/7 capital-efficient on-chain FX conversion. This is designed to reduce frictions and settlement costs.

AI strategy — AI as a core driver: AI is becoming a major driver of Circle's platform and USDC adoption. This is central to agent-based commerce and autonomy.

Agentic Payments: on testnet we launched Circle Gateway, enabling AI agents to autonomously execute cross-chain USDC transactions programmatically at ultra-low cost (one-thousandth of a cent per transaction). Circle believes this capability is unique globally. Empowering AI developers: we are investing in tools and infra for developers building AI agents, helping them ship faster and smarter. The goal is to standardize primitives for payments and custody. Internal AI applications: AI is becoming foundational across all Circle functions, embedded in ops, product, and engineering. This has meaningfully accelerated product development.

Competitive position and network effects

- Durable network effects: the stablecoin market is dominated by two major issuers, reflecting high barriers to entry. Circle's edge is built on trust, compliance, and transparency, earning the confidence of FIs, enterprises, and end users.

- Unmatched liquidity: $75 bn USDC in circulation and $163 bn of mint and redeem in Q4 prove Circle's unmatched ability to create and redeem digital dollars at scale via the global banking system.

- Neutral infra: being market-neutral and not competing with customers or partners is key to Circle's success. This neutrality supports broad ecosystem alignment.

Financial guidance and outlook

Guidance philosophy: we do not provide detailed quarterly or comprehensive financial guidance, but guide to select metrics to help investors understand trajectory. We will update guidance if results may materially deviate. FY26 guidance:

- Other revenue: expected at $150–170 mn. This reflects early monetization across products.

- RLDC margin (revenue less distribution costs): expected at 38–40%. This underscores unit economics discipline.

- Adj. OPEx: expected at $570–585 mn, reflecting continued investment in platform, capabilities, and global partnerships. The definition now excludes SBC-related payroll taxes and certain one-offs.

Long-term outlook: USDC is expected to grow at 40% CAGR across the cycle. This is anchored by adoption in real-economy use cases.

2.2 Q&A

Q: On the agent economy timeline — how does it unfold across trading liquidity, payments, and lending, and how do you ensure USDC is central? Can Arc support this technically?

A: Arc's core design centers on agentic economic activity, aligned with our early vision of programmable, machine-mediated money. We see the convergence happening, and recent Claude/OpenClaw developments unlocked a step-change in agent capabilities, with developers realizing agents need reliable, low-cost, trusted media of exchange. Virtually all emerging AI payment infra and agent-to-agent activity is happening on-chain using USDC, which is very encouraging. In terms of pace, this could be an 'inflection moment' with agents consuming work from each other, collaborating, and distributing work to humans already emerging. In recent weeks we have seen agent marketplaces (agents hiring human workers with USDC) and agent job boards (agents paying each other with USDC). As enterprises and startups build around economic activity, they naturally choose stablecoins and blockchains.

Arc is built for this: its validation and consensus models scale, and its economic model drives transaction costs on high-performance lanes to one-thousandth of a cent. Last week on testnet, Circle Gateway enabled autonomous agents to hold balances and spend across networks, including Arc, achieving one-thousandth of a cent per transaction and sub-second value transfer. We are building these primitives and tools at the OS and infra layers and actively marketing to agents that want to build. Looking ahead to a world with tens or hundreds of billions of agents, money velocity will be orders of magnitude higher than today's systems. Circle is building new economic infra and is optimistic about playing a key role in the fusion of AI and stable blockchains. We see a large opportunity to standardize agentic payments.

Q: What are the current thoughts on an Arc token, and when might you decide on launching one?

A: We continue to explore an Arc token, and it is a valuable avenue of exploration. We are deepening our understanding of how a token could play key roles on Arc, including stakeholder incentives, governance, security, and utility. We do not have a timeline yet as we remain in the exploration phase. As noted, Arc is making strong progress toward mainnet, and we are excited to have leading firms operate infra, deploy apps, and support broad use cases for asset issuers and AI agents. We are pleased with progress and will share more when available. Any decision will prioritize prudence and market integrity.

Q: On regulation, GENIUS has been in effect for several quarters — what direct progress have you seen? Also, views on CLARITY — stablecoins seem central to the debate.

A: GENIUS is a clear tailwind, establishing legal foundations for large institutions to enter. We have seen SEC and CFTC guidance clarifying how GENIUS-compliant stablecoins can be used as collateral in CFTC markets. SEC's recent move to allow stablecoins as margin or offsets in broker-dealer trading is a major breakthrough for capital markets usage. Globally, banks, payment firms, and tech companies want stablecoins embedded in product strategy. This is influencing Intl markets as regulators recognize GENIUS-compliant stablecoins as 'good stablecoins' their markets can permit, which is highly favorable. We see it as very positive, and with the act in force and certain OCC licenses being issued, the positive impact should continue.

On CLARITY, it is close to a final outcome, and recent reporting appears accurate, namely that the crypto industry and banks are working with the White House on compromise language around rewards for holding or using stablecoins. We think all parties want this resolved, which is significant for banks, capital markets, asset managers, and crypto. We are cautiously optimistic, though Washington can be unpredictable, and if CLARITY can pass on a bipartisan basis, it would be another major breakthrough for building in this space. It would be very, very consequential for market development and broader blockchain application. We see potential for durable policy clarity.

Q: Long-term evolution of Arc and CCTP — do they become asset-agnostic platforms or broad platforms for tokenizing assets like equities? What is the long-term vision?

A: Absolutely. Arc's core idea is a distributed economic OS operated by leading financial infra firms including Circle, supporting prudent financial and economic activity and providing foundations for real-economy build-out on the internet. On this secure and reliable base, we first aim to build the most capital-efficient digital dollar liquidity, combining USDC with Arc tech to create the fastest, most capital-efficient digital dollar model globally. This should reduce cost of value transfer. Second, we aim to be the liquidity and distribution hub for other asset issuers, building on CCTP's massive distribution. Any issuer — tokenized equities, funds, bank deposits — could issue on Arc and then unlock liquidity and distribution on other chains.

Issuers need safe, liquid, and distributable paths, and CCTP in Jan captured over 60% of cross-chain flow. With new Arc tech, we believe we can activate these highways for any asset issuer, scaling both issuance and settlement. In short, the long-term vision is a general OS for internet economic activity, well-suited for today's demand to build cost-effective AI transactions and tokenized apps. Arc and its interoperability infra fit this environment.

Q: On Agentic AI and given crypto stocks and token markets, will agentic AI and its payment functions be a broad positive for the industry?

A: It is one of the most exciting convergence points. If developers are building agents that can contract with other agents or humans, handle disputes, execute contracts, and move money, or form organizations of humans and AI agents needing underlying governance, blockchain infra is the foundation. We need cryptographic proofs as the only way to trust agent activities, data, and transactions. We are seeing this in developer activity and Arc engagement, with AI-first founders recognizing the utility of this backplane. Looking back at platform transitions — just as mobile rose alongside cloud — we believe starting in 2026 AI platforms and blockchain OS platforms will tightly pair for those building the AI-driven economic system. This pairing should catalyze adoption.

Q: CPN onboarding and flows — initial use cases, stickiness, growth per FI? Also, for Agentic Commerce, how should investors think about the impact on Circle's operating and financial model?

A: Since CPN's launch in Jun last year, we iterated the product and commercial model several times, and the network now has 55 FIs with strong QoQ growth. Interest from prospective members remains robust and is broadening in scale. On flows, annualized TPV was approx. $5.7 bn as of last Fri, up 68% since our last update. We see more large firms joining that can support larger flows, which is a key objective for scale and resilience. From a product perspective, we want to improve onboarding and implementation efficiency, and many FIs are new to blockchain and stablecoins. We need to simplify processes and ensure high-demand lanes have solid participants and redundancy.

Use cases are led by B2B cross-border merchant settlement and remittances between emerging markets and between developed and emerging markets. We are pleased with progress, investing heavily in the product, and have ambitious goals. Once scale is sufficient, we will begin monetization, and partners are already realizing benefits. This should enhance network economics. On agentic impact, it is a major new demand driver for stablecoin network utility, with agents as end users driving transaction volume and balances and expanding into non-crypto-native commerce scenarios. It also helps us accelerate entry into other software institutions whose products need to be consumable by AI agents.

These may require different pricing and economic models where our agentic payments standards can help. It can fundamentally drive Arc traffic and growth, and over time Arc can create new transaction-based revenue streams. While early, we think the scale could be significant, and what we have seen over the past 3–4 weeks has been eye-opening. We are excited our products and standards are ready for what appears to be an inflection moment. The runway for adoption looks strong.

Q: On prediction markets and the Polymarket partnership — why is USDC so critical to this fast-growing area? What should we expect over coming quarters and years?

A: when we think about killer apps for stablecoin networks, prediction markets are absolutely one of them. We invested early in the on-chain ecosystem, so USDC has been systemic and critical to many apps built in recent years, including Polymarket. Through close collaboration we helped them improve customer experience with tech and deliver more seamless services. For prediction markets, users need to move fast, and as information markets they require rapid capital movement. Stablecoins let end users globally post collateral and settle at internet speed, and they can connect from different wallets and venues. This opens global access and provides solid infra for firms like Polymarket to store funds and present balances to users. USDC is already used as the funding method across multiple prediction markets, supporting offerings on Coinbase, Kraken, and Robinhood.

We aim to partner with leaders so the best digital dollar is used for settlement or collateral in these scenarios. Partnering with and co-building alongside leading prediction markets globally is a very positive outcome. Polymarket's growth and success are remarkable, and the markets are still early. We see durable growth ahead as products mature.

Q: USDC on-platform share rose to 17% in Q4. Into FY26 and new initiatives, what is a reasonable range for this share, and what relationships or initiatives will be the biggest drivers of incremental on-platform USDC over the next 12–24 months?

A: We are very pleased with 5x YoY growth in on-platform USDC. We are continuously building infra products that create value for holding and using USDC, spanning wallet products, Circle Gateway, Circle Mint, and many other developer touchpoints. The core premise is that more large institutions, both FIs and others, will want to build on our infra. For example, Arc is a driver as our infra will integrate well with Mint, wallets, and Gateway, jointly enabling more apps, flows, and balances to use Circle tech, which supports growth in on-platform USDC. At a macro level, it is about continuing to build institutional partnerships with diverse firms. We do not guide to the share, but the direction is clear.

We will keep focusing on building infra people want to build on. Also noteworthy, we have received conditional approval for Circle National Trust Bank (the first national digital currency bank), which matters for USDC and its reserves and for how we work with the OCC under GENIUS in the future. This strengthens our custody infra for market participants, and as we build it into a fiduciary, safe, and operational system with trust bank protections, we think it will be incremental to platform capabilities over the coming quarters. Our unmatched global banking and liquidity infra in stablecoins is second to none, and the broad network of users, developers, and enterprises building on USDC only makes any new large enterprise more inclined to choose USDC. We are positioned as neutral market infra and do not compete with enterprises and developers building on our stack for their customers. This neutrality supports adoption across sectors.

Q: Two questions. First, can you break down FY26 guidance for other revenue of $150–170 mn and drivers vs. FY25? Second, as Arc mainnet nears, can you outline the post-mainnet release plan at a high level? Also, could elements of Arc and CPN converge to deliver more value to customers and new users?

A: For other revenue, Q4 was $36.8 mn, including approx. $25 mn from subscriptions and services and $12 mn from transaction revenue. Within subscriptions and services, the largest portion comes from blockchain network partnership revenue, which includes upfront and recurring components. Upfront depends on the number of integrations and partners and may vary by quarter, while base recurring grows as more partners go live and we execute a strong pipeline. It also includes USYC tokenized MMF management fees, currently small but with potential. Transaction revenue has multiple components, such as fees from value-added products like CCTP fast transfers and, in future, fees from Circle Payments Network. We also run validator infra, and this quarter revenue was unusually high due to Canton Coin listing and share price moves. We do not guide to the granular mix, and most of these products and services only began monetizing in Q4'24 and Q1'25. Given this line is only one year old, we are very pleased with the $110 mn full-year outcome.

On Arc mainnet, progress is strong, the testnet infra is robust, and usage, transactions, and developer activity are growing well. Transitioning from testnet to mainnet involves several key considerations, starting with technical delivery to ensure certain capabilities are available at launch for institutional tokenization and agent activity. Second, ARC Phase 1 will use a proof-of-authority validator model, introducing an initial cohort of strategic partners to operate Arc network infra. World-class financial infra firms running with us are critical to trust, reliability, and future governance. Third, we are working closely across the digital asset ecosystem on enterprise tools, custody, wallets, and exchanges to ensure everyone is day-one ready. This includes deep integration with Circle's existing stack, such that USDC liquidity at mainnet will be the best globally and most capital-efficient.

We are collaborating with leading firms in the testnet cohort to ensure readiness across capital markets, payments, FX, and agent economy use cases. On Arc-CPN convergence, Arc will be key infra for CPN, providing speed, reliability, prudence, safety, and efficiency, simplifying flows by enabling usage with stablecoin balances and embedding best-in-class interoperability. If CPN endpoints need to interact with wallets on other networks, Arc allows members to seamlessly switch. Arc will be CPN's backplane, and Stable FX as a native Arc app will be the FX backplane supporting Arc transactions. By onboarding other stablecoins and market makers to Stable FX, we can offer real-time atomic cross-currency liquidity, speeding settlement and settlement assurance, and reducing capital needs. Arc, Stable FX, CPN, and Circle Mint will work in concert.

Q: On distribution costs, Coinbase is well-known — can you discuss non-Coinbase distribution costs and negotiations, as those have been quite stable for several quarters?

A: We are in a very favorable position because USDC has strong network effects. If you are building a product or service and want a compliant, liquid, available, and interoperable digital dollar, USDC is the default choice. We see many products being built and launched using USDC and connecting to our stablecoin network, which drives demand and liquidity. This is valuable to those products as they are tapping a globally available, near-free dollar payment system. As this organic growth occurs, a developer- and institution-led flywheel forms, driving USDC and institutional adoption, and we do not need incentive deals or other arrangements for this. We are disciplined on incentive relationships and only engage where it is rational and where we see partners can drive meaningful growth, which helps us maintain strong unit economics.

Additionally, USDC growth brought by distribution partners — some of which is incentivized — strengthens the underlying network effects of USDC. This makes other market participants more inclined to independently build and use USDC and offer USDC-based products and services to customers, and any distribution relationship strengthens USDC. A material portion of USDC adoption is not influenced by any distribution or incentive deals, which is how base networks achieve network-effect advantage. This supports RLDC margins and underlying economics.

Q: On the AI Hackathon — to make Circle core to these emerging payment networks, what are the to-dos? Versus Ethereum and other crypto solutions, what are pros/cons, and how do you establish position in an agent economy?

A: Over the past 4–5 years Circle has invested heavily to ensure our stablecoin network and USDC distribution, liquidity, and settlement pipes are deployed across as many chains as possible, now covering 30+ networks. This breadth is critical for developer choice. When developers build, agents may anchor on Ethereum, Solana, Arc, or new chains to come, and blockchain networks as economic OS are still early and scaling to AI-required transaction speeds. We operate across these networks and co-authored or contributed to nearly all key agent payment standards, such as x402 and ERC-8004. Recent stats show 99% of agent payments use USDC, and through network coverage, standards participation, and multi-modal deployment, we have a first-mover advantage. We also ensure all our APIs and protocols are exposed as skill libraries to agent coding systems and as MCP servers so AI dev tools integrate seamlessly.

These investments are paying off now. Many companies realize SaaS may sell API access to AI agents rather than end-user seats, and everyone is thinking about marketing to AI agent populations. We seized the moment to host the first Hackathon allowing AI agents to compete and vote, which is powerful marketing that gives agents deep familiarity with USDC. There will be more such initiatives to drive adoption. On the tech side, we believe Arc will be very attractive high-throughput infra given its USDC-centric capabilities, capital efficiency, interoperability, and transaction cost efficiency, and we will keep investing here. This should support agent commerce at scale.

Risk disclosure and statements:Dolphin Research disclaimer and general disclosure