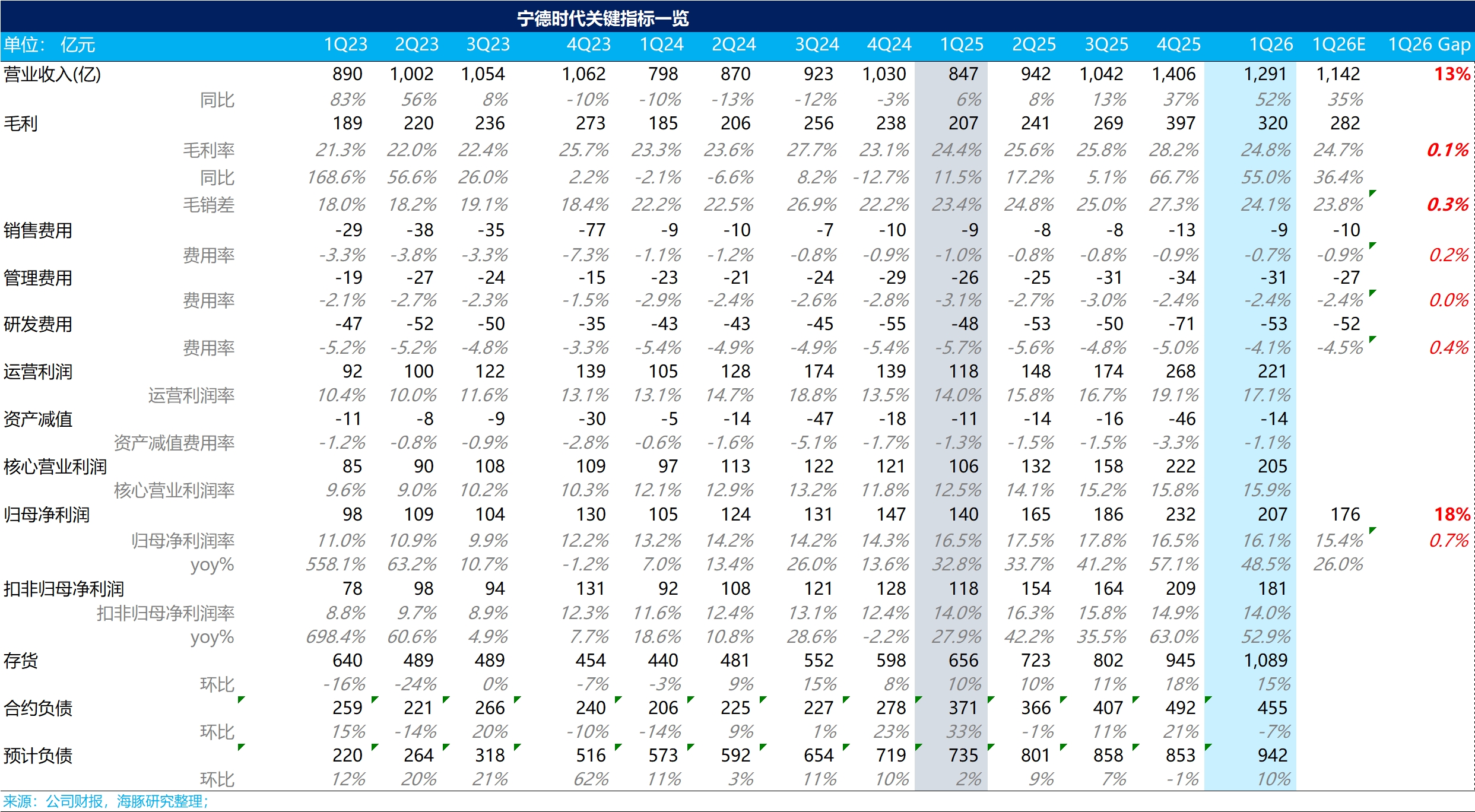

CATL 1Q26 First Take: CATL again demonstrated strong earnings resilience in 1Q26. Despite raw-material inflation and elevated expectations, both revenue and net profit beat. Specifically:

① Revenue: Volume and price both rose, well ahead of estimates. 1Q26 revenue reached RMB 129.1bn (+52% YoY), beating the street at RMB 114.2bn. The upside was driven by sustained shipment growth and partial cost pass-through that lifted ASPs amid upstream price hikes.

② Profitability: resilient, GPM in line. 1Q26 GPM was 24.8%, down from the Q4 peak when capacity was fully utilized. Given the seasonal softness and lithium carbonate averaging near RMB 180k/t, this margin level was resilient and broadly in line with market expectations.

③ Bottom line: beat as well. 1Q26 net profit came in at RMB 20.7bn (~+49% YoY), above market expectations. Attributable NPM only edged down QoQ to 16.1%, while ex-non-recurring attributable net profit was RMB 16.4bn (+53% YoY).

The earnings beat was driven by volume and ASP uplift, tighter control of R&D and other opex, and lower impairment losses QoQ. This print eased prior concerns that rising lithium carbonate prices would erode margins.$CATL(300750.SZ) $CATL(03750.HK)

The copyright of this article belongs to the original author/organization.

The views expressed herein are solely those of the author and do not reflect the stance of the platform. The content is intended for investment reference purposes only and shall not be considered as investment advice. Please contact us if you have any questions or suggestions regarding the content services provided by the platform.