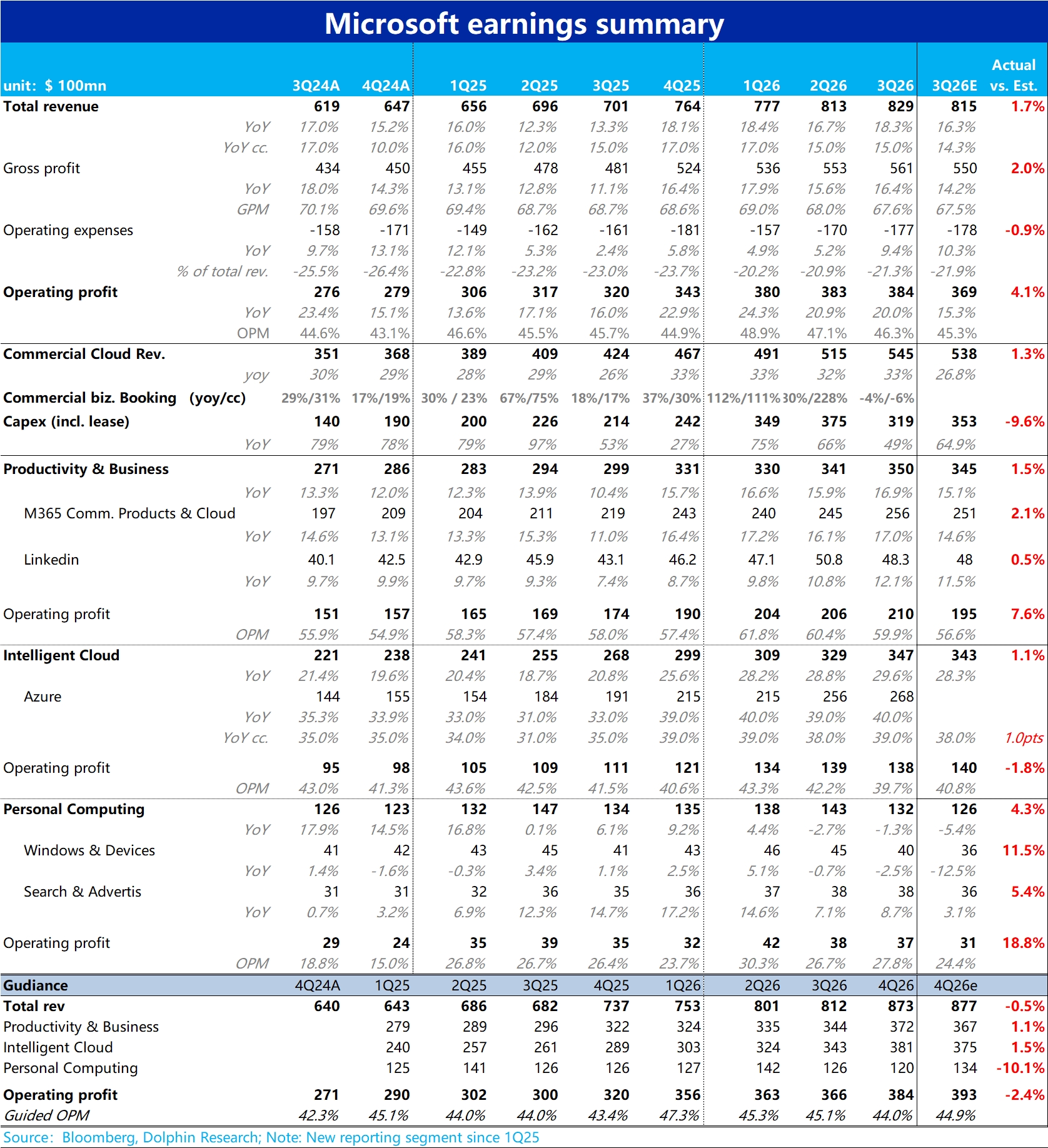

MSFT F3Q26 First Take: Results once again highlight a steady profile, with most key metrics slightly beating expectations but by modest margins. Ex-FX tailwinds, revenue and profit growth momentum was broadly in line with last quarter. Azure grew 39% at cc, a slight acceleration, but it lagged the sharper re-acceleration seen at Google Cloud and AWS.

Specifically:

1) Total revenue rose 15% ex-FX, with growth flat vs. last quarter. OP grew 20%, also flat vs. last quarter, but ex-FX profit growth slowed to 16% this quarter vs. 19% last quarter. Overall delivery was stable.

2) Azure grew 39% at cc, up 100bps QoQ and roughly in line with the Street. While not matching competitors' strong acceleration, it shows signs of re-acceleration. Recent developments suggest OpenAI order pullbacks weighed on growth.

3) The other two segments also came in slightly better than expected. Productivity & Business Processes (PBP) revenue grew 17% at cc, up 100bps and steadily improving. More Personal Computing (MPC) declined 1%, much better than the Street's -5%.

4) On other metrics, AI ARR reached 37 bn, ~150% above Amazon's disclosed 15 bn, keeping MSFT in the lead by absolute AI scale. However, with the OpenAI partnership further downgraded, new enterprise bookings fell 4% YoY (ex-OAI +7%).

Similarly, RPO was 627 bn, up 99% YoY, but only +26% ex-OpenAI orders. Based on Dolphin Research's preliminary estimate, the implied OAI order balance fell by about 5 bn QoQ this quarter.

5) Despite subdued top-line growth, profit delivery was solid, driven by upside in PBP and MPC. Cloud OP margin came in at 39.7%, below expectations and down ~180bps YoY, reflecting capex investment and revenue mix shifts.

6) Capex was 31.9 bn, down over 5 bn QoQ and below expectations, likely reflecting OAI order adjustments and the corresponding pacing. The company guided CY26 total capex to 190 bn, implying >50 bn per quarter over the next three quarters, potentially surpassing Amazon as the most aggressive CSP spender.

7) For next quarter, Azure revenue is guided to grow 39–40% at cc, steady but not particularly surprising. Overall revenue guidance roughly matches expectations (aside from the usual conservatism in MPC), but the profit guide is slightly light; the implied OPM midpoint is 44%, below expectations and 44.9% a year ago, suggesting greater margin pressure next quarter.$Microsoft(MSFT.US)

The copyright of this article belongs to the original author/organization.

The views expressed herein are solely those of the author and do not reflect the stance of the platform. The content is intended for investment reference purposes only and shall not be considered as investment advice. Please contact us if you have any questions or suggestions regarding the content services provided by the platform.