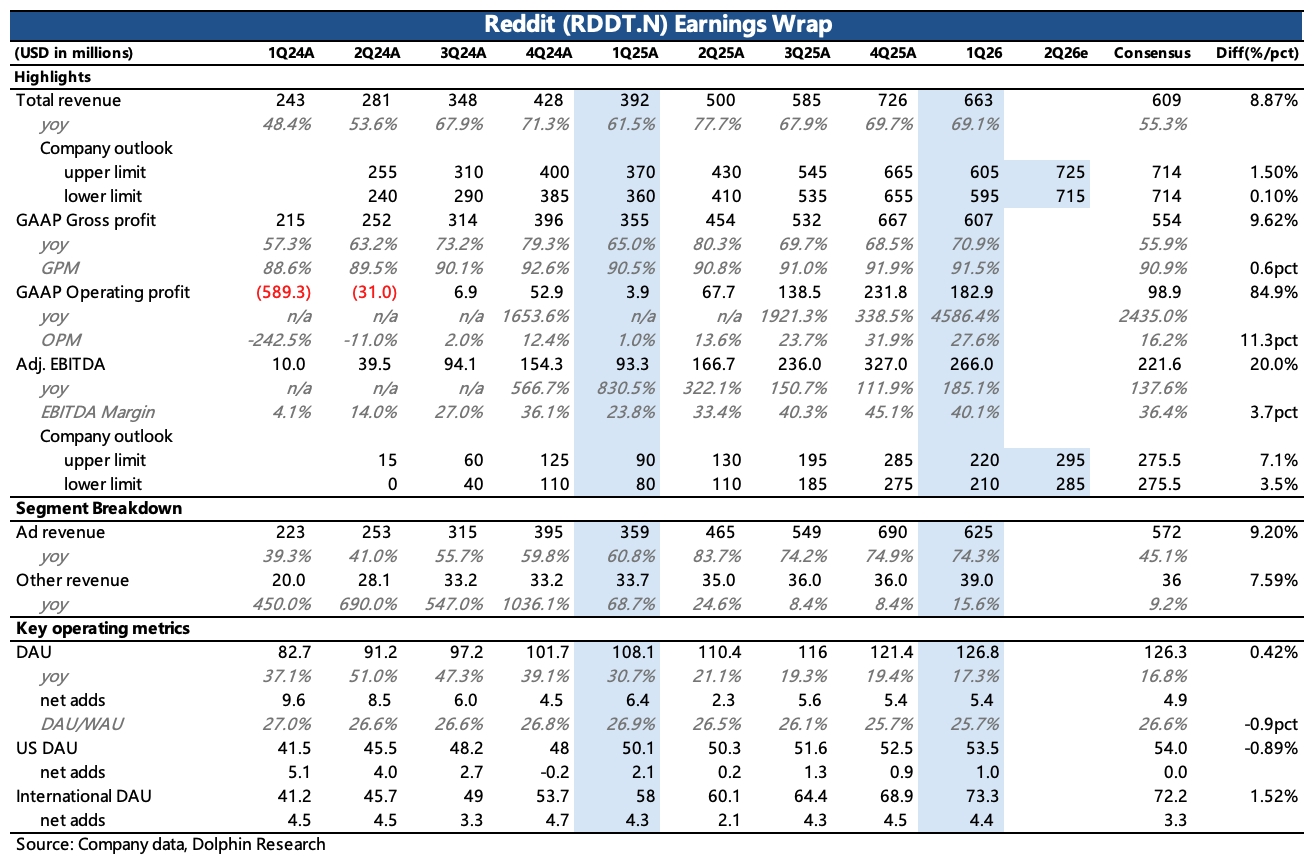

Reddit 1Q26 Quick Take: Q1 delivered solid results. As a key data source for AI with authentic, human content, Reddit is benefiting from referral traffic from Google and other gateways. Monetization remains early, with performance ads ramping alongside brand, implying a steep slope for revenue growth and margin expansion.

Ahead of the print, Cleveland's checks indicated that macro volatility led advertisers since late Mar to cut brand budgets and shift spend to higher-ROI large platforms. That reset growth expectations for Reddit and put the stock under sustained pressure in recent sessions, helping digest a premium multiple.

With growth showing no clear slowdown, a clean Q1 print should alleviate some market concerns. That said, there were blemishes: US user growth remains sluggish, and the Q2 revenue guide implies growth slowing to ~45% from 69% in Q1, which may indirectly corroborate the above channel checks.

Management tends to guide conservatively. With the automated ad-buying tool 'Reddit Max' slated for a broad Q2 rollout, Reddit could again outgrow guidance. $Reddit(RDDT.US)

The copyright of this article belongs to the original author/organization.

The views expressed herein are solely those of the author and do not reflect the stance of the platform. The content is intended for investment reference purposes only and shall not be considered as investment advice. Please contact us if you have any questions or suggestions regarding the content services provided by the platform.