It's actually quite reasonable.

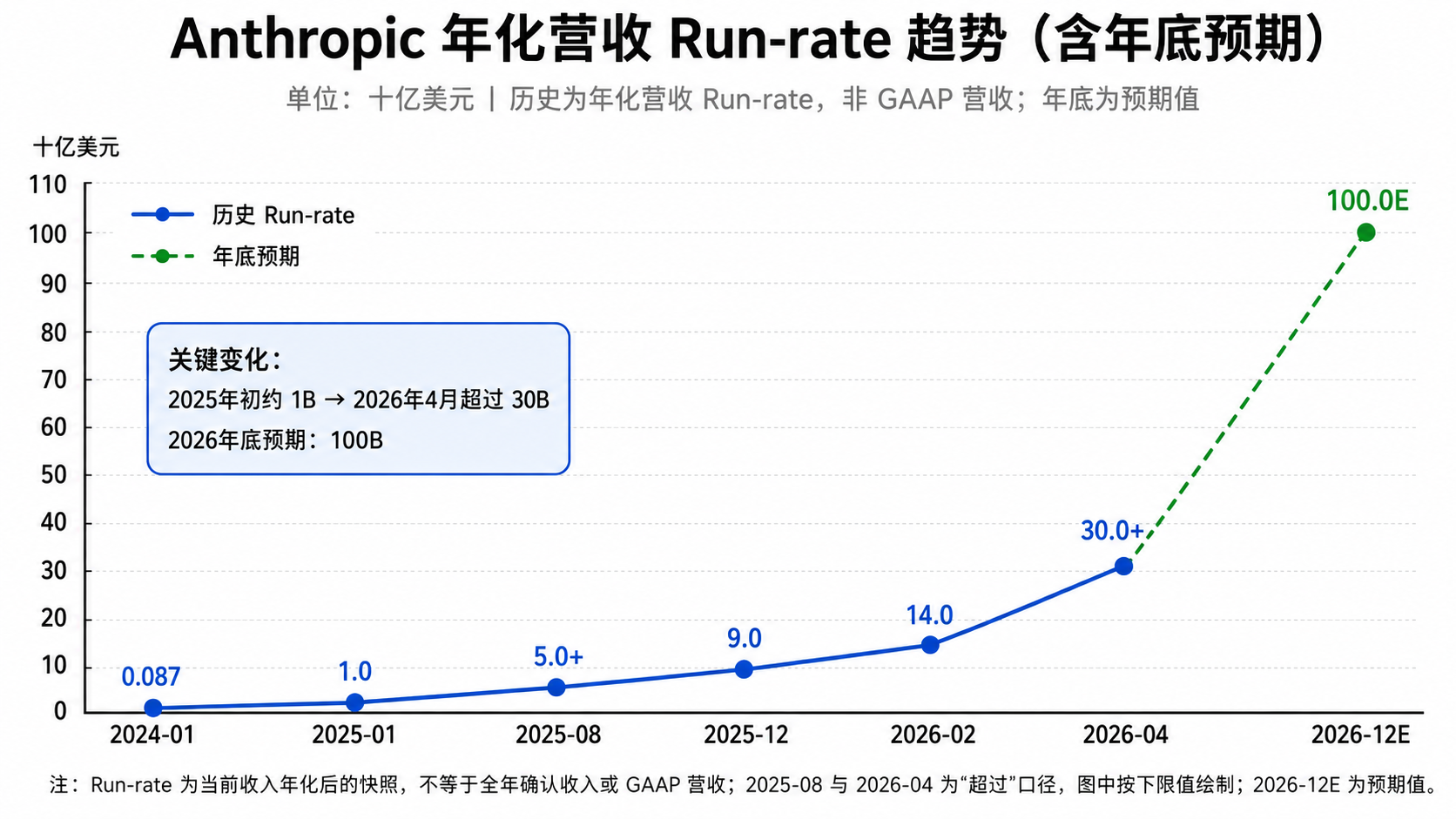

If Anthropic is valued at $1T, with year-end ARR/run-rate reaching $100B, that's only about a 10x price-to-sales ratio (not expensive for a company that's still early-stage and growing rapidly).

If the profit margin can reach 40%, the corresponding PE would be about 25x (large tech companies have long maintained PEs above 30x), which is very cheap.

To get to the point: if it goes public with a $1 trillion market cap, I think it's worth buying.

Current stage: Fierce competition means prices can't be raised temporarily, and profits can't increase. Programming is the only area where AI has deeply penetrated.

Future stage: Once the competitive landscape settles, companies will start focusing on profitability, with deep penetration across various sectors and unlimited potential.

A 10% expansion in profit margin, from 40% to 50% (software companies have long-term profit margins of 70%+), translates to a 25% growth in the company's profitability. Over 4 years, that's 100% profit growth, easily achieving the exaggerated gains of a Davis Double.

Nowadays, what company doesn't pay for large models? And this payment is just beginning. In the future, there will definitely be a large model company with a market cap exceeding $10 trillion.

The copyright of this article belongs to the original author/organization.

The views expressed herein are solely those of the author and do not reflect the stance of the platform. The content is intended for investment reference purposes only and shall not be considered as investment advice. Please contact us if you have any questions or suggestions regarding the content services provided by the platform.