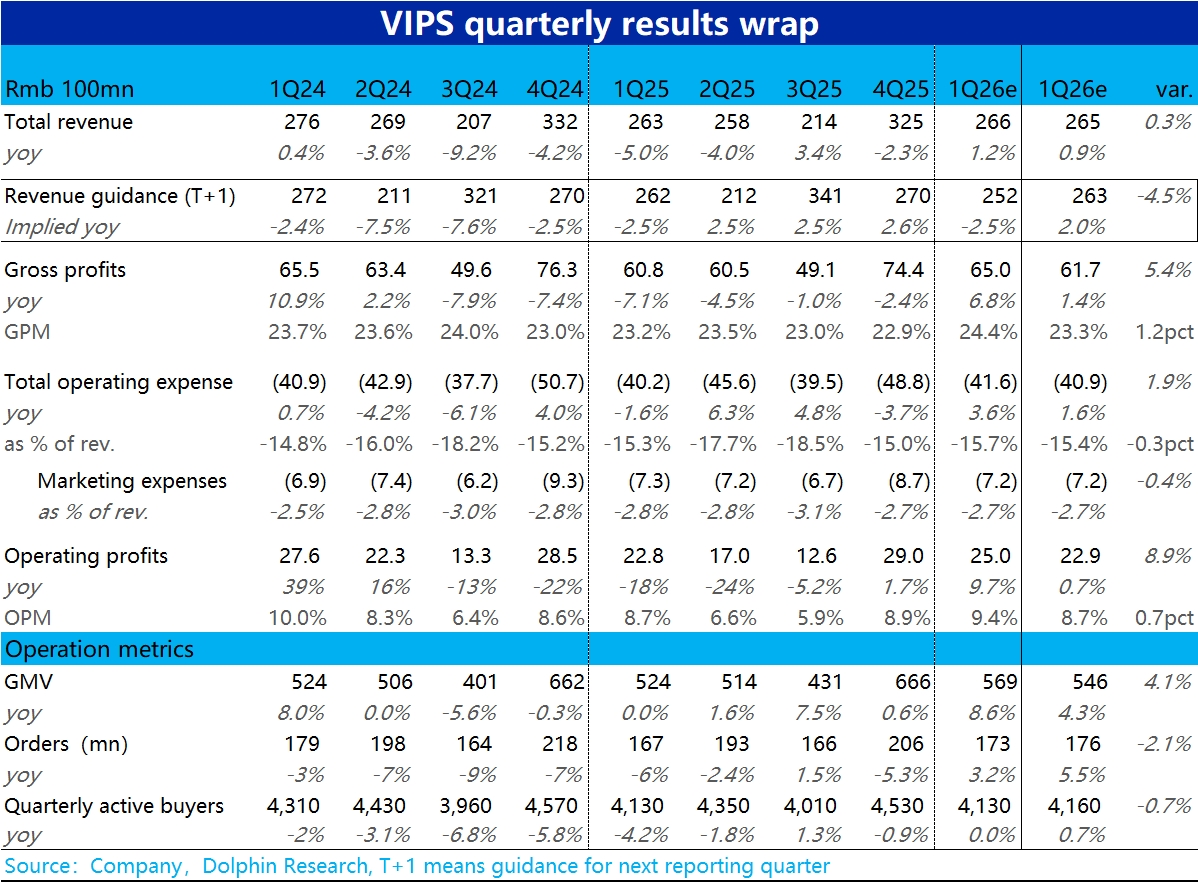

VIPS 1Q26 First Take: a solid quarter with a modest beat vs the Street. GMV growth and a higher GPM were the key positives. Guidance for 2Q revenue at -5% to 0% puts growth back into negative territory, though a softer 2Q vs 1Q across e-comm is broadly expected.

In detail:

1) GMV rose nearly 9% YoY, beating Bloomberg consensus of ~5%, and improved materially from roughly flat QoQ in the prior quarter. On the flip side, order volume grew about 3% YoY and quarterly active users were flat. Growth therefore remained primarily driven by higher AOV.

2) Total revenue grew 1.2% YoY, at the low end of prior guidance and broadly in line with conservative Street expectations, as GMV strength did not translate to revenue. Based on past patterns and the fact that other revenue grew far faster than self-operated retail revenue (+14% vs +0.2%), it is reasonable to infer a higher return rate and faster growth in 3P GMV (incl. shanshan).

3) With higher AOV and a larger mix of non-self-operated retail revenue, GPM expanded by 120bps, well above market expectations. This was the biggest positive surprise this quarter.

4) Opex ticked up, rising 3.6% YoY, outpacing revenue and above market expectations. The increase was driven mainly by fulfillment expenses, up 8% and tied to volume, while other costs were flat to down.

5) While opex ate into part of the GPM beat, OP came in near 2.5bn, above the Street at about 2.3bn, up nearly 9% YoY. Profit growth was solid. $Vipshops(VIPS.US)

The copyright of this article belongs to the original author/organization.

The views expressed herein are solely those of the author and do not reflect the stance of the platform. The content is intended for investment reference purposes only and shall not be considered as investment advice. Please contact us if you have any questions or suggestions regarding the content services provided by the platform.