After weathering the worst, how close is NIO to a full turnaround?

$NIO Inc(NIO.US) released its Q1 2026 results pre-market in the US and post-close in HK on May 21, Beijing time. Despite the seasonal lull, Nio showed solid earnings resilience, with key takeaways as follows:

1. Vehicle revenue slightly missed but remained up sharply YoY: In Q1, vehicle sales revenue was RMB 25.5bn, just below the market's RMB 26.0bn estimate but up 112% YoY.The miss was mainly due to ASP of RMB 273k vs. RMB 277k expected, though ASP rose by RMB 20k QoQ as the high-priced ES8 accounted for over half of the mix, lifting overall pricing.

2. Vehicle GPM continued to improve, bucking seasonality: Q1 vehicle GPM was 18.8%. Despite weaker scale benefits and higher procurement costs, Nio maintained a high margin level and even improved 70bps QoQ, above the market's 18.2% and prior guidance for flat QoQ.Mix shift toward higher-end models offset headwinds from softer scale and rising raw materials.

3. Opex disciplined; cost-down and efficiency gains ongoing: With Q1 deliveries down 33% QoQ to ~83.5k units, management had expected a small operating loss.However, better-than-expected GPM and lower R&D spend (RMB 1.9bn, below consensus and guidance) led to a narrower loss: OP was -RMB 0.3bn vs. -RMB 1.0bn expected, and OPM was -1.2%, down 3.5ppt QoQ but ahead of the -3.8% consensus.

Overall, Nio demonstrated resilient profitability through the off-season. Strong volumes of the high-priced ES8 supported margins, while ongoing cost and expense controls created more room at the bottom line.

All in, Q1 was solid: revenue was a slight miss, but margins held at a high level through seasonality.The core driver was the ES8's strong ramp, which shored up GPM and offset headwinds from weaker scale and higher procurement costs, while tighter cost control widened profit headroom and kept losses slightly better than expected.

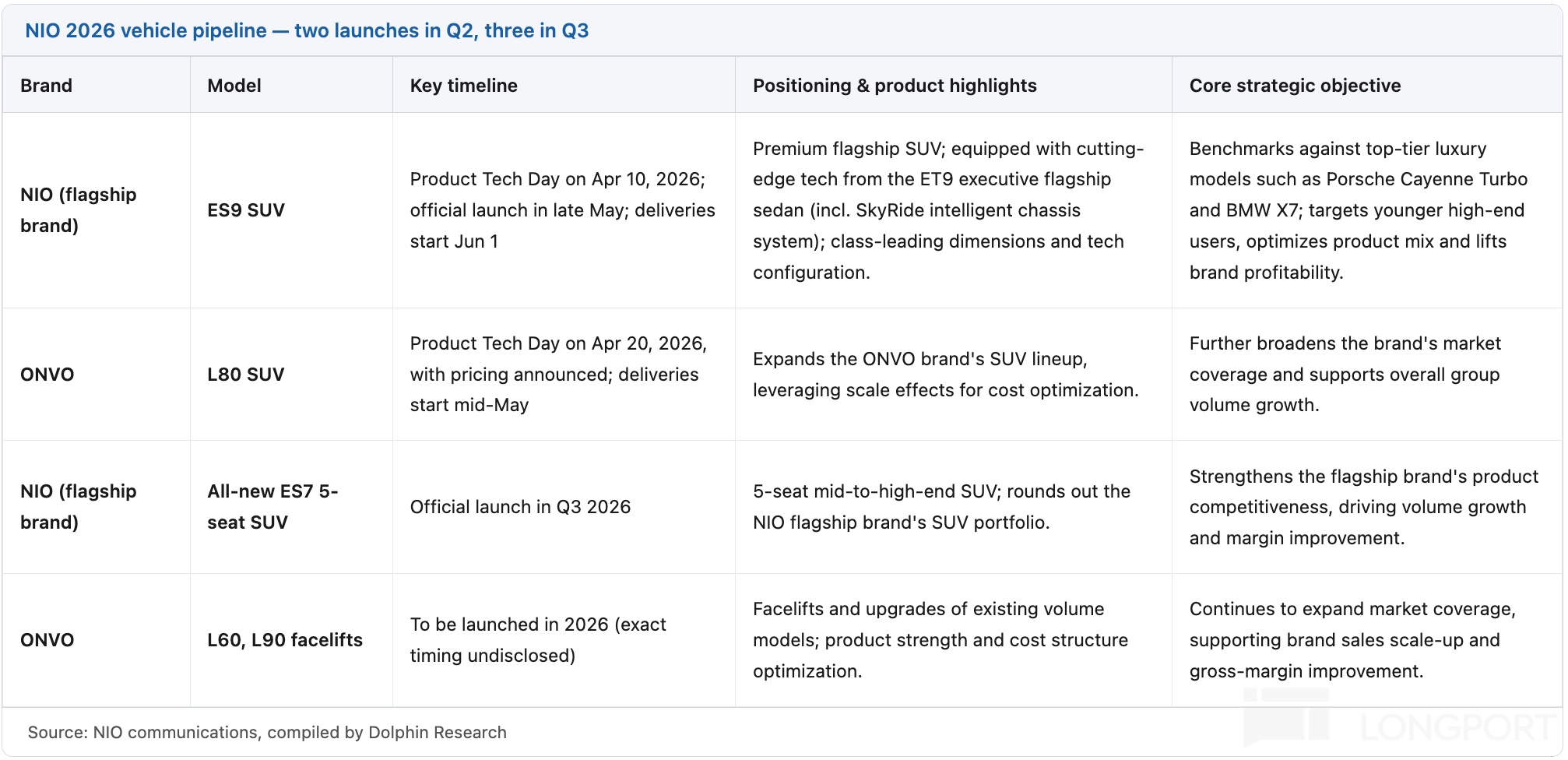

More importantly than the print is Q2 guidance. With two major models — ES9 and ONVO L80 — both starting deliveries in May, Nio's upbeat volume and revenue guide implies healthy order intake for these launches.

① Q2 deliveries are guided at 110k–115k, above the market's ~106k. With only ~29.4k delivered in Mar, the guide implies average monthly deliveries of 40k–43k in May/Jun, a very strong pace.

Notably, ES8 lead time shortened from 4–5 weeks in Mar to 2–4 weeks in Apr, indicating rapid digestion of backlog. Thus, Q2 upside should mainly come from ES9 and L80 (and, to a lesser extent, refreshed 5566 models), corroborating ample order reserves and delivery cadence aligned with demand.

② Q2 total revenue is guided at RMB 32.9bn–34.4bn, well above the ~RMB 30bn consensus, with both volume and ASP beating expectations. The guide implies Q2 vehicle ASP of ~RMB 270k, roughly flat vs. Q1's RMB 273k.

Given ES8's Q1 mix share reached 54% but its backlog and deliveries are now declining QoQ, maintaining a high ASP in Q2 hinges on the higher-priced ES9 stepping in. Management confidence in ES9's monthly run-rate appears strong; if ES9 (pre-sale RMB 528k–658k) sustains 5k+ units per month, Nio's GPM should remain elevated, with mix upgrade offsetting BOM inflation and potentially pushing margins higher.

For full-year 2026:

Management previously guided for 40%–50% YoY delivery growth (approx. 456k–490k units), backed by a heavy product cycle starting in Q2.

Nio ES9 (on sale and delivering from May 27): a 5.4m all-new flagship carrying ET9 core tech, with pre-sale pricing of RMB 528k–658k. Dealer checks indicate refundable RMB 5,000 deposits could total ~40k units nationwide.ES9 emphasizes spaciousness and first-class ride experience, with premium interior and design that reflect Nio's brand aesthetics and flagship positioning; dealers expect a steady 5k+ units per month, potentially repeating ES8's success.

ONVO L80 (on sale and delivering from May 15): the 5-seat version of L90, priced at RMB 242.8k–279.8k. It targets incremental demand in the RMB 200k–250k segment with a lower entry point.

Nio ES7 (Q3 launch): a 5-seat version of ES8 to further consolidate the high-end base.

Among existing models, the previously popular 5566 series has been refreshed. ES8, successful in 2025, will contribute a full 12 months in 2026, and ONVO L60 and L90 are also slated for facelifts.

As such, Nio's 2026 pipeline looks robust, underpinning confidence in high delivery growth guidance. The strategic focus is clearly pivoting toward 'big SUVs' and further premiumization.

Against a slower NEV market in 2026 due to purchase tax roll-off (industry growth expected at only 5%–15%), Nio's BaaS model stands out. Because batteries are excluded from the vehicle invoice, the taxable base is much lower.This means Nio buyers pay less purchase tax vs. peers in the same segment, helping cushion macro headwinds from the tax rollback.

Guidance on margins and profitability is also constructive:

Nio expects vehicle GPM to improve from 18% in Q4 2025 to around 20% in 2026. Key drivers include the launch of higher-margin ES9, scale-driven cost reductions (further magnified by ONVO L80, Nio ES7, etc.), and margin uplift from the refreshed ONVO L60 SUV.

On expenses, Nio continues to tighten the belt: 2026 full-year R&D is expected to be flat vs. Q4 2025 annualized levels, and SG&A ratio is guided to around 10% of revenue. With higher volumes, better vehicle margins, and strict control of R&D and SG&A, Nio aims to achieve full-year profitability in 2026.

In sum, Dolphin Research believes that, while Q1 volumes were pressured by seasonality, pricing and margin resilience from an improved mix have become more evident.

For 2026 full-year deliveries, Nio benefits from some buffer against the tax rollback via BaaS and a strong pipeline (ES9, L80, ES7). However, with the broader NEV industry expected to grow only 5%–10% YoY, we prefer to stay cautious versus management's 40%–50% guide to 456k–490k units and will monitor execution.

Base-to-neutral case: factoring in tougher competition, price-war risk, and ramp uncertainties, we assume 20%–30% YoY growth to 390k–430k units in 2026. With ASP rising from RMB 236k in 2025 to ~RMB 248k in 2026 on greater mix of higher-margin large vehicles, and continued growth in services revenue, we estimate total revenue of RMB 110bn–119bn (+26%–36% YoY).On a neutral 1.0x 2026 P/S, implied market cap is RMB 110bn–119bn, offering ~18%–27% upside vs. the current HK valuation of ~RMB 93.5bn.

Upside case: if the high-priced ES9 sustains 5k+ units per month (lifting margins) and the volume driver ES7 reaches 10k–12k per month, deliveries could rise ~40% YoY to 456k (near the low-end of guidance). Under this scenario, at 1.2x 2026 P/S, implied market cap would be ~RMB 150bn, or ~60% upside vs. current levels.

Thus, whether Nio can break through its valuation ceiling hinges on the ES9 and ES7 achieving volume scale — the former sets margin height, the latter drives volume and revenue. If both deliver, the profit inflection and re-rating would have a solid foundation.

I. Vehicle GPM 'strong despite off-season'

As the most critical metric each quarter, we first look at vehicle profitability. Nio had guided that Q1 vehicle GPM would be flat QoQ vs. Q4 2025's 18% as ES8 (GPM >20%) gained mix, offsetting cost inflation and smaller scale, aligning market expectations at 18.2%.

Actual Q1 vehicle GPM was 18.8%. Despite weaker scale and higher procurement costs, margin stayed high and rose 70bps QoQ, beating expectations and prior guide, as higher mix lifted ASP and offset cost drag.

1) ASP: continued QoQ improvement, driven by high-priced ES8

Q1 ASP was RMB 273k, slightly below the RMB 277k consensus, but up a notable RMB 20k QoQ from RMB 253k. The key driver was continued scale-up of the high-priced ES8 SUV (RMB 406.8k–456.8k list).Although ES8 orders in Q4 2025/Q1 2026 carried RMB 15k/10k discounts, ES8's mix jumped 22ppt QoQ to 54%, lifting overall ASP and offsetting promotional pressure.

Meanwhile, the premium Nio brand mix rose 16ppt QoQ to 70%, reinforcing the upward price structure.

2) Unit cost: up QoQ on weaker scale and raw material inflation

In Q1, unit cost was RMB 222k, up ~RMB 14k QoQ, driven by higher ES8 production cost and headwinds from weaker scale and raw materials. Even so, vehicle margins remained stable.

① Off-season scale effect: Q1 sales were ~83.5k units, slightly above the guided range but still down 33% QoQ amid seasonality and tax headwinds, diluting scale and lifting per-unit overhead.② Procurement costs rose, but near-term impact was limited: pressures came from memory, raw materials, and batteries, but were contained because: a) long-term contracts delay major cost swings, likely showing up in Q2; b) the swap model's low-cost battery inventory buffered the Q1 battery price spike.

③ Platform and supply-chain cost-down continued to offset: the NT3.0 platform with 900V architecture and zonal controllers drove high hardware integration, lowering materials and manufacturing costs. Coupled with supplier savings and in-house tech (replacing Nvidia Orin-X with the self-developed NX9031, cutting ~RMB 10k per vehicle), ES8 maintained 20%+ GPM even with a RMB 10k discount in Q1.

3) Unit GP: up QoQ, margins 'strong despite off-season'

Q1 unit GP was RMB 51k, up RMB 5k QoQ from RMB 46k, and vehicle GPM reached 18.8%, up 70bps QoQ. Again, ES8's strong ramp offset weaker scale and higher procurement costs.

II. Q2 volume and revenue guides 'beat', implying healthy new-order intake

1) Q2 deliveries guided at 110k–115k, above market

With two major launches — ES9 and ONVO L80 — entering sales and delivery in Q2, Nio guided 110k–115k units, above the ~106k consensus. Given only ~29.4k were delivered in Mar, the guide implies 40k–43k average monthly deliveries for May/Jun, a robust cadence.

ES8 lead times shortened from 4–5 weeks in Mar to 2–4 weeks in Apr, signaling fast backlog digestion. Hence, most incremental beats in Q2 should be driven by ES9 and L80 (and refreshed 5566), confirming strong order books and aligned delivery pace.

2) Q2 revenue and ASP both above expectations

Total revenue guided at RMB 32.9bn–34.4bn vs. ~RMB 30bn consensus, with both deliveries and ASP ahead. Implied vehicle ASP is ~RMB 270k in Q2, roughly flat vs. Q1's RMB 273k.

As ES8 accounted for 54% of the Q1 mix but its backlog and deliveries are now trending lower QoQ, ES9 must backfill to sustain high ASP. If ES9 holds at 5k+ per month, mix benefits should counter BOM inflation and may drive further GPM expansion.

Looking at the overall picture:

III. GPM continued to climb QoQ, reaching a record high

Total Q1 revenue was RMB 25.5bn, up 112% YoY but slightly below the RMB 26.0bn consensus, mainly on ASP.

① Vehicle revenue was RMB 22.8bn vs. RMB 23.1bn expected as ASP of RMB 273k came in below the RMB 277k estimate, though, as noted, ASP rose by RMB 20k QoQ on a higher ES8 mix.② Other revenue was RMB 2.75bn, down ~RMB 0.3bn QoQ, driven by lower tech services and used-car sales.

Overall GPM was 19% in Q1, up 1.5ppt QoQ to a record high, with both vehicle and other segments beating.

① Vehicle GPM was 18.8%, up 8.6ppt YoY as ES8 mix rose and prior cost-down delivered, offsetting weaker scale and raw material inflation.② Other-segment GPM was 20.6%, up 8.8ppt QoQ from 12% even as high-margin tech services declined QoQ, mainly due to: a) efficiency gains in energy services and faster loss reduction at swap stations; b) growth in higher-margin parts, accessories, and after-sales.

IV. Continued R&D cuts; cost-down and efficiency push sustained

Nio historically spent heavily to build a luxury brand, but since Q2 2025 it has undertaken sweeping reforms. Q1 again showed cost-down and efficiency gains beating expectations, supporting profit leverage.

1) SG&A: flat QoQ, down meaningfully YoY

SG&A had been elevated due to the Nio House footprint, service system, staffing, and separate channels for the Nio and ONVO brands. Now, ONVO has merged into the main Nio channel to share resources, and ongoing optimization of sales and service teams has lowered payroll and marketing costs.Q1 SG&A was ~RMB 3.5bn, down ~RMB 0.9bn YoY from the ~RMB 4.4bn peak in Q1 2025 and roughly flat vs. Q4 2025's RMB 3.54bn.

Despite seasonality, SG&A did not drop QoQ because the company invested to prepare for the Q2 launch cycle — maintaining channel exposure and staffing for ES9 and L80 — rather than relaxing discipline. Management has guided 2026 SG&A ratio to below 10% of revenue, indicating orderly expense control.

2) R&D: further reduced to RMB 1.9bn

Q1 R&D was RMB 1.9bn, down RMB 0.13bn QoQ from RMB 2.03bn, below the RMB 2.2bn consensus and the prior RMB 2.0bn–2.5bn quarterly guide. The decline reflects the passing of prior peaks (e.g., NT3.0 development largely complete), team optimization, and efficiency gains in design and development.

Importantly, R&D efficiency improved even as spend fell, evidenced by two aspects:

① AD stack upgraded with world-model approach, boosting all-scenario performance: Nio rolled out NWM 2.0 early in the year, integrating a 'world model' and closed-loop reinforcement learning. Through massive imitation learning, long-horizon digital-world decision rollouts, and high-frequency closed-loop RL, it delivers an end-to-end loop from core tech to user experience, significantly improving highway/city pilot, auto-parking, and active safety; user AD usage hours rose over 80% MoM in Feb, with two major updates planned this year.

② In-house chip business secured external funding, advancing commercialization: the entity for the self-developed NX9031 (Shenji) completed a first-round external raise of RMB 2.257bn via new shares; Nio holds 62.7% of the chip subsidiary. Built on 5nm with 1,000+ TOPS, performance rivals multiple Nvidia Orin-X chips.Beyond strengthening the cash position, this marks a shift from internal use to external supply, opening new monetization pathways.

Meanwhile, the second-gen 5nm AD chip has taped out, with better performance and much lower cost, and a mid-range product line is planned to cover broader customers. This signals a move from single-point R&D to a product matrix and readies offerings for external commercialization; the market expects continued independent financing with a long-term goal of a standalone listing.

V. Losses slightly better than expected

With Q1 deliveries down 33% QoQ to ~83.5k, management had anticipated a small operating loss. Yet better-than-expected GPM and further R&D cuts to RMB 1.9bn (below consensus and guidance) led to narrower losses vs. expectations.

Q1 OP was -RMB 0.3bn vs. -RMB 1.0bn expected; OPM was -1.2%, down 3.5ppt QoQ, but ahead of the -3.8% consensus. Overall, Nio showed strong profitability resilience during the off-season — ES8 mix supported margins, and ongoing cost controls expanded bottom-line flexibility.

<End here>

For more of Dolphin Research's in-depth work and tracking on Nio, click:

Earnings:

Sep 2, 2025, earnings take: 彻底弃 ‘价’ 保命,蔚来困境反转 ‘够味’ 吗?

Sep 3, 2025, call Trans: 蔚来(2Q25 纪要):仍然维持四季度盈亏平衡目标

Jun 3, 2025, earnings take: 蔚来:画饼无用,活下来才有 ‘未来’

Jun 4, 2025, call Trans: 蔚来(1Q25 纪要):砍三费,缩摊子,蔚来能否生死自救?

Mar 23, 2025, call Trans: 蔚来(纪要):2025 年计划 NIO 品牌毛利率 20%、ONVO 品牌 15%

Mar 22, 2025, earnings take: 蔚来:Nio 丧,乐道萎,蔚来还能拥有未来吗?

Events

Sep 9, 2025: 终于 ‘活明白了’!但蔚来真能 ‘重生’ 吗?

Risk disclosure and statements: Dolphin Research disclaimer and general disclosure

The copyright of this article belongs to the original author/organization.

The views expressed herein are solely those of the author and do not reflect the stance of the platform. The content is intended for investment reference purposes only and shall not be considered as investment advice. Please contact us if you have any questions or suggestions regarding the content services provided by the platform.