SOXS Commentator

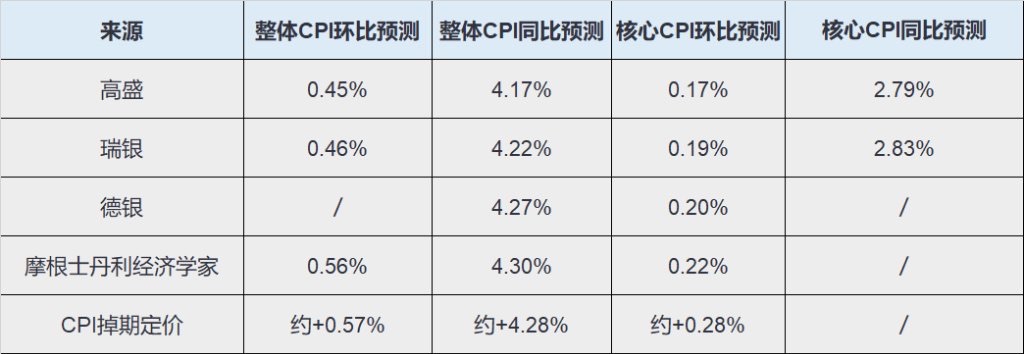

SOXS Commentator$Direxion Semicon Bear 3X(SOXS.US)The impact of the CPI trend on long-term US Treasury rates is the real medium-term bloodletting at the discount rate and liquidity level, reflecting institutional thinking. As long as tonight's data exceeds April's 3.8% (even just 3.9%), that's enough to trigger a chain reaction. Lower than 4.2%? Totally possible! If it really falls below 4.2%, US stocks are highly likely to stage a strong rebound on sentiment. But does that mean the "summer chill" is over? Absolutely not. As long as it's higher than April's figure, we must remain highly vigilant.

The "grey rhino" is never inflation itself, but the unexpected rise in long-term US Treasury rates (10-year)!

Look at the current macro picture: the US is deep in debt, interest payment pressure is off the charts, and geopolitics is a mess. In this context, if the inflation trend in May and June is just higher than April's, long-term rates are bound to rise. Not to mention the two major catalysts ahead: the blockade effect in the Strait of Hormuz is still transmitting, coupled with the upcoming 6.11-7.19 US-Canada-Mexico World Cup. The high volatility in energy prices will inevitably quickly feed into North America's core services inflation. The 10-year US Treasury yield is highly likely to surge beyond expectations.

It's highly probable that inflation will continue to worsen in May and June, and the rise in long-term US Treasury rates is far from over. The grey rhino is already on the run, and it needs enough time and space to unleash its destructive power.

Tonight, if CPI really falls below 4.2%, causing the already extremely crowded AI concept stocks to stage another strong rebound, everyone must stay calm and control your hands! Don't be fooled by sentiment into buying at highs. Guarding against subsequent greater stampede risks is the key to surviving this summer.

The copyright of this article belongs to the original author/organization.

The views expressed herein are solely those of the author and do not reflect the stance of the platform. The content is intended for investment reference purposes only and shall not be considered as investment advice. Please contact us if you have any questions or suggestions regarding the content services provided by the platform.