ATFX: US June CPI data is coming, annual rate may drop to 3.8%, core expected unchanged

ATFX: At 20:30 today, the U.S. Bureau of Labor Statistics will release the U.S. core CPI year-on-year rate, with the previous value at 4.2% and the expected value dropping to 3.8%, primarily based on the easing of geopolitical issues. The core CPI year-on-year rate is expected to remain unchanged at 2.9%, mainly due to not being significantly affected by energy and food prices. The June CPI month-on-month rate is expected to drop from 0.5% to -0.1%, and the core CPI month-on-month rate is expected to remain at 0.2%.

The main highlight of this data release lies in the decline range of the CPI year-on-year and month-on-month rates. If it exceeds the expected 0.4 percentage points, it means that U.S. inflation is falling rapidly, which could have a significant impact on the U.S. dollar, benefiting U.S. stocks. If the decline in inflation is not significant, coupled with the resurgence of Middle East geopolitical issues, it may trigger expectations of a Fed rate hike.

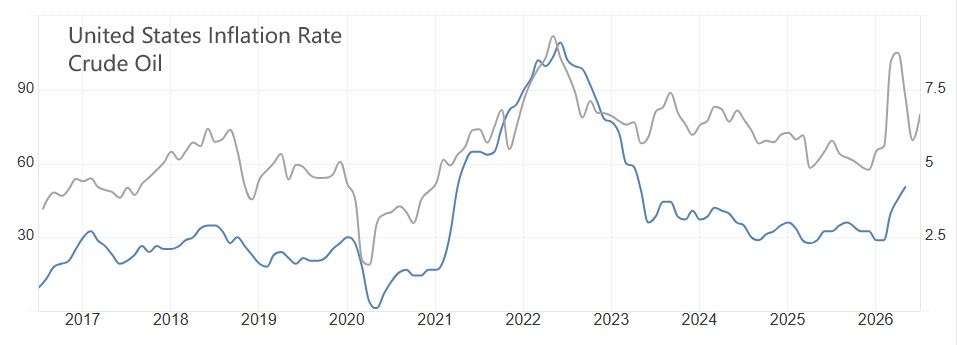

Chart 1: WTI Price Overlaid with U.S. CPI Year-on-Year Rate - ATFX

WTI crude oil price (gray line) and the U.S. CPI year-on-year rate (blue line) show a clear positive correlation. Between 2021 and 2022, both rose significantly in sync, with soaring oil prices directly pushing inflation to high levels; after 2023, the decline in oil prices gradually cooled CPI, and during oil price fluctuations from 2025 to 2026, CPI also showed corresponding ups and downs, verifying that energy prices are an important driver of U.S. inflation. From a long-term trend perspective, WTI oil price is not only a synchronous indicator of inflation but also a leading signal. After 2020, every significant rebound in oil prices led to an uptick in CPI one to two months in advance, suggesting that if the current oil price remains in low-level fluctuations, core inflation is expected to further decline to the 2% target range, opening up space for the Fed to cut rates multiple times within the year.

Risk exists in Middle East geopolitical issues. On June 25, Iranian drones attacked merchant ships, and the U.S. subsequently struck Iran. To this day, conflicts between the U.S. and Iran around the Persian Gulf coast continue, with Iran announcing the blockade of the Strait of Hormuz and the U.S. striking Iran's nuclear facilities again (Gaoshan underground facility). Affected by this news, international oil prices have returned above $80. Even if the June CPI year-on-year rate significantly declines, the July CPI may rise again.

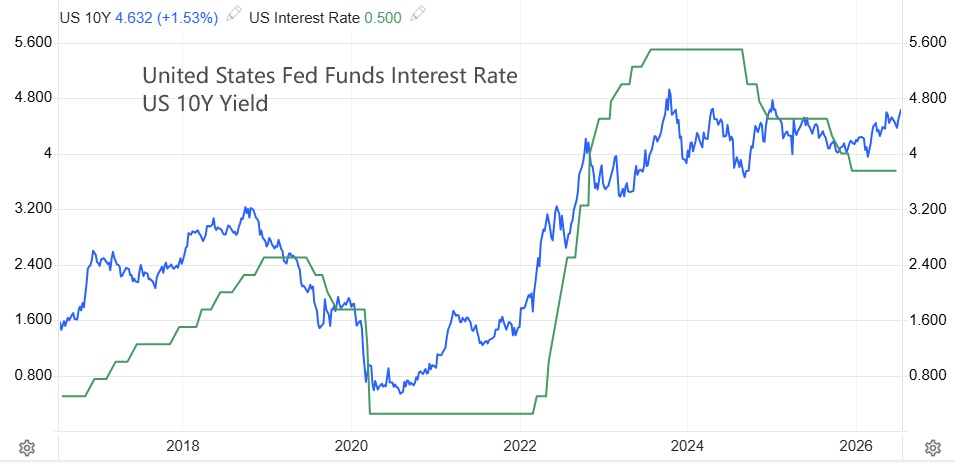

Chart 2: Fed Rate Overlaid with 10-Year U.S. Treasury Yield - ATFX

The Fed's benchmark rate and the U.S. 10-year Treasury yield are highly correlated. During the Fed's tightening cycle, short-term policy rates rise rapidly, driving up long-term yields; during the easing cycle, they decline in sync. Currently, the 10-year Treasury yield has rebounded to around 4.63%, while the Fed rate remains in a plateau. The Fed's monetary policy determines long-term Treasury yields, so there is a possibility that Treasury yields will revert to the Fed rate. The current Treasury yield being higher than the Fed rate of 3.75 means there may be a corrective rate cut by the Fed in the future.

If the U.S. inflation rate can fall to around the 2% moderate inflation level, the Fed's willingness to cut rates will significantly increase. The uncertainty lies in how long the differences between the U.S. and Iran on Middle East issues will persist. If the Strait of Hormuz remains blocked, or if there are repeated cycles of reopening and re-blocking, the supply side of the international energy market may remain insufficient for a long time. The difficulty of reducing the U.S. inflation rate will be greatly increased.

ATFX Risk Warning, Disclaimer, Special Statement: The market carries risks, and investment requires caution. The above content only represents the analyst's personal views and does not constitute any operational advice. Please do not treat this report as the sole reference. In different periods, the analyst's views may change, and updated content will not be notified separately.

The copyright of this article belongs to the original author/organization.

The views expressed herein are solely those of the author and do not reflect the stance of the platform. The content is intended for investment reference purposes only and shall not be considered as investment advice. Please contact us if you have any questions or suggestions regarding the content services provided by the platform.