$Microsoft(MSFT.US)Will employees go against the leadership if the CIO says which AI company to buy?🤔

SpiceMonkey

AssetsTop 24%ReturnsTop 76%SmallValue

核心资产 拿住不动

SpiceMonkeySuggestions for you to follow

S

$NVIDIA(NVDA.US)$Micron Tech(MU.US)$SK Hynix(SKHY.US)$Samsung Electronics (SSNGY.US) Inference cards skipping HBM? Let's wait for the actual test data from the 64-card rack 🧐 But regardless of who wins, the physical limit still needs to be broken by the advanced packaging of the shovel's shovel 😋 Suitable for a three-phase layout.

NVIDIA

USNVDA

S

$Micron Tech(MU.US)$Sandisk(SNDK.US)$Roundhill Memory ETF(DRAM.US)$Amazon(AMZN.US)Are even the landlords' financiers running out of surplus grain? 🙃 The willingness to subscribe to bond issuance is already low. If ROI doesn't show significant improvement, I'm afraid capex can't be increased anymore.

Micron Tech

USMU

S

$Microsoft(MSFT.US)

Hot take: Storage manufacturers have drained cloud providers' cash through long-term agreements → Cloud providers cut back on buybacks → Stock prices lose buyer support → Rising storage costs force end-product price hikes → Driving up CPI/PCE → The Fed is forced to remain hawkish → High interest rates persist → Tech stock valuations continue to be compressed → More selling 😅

Any resemblance is purely coincidental.

Microsoft

USMSFT

S

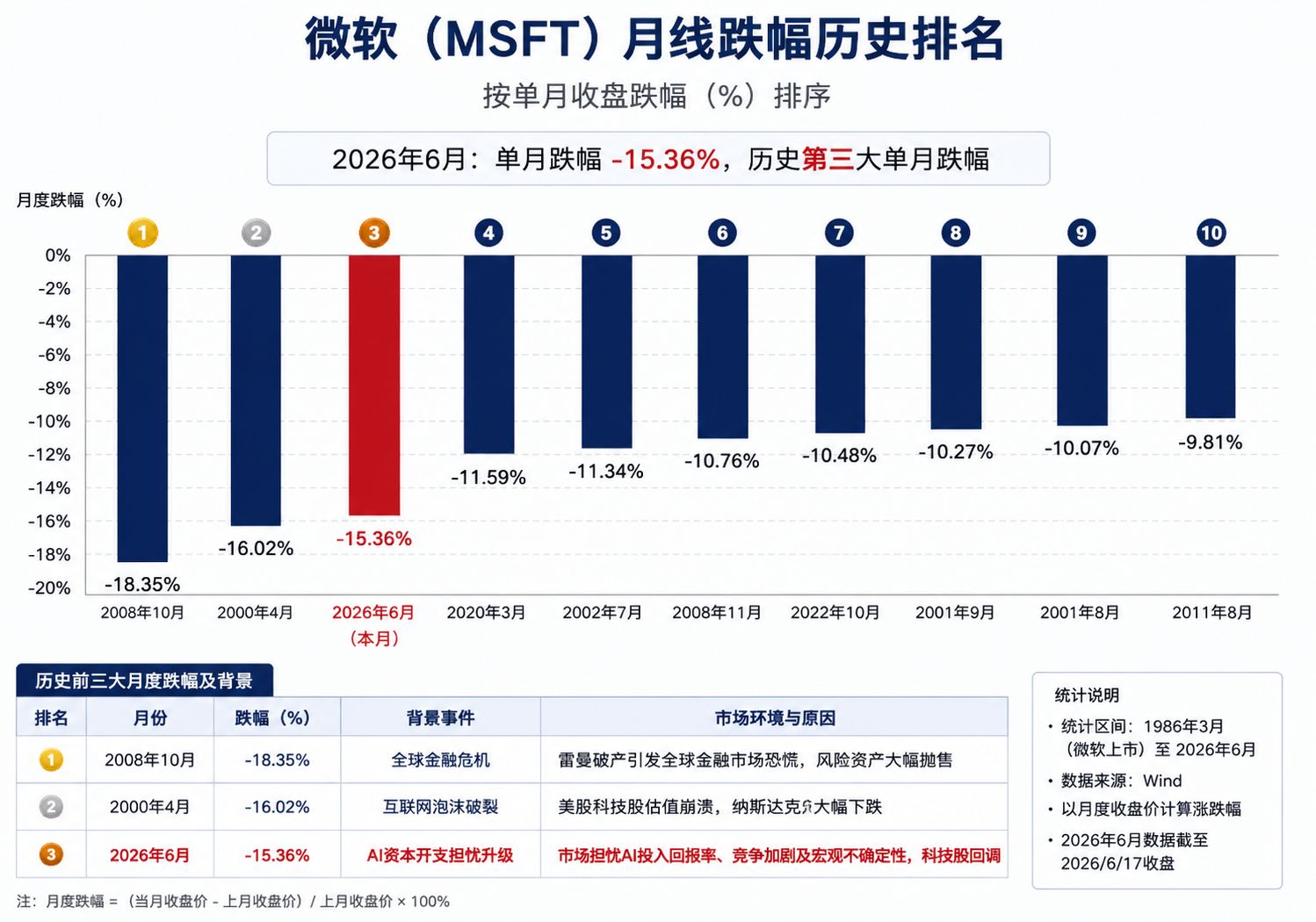

$Microsoft(MSFT.US) falls two points every day. It only needs to fall for another 291 days to be delisted. 😅

Microsoft

USMSFT

S

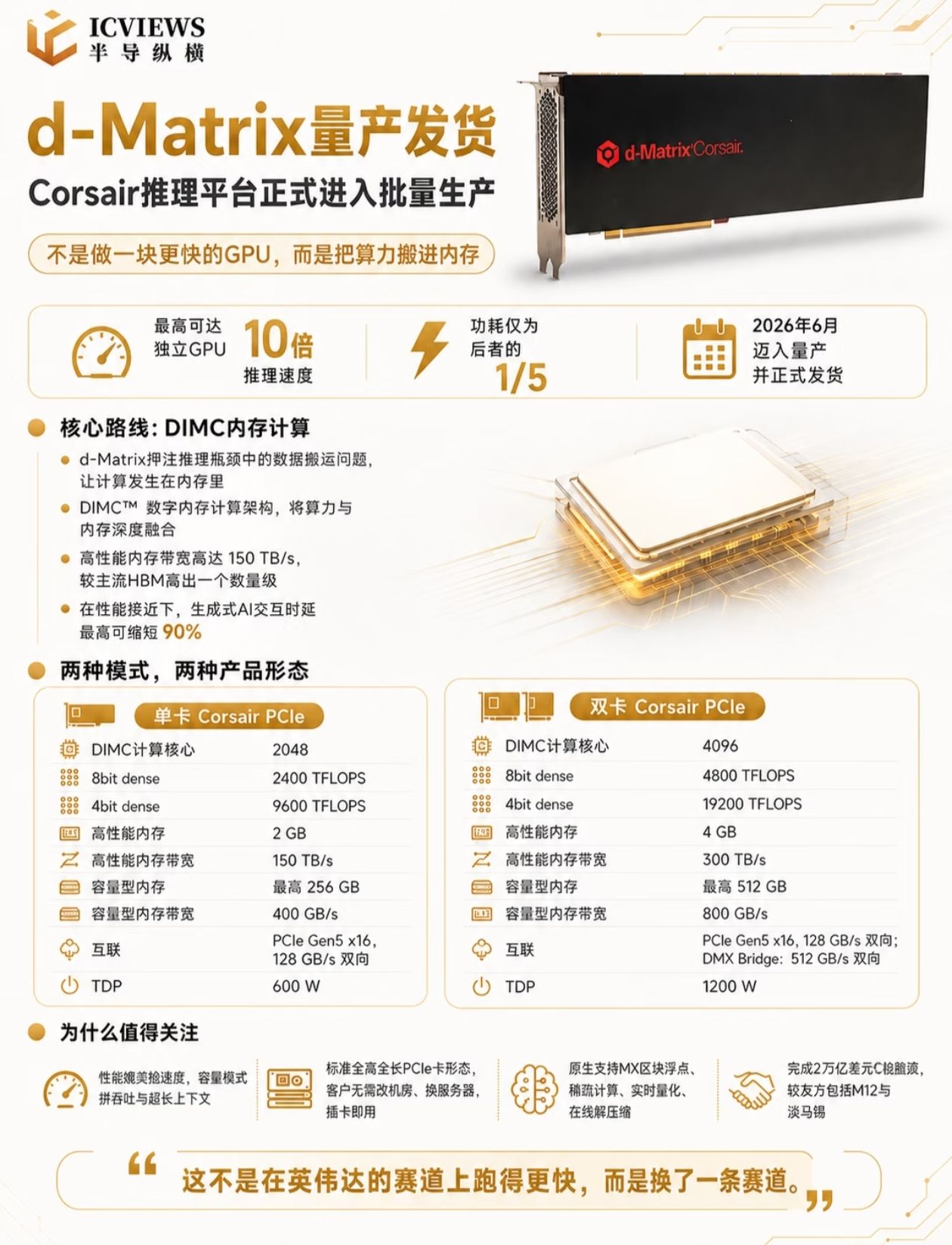

When it was mentioned in the last long article, there wasn't much news, and suddenly mass production has started. It's still a low-key launch for now. With plug-and-play compatibility and low demand for HBM, let's see which major manufacturer will be the first guinea pig. However, most that use chiplet will have to face TSMC's capacity issues 🤔. Additionally, it can only alleviate the HBM shortage problem; the high-bandwidth issue in the interconnect part is still unavoidable. This is basically the best application window now, and it seems all parties are rushing their schedules. Microsoft also invested in this company; will it be the first major manufacturer to conduct a small-scale trial? $Marvell Tech(MRVL.US)$Micron Tech(MU.US)$Sandisk(SNDK.US)$NVIDIA(NVDA.US)$Cerebras(CBRS.US)$Microsoft(MSFT.US)

S

Interesting, by the way, I've also referenced their design. Let's see if we can take the first step🌝🌝

S

$Ambarella(AMBA.US) Everyone is focusing on data centers, but I think AMBA's growth point is actually in robotics.

This year marks the first year of robotics. In edge intelligence, AMBA's low-power video chips could become a hit product. For a small-cap stock, the potential upside is significant.

Ambarella

USAMBA

S

$Cerebras(CBRS.US) is a large digital chip with extremely high power consumption, requiring custom oversized cooling🌝🌝 beneficial for liquid cooling

Cerebras

USCBRS

S

存算一体:噱头还是战未来

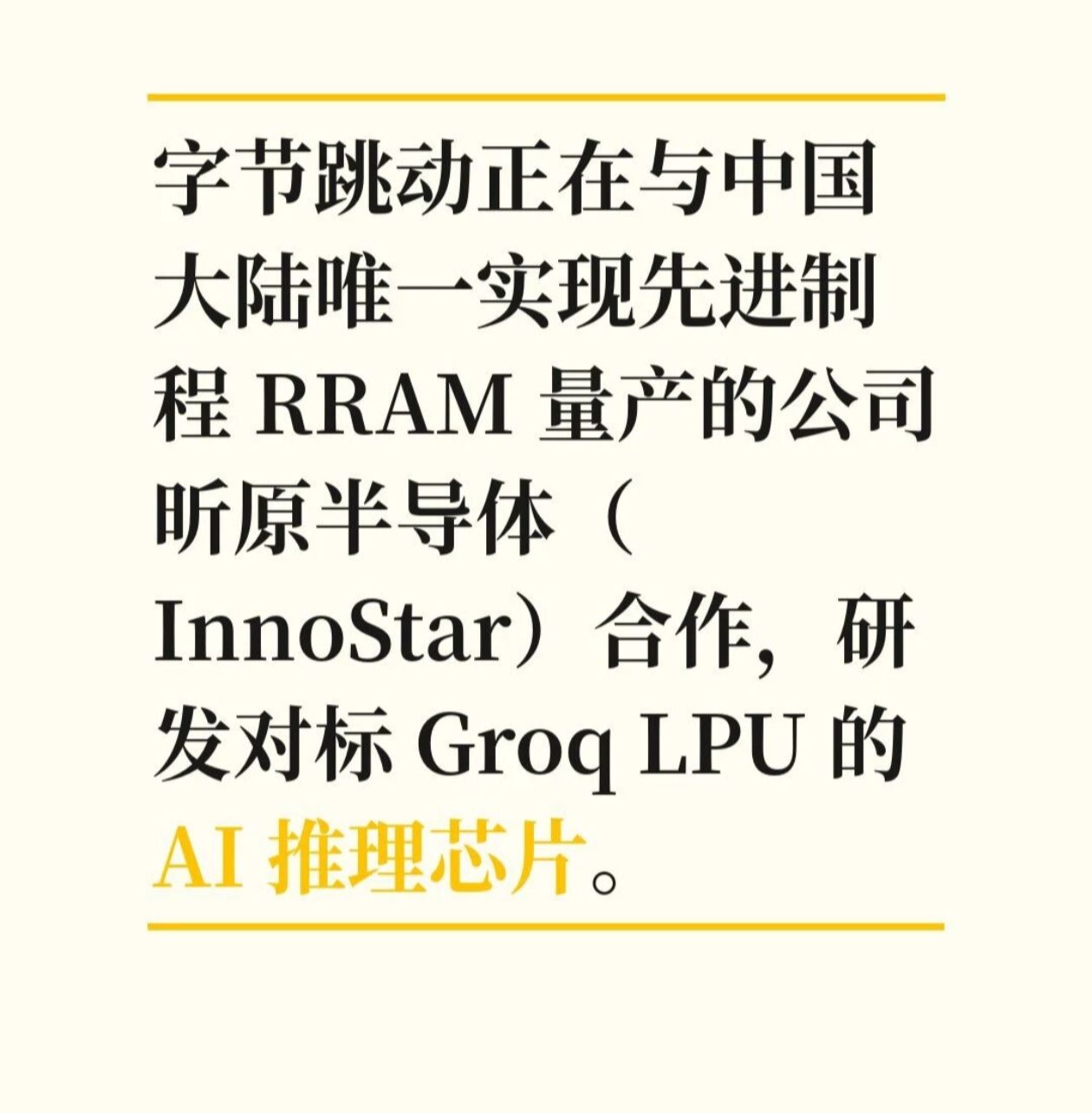

$Everspin Tech(MRAM.US) $Micron Tech(MU.US) $Sandisk(SNDK.US) $Taiwan Semiconductor(TSM.US) $XL2CSOPHYNIX(07709.HK) $XL2CSOPSMSN(07747.HK) $Intel(INTC.US) $NVIDIA(NVDA.US) $VeriSilicon(688521.SH)MRAM 又火了,我们 RRAM 什么时候能好起来存算一体不是新概念,属于老生常谈的了,以前火过一阵...

S

AetherCraft AI(灵境交互)

$Roblox(RBLX.US) I previously looked at RBLX's business model and had some ideas of my own, but didn't think them through in detail. Later, I saw Li Feifei's Astrocade funding round, which was actually somewhat similar to my own thoughts. So, I used AI to flesh out those vague ideas. Essentially, it's an attempt to combine a gaming platform with AI and token economics. The title was generated by AI, and it feels quite fitting for the concept, just for fun. @Miracle Trader cola Bro cola, take a look and see what you think...

Hypothesis Under Review

S

Views on ASML's earnings report

ASML's performance hasn't skyrocketed, with the core reasons being the dual physical constraints of "its own capacity limitations" and "lagging downstream Fab (wafer fab) construction." Here's a breakdown of the core logic: 1. Demand has actually already "exploded," but is limited by ASML's extremely long delivery cycle. To gauge ASML's business climate, one cannot just look at current revenue, but must also consider the order backlog. Lithography machines (especially EUV) are the most complex mechanical equipment currently manufactured by humans, and their supply chain is constrained by extremely high physical barriers (such as Zeiss's extreme ultraviolet lenses)...

S

$Broadcom(AVGO.US)$Marvell Tech(MRVL.US)

Personally, I think MRVL's TPU orders don't affect AVGO. Capacity is still the priority, bargaining power remains, and it's not a zero-sum game.

Broadcom

USAVGO

S

$Cleveland Cliffs(CLF.US) Regarding the situation with grain-oriented electrical steel (GOES), I consulted Gemini, no specific verification, just for fun 🌝

Regarding the underlying logic of the supply-demand game between AI data center power infrastructure and grain-oriented electrical steel (GOES), it can be distilled into the following three core dimensions:

1. Core Thesis: GOES is the hidden "hard bottleneck" of AI computing power expansion

The end of computing power is electricity, and the backbone of the power grid lies in transformers.

* **Cycle Mismatch:** Data center computing power iteration and expansion take only months, but the construction and process refinement of high-end GOES production lines take 3-5 years.

* **High-Barrier Oligopoly:** Manufacturing oriented silicon steel is extremely difficult. Globally, only a handful of companies have the capability for mass production of high-permeability oriented silicon steel (HiB). The supply side is extremely inelastic, leading to significantly extended transformer delivery cycles, granting upstream core material suppliers strong bargaining power and profit elasticity.

2. Macro Outlook: Geopolitics and Grid Challenges Will Not Weaken GOES Demand

The market worries that the US grid's weakness will lead to computing power moving overseas and weakening domestic construction, but the actual logic is the opposite:

* **Data Sovereignty Locks in Core Compute:** Constrained by high-end chip export controls and privacy compliance requirements for high-value large models, core ten-thousand/hundred-thousand-card training clusters must remain in the US or controlled regions, unable to easily "go offshore."

* **Nationwide Grid Renewal Cycle:** Setting aside AI growth, the US grid itself is severely aging. Combined with renewable energy integration and EV supercharger construction, domestic transformer replacement demand is already a rigid baseline.

* **Global Synchronization:** Even if some computing power shifts overseas (e.g., Southeast Asia, Middle East), as the GOES supply chain is a global oligopoly, overall capacity remains constrained. The material shortage and high pricing power hold true globally.

3. Technology Path: "Grid Bypass" Not Only Amplifies Demand but Cannot Be Fully Replaced by New Materials

To bypass main grid approvals, tech giants are turning to "behind-the-meter generation (microgrids/nuclear/gas)," which triggers an exponential increase in system complexity:

* **Redundancy Drives Usage:** For islanded microgrids to achieve Tier IV availability (e.g., 2N fault-tolerant architecture), each set of backup generation equipment requires independent step-up/step-down transformers. The standardization of large-scale Battery Energy Storage Systems (BESS) further increases the demand density for transformers and reactors.

* **Material Science Physical Limits:** While **amorphous/nanocrystalline** materials, with their extremely low core loss and excellent high-frequency characteristics, will capture the market for "high-frequency, low-power" components like UPS and energy storage inverters; due to their **lower saturation flux density (Bs)** (leading to bulky equipment) and **extreme physical brittleness**, they absolutely cannot replace traditional GOES in high-capacity backbone transformers.

**Final Conclusion:**

In the investment theme of AI infrastructure, capital often over-focuses on the visible digital logic computing power (GPUs, optical modules), while overlooking the underlying physical constraints supporting the operation of massive computing clusters. High-end GOES is precisely such a long-cycle, deterministic bottleneck formed by the overlay of capacity mismatch, geopolitical constraints, and physical limits.

Cleveland Cliffs

USCLF

S

$Alibaba(BABA.US) T-Head mainly focuses on CPU and GPGPU, while Damo focuses on RISC-V. Training chips are most likely still handled by T-Head.

Alibaba

USBABA