$Super Micro Computer(SMCI.US)

Supermicro’s $60 Billion AI Backlog: Is This the Start of a New Growth Era?

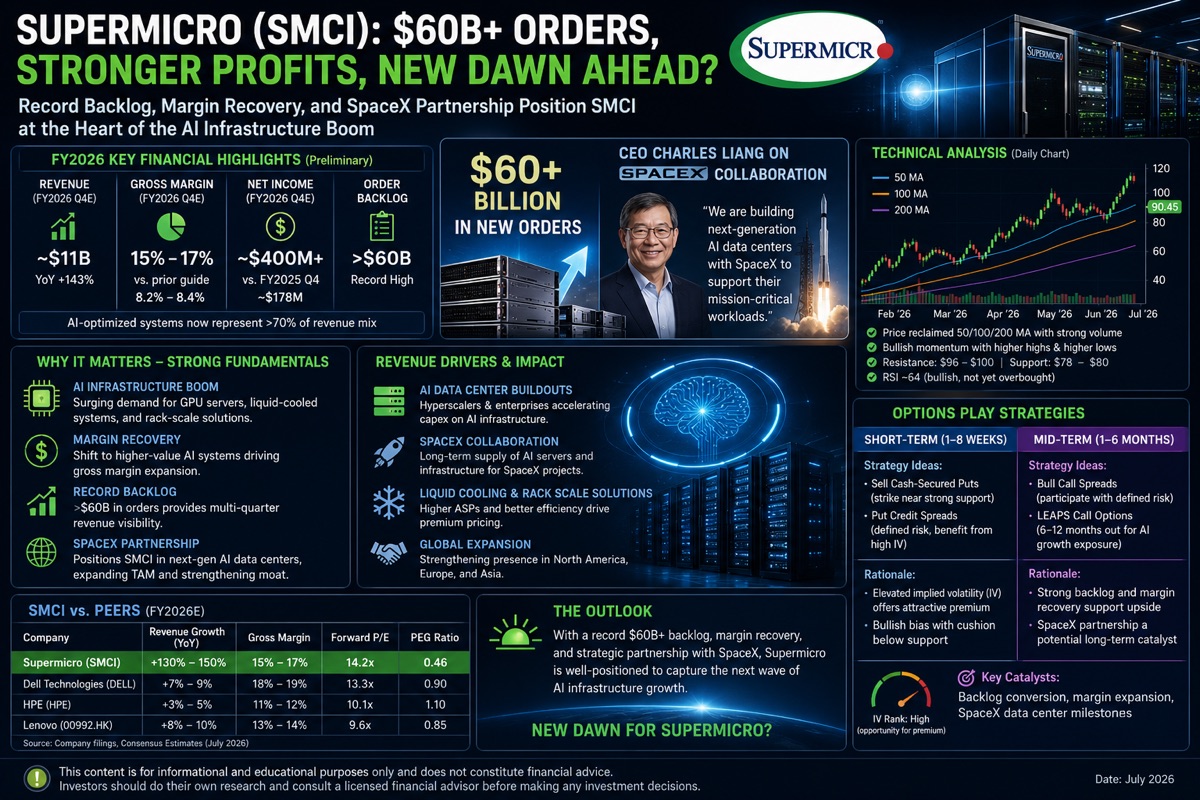

Super Micro Computer $Super Micro Computer(SMCI.US) may be entering its strongest growth cycle yet. The company disclosed a record over US$60 billion AI infrastructure backlog, while preliminary FY2026 Q4 results pointed to revenue approaching US$11 billion and gross margins recovering to 15–17%, a sharp improvement from prior guidance. The recovery suggests pricing power is returning as high-value AI systems become a larger share of sales.

CEO Charles Liang also highlighted Supermicro’s collaboration with SpaceX to build next-generation AI data centres, reinforcing the company’s evolution from a server manufacturer into an end-to-end AI infrastructure provider. This expands its addressable market and differentiates it from peers such as Dell, HPE and Lenovo, which remain more exposed to traditional enterprise hardware refresh cycles.

Technically, SMCI has regained bullish momentum after reclaiming key moving averages on improving volume, although near-term volatility remains elevated following its sharp rally. Fundamentally, a record backlog, recovering margins and AI infrastructure demand improve earnings visibility and could mark a new dawn for the company.

For options investors, the short-term favours selling cash-secured puts or put credit spreads to capitalise on elevated implied volatility, while mid-term investors may consider bull call spreads or LEAPS call options to participate in continued AI-driven upside with defined risk. Strong execution on the SpaceX initiative and backlog conversion could become the next catalyst for sustained share price appreciation.

This article is for educational purposes only and should not be considered financial advice.