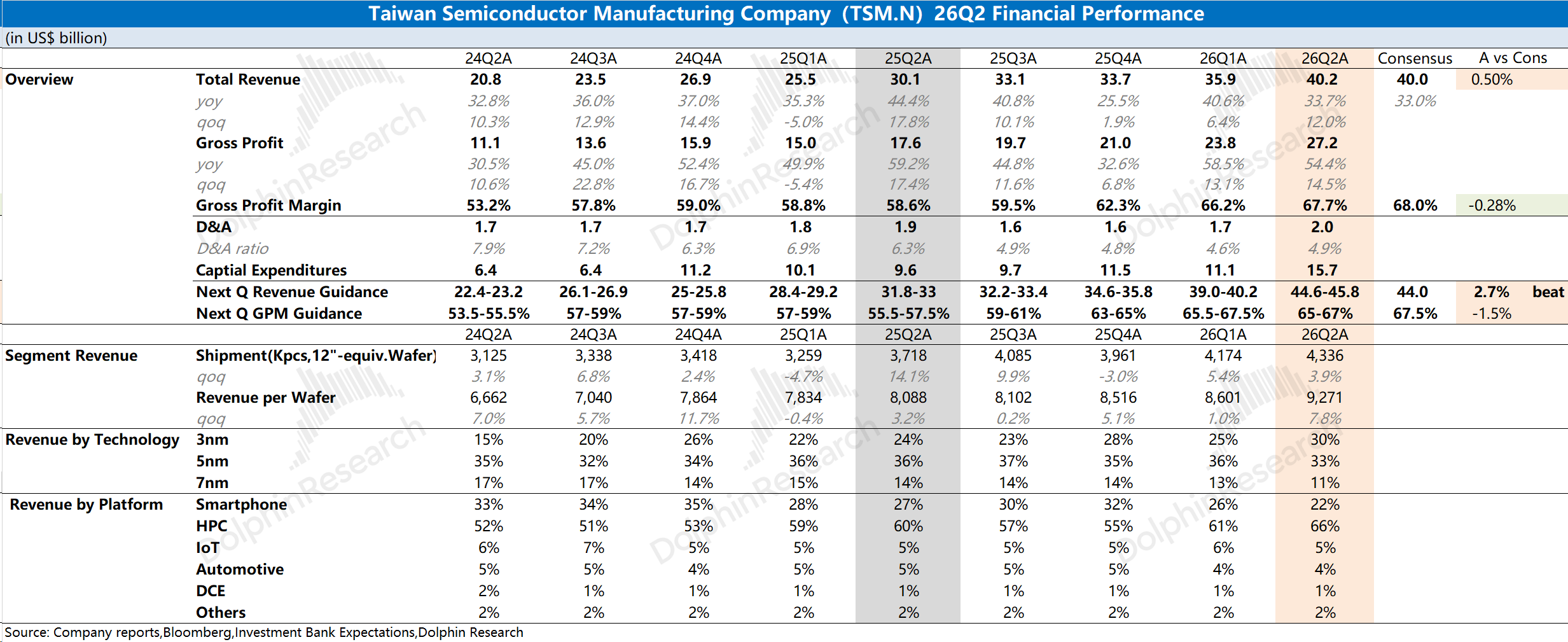

TSMC 26Q2 First Take: with the AI market in need of a confidence boost, this print is unlikely to satisfy. As the company discloses monthly ops data, revenue came in at $40.2bn, broadly in line with buy-side expectations (~$40bn).

Versus the top line, investors focused on gross margin. GPM was 67.7%, at the top end of guidance but slightly below raised buy-side expectations (some aggressive marks were 69%+).

Margins are still on an upward trend, driven by higher utilization and pricing. N5 and below have been running at >100% utilization, while rush orders lifted ASPs, with some orders carrying >50% premiums.

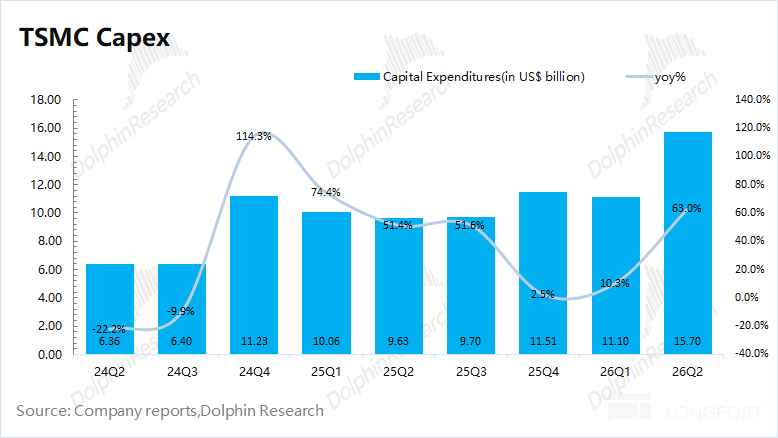

With fab loading tight, the company has more incentive to lift capex. Management raised capex to $60-64bn (from the higher end of $52-56bn), well above the Street at $58bn. This implies H2 capex of $33.2-37.2bn (+56%-75% YoY), aligning with ASML’s back-half-weighted revenue outlook.

On the outlook, next-quarter revenue is guided to $44.6-45.8bn, with GPM at 65%-67%. Since TSMC provided full-year growth guidance, the importance of next-quarter guidance is reduced. Management lifted the FY revenue growth target to 40% (vs. at least 30% prior), slightly above mainstream expectations (35%+).

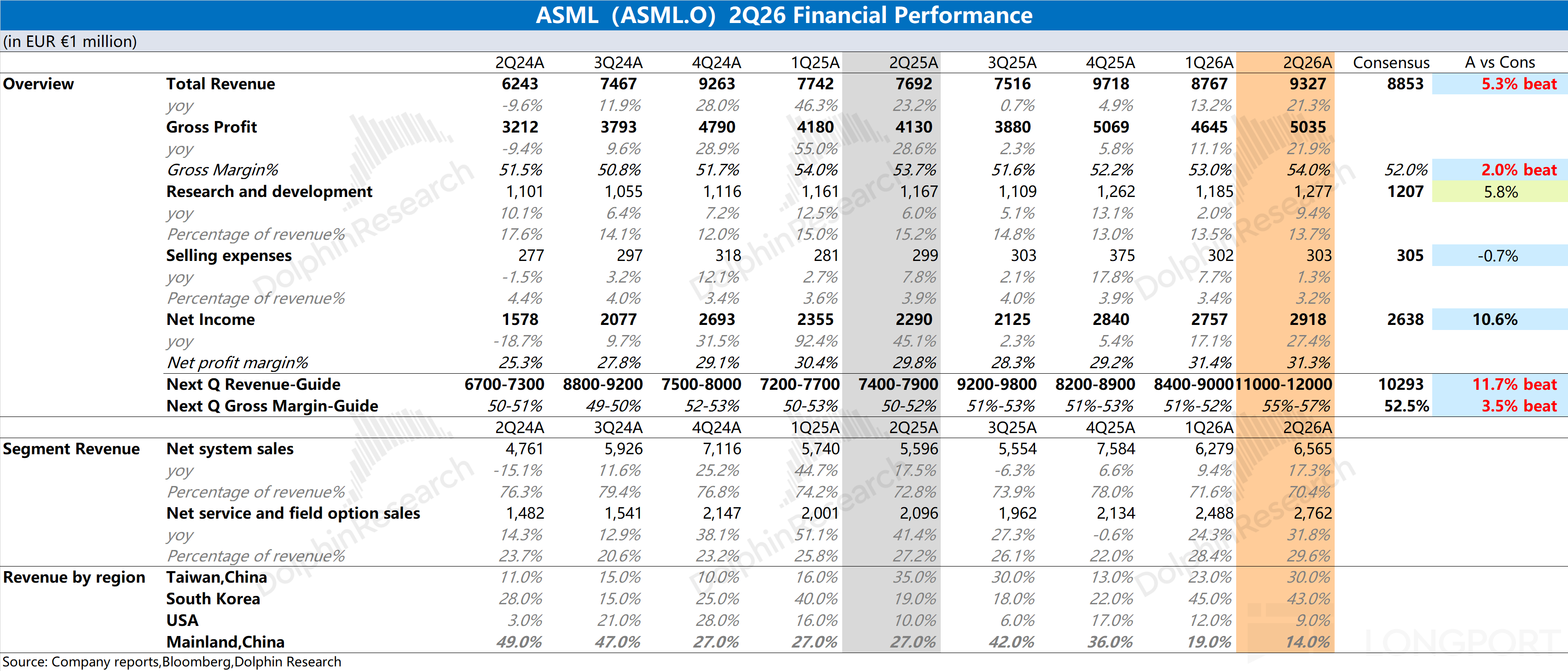

Overall, the market had hoped for a more dazzling report to inject confidence into the AI supply chain, but the print and outlook did not deliver a big beat. Among the metrics, only capex clearly topped expectations, a relative positive for upstream equipment names such as ASML. For more, stay tuned for Dolphin Research’s follow-up take and transcript highlights. $Taiwan Semiconductor(TSM.US)