$Lululemon(LULU.US)

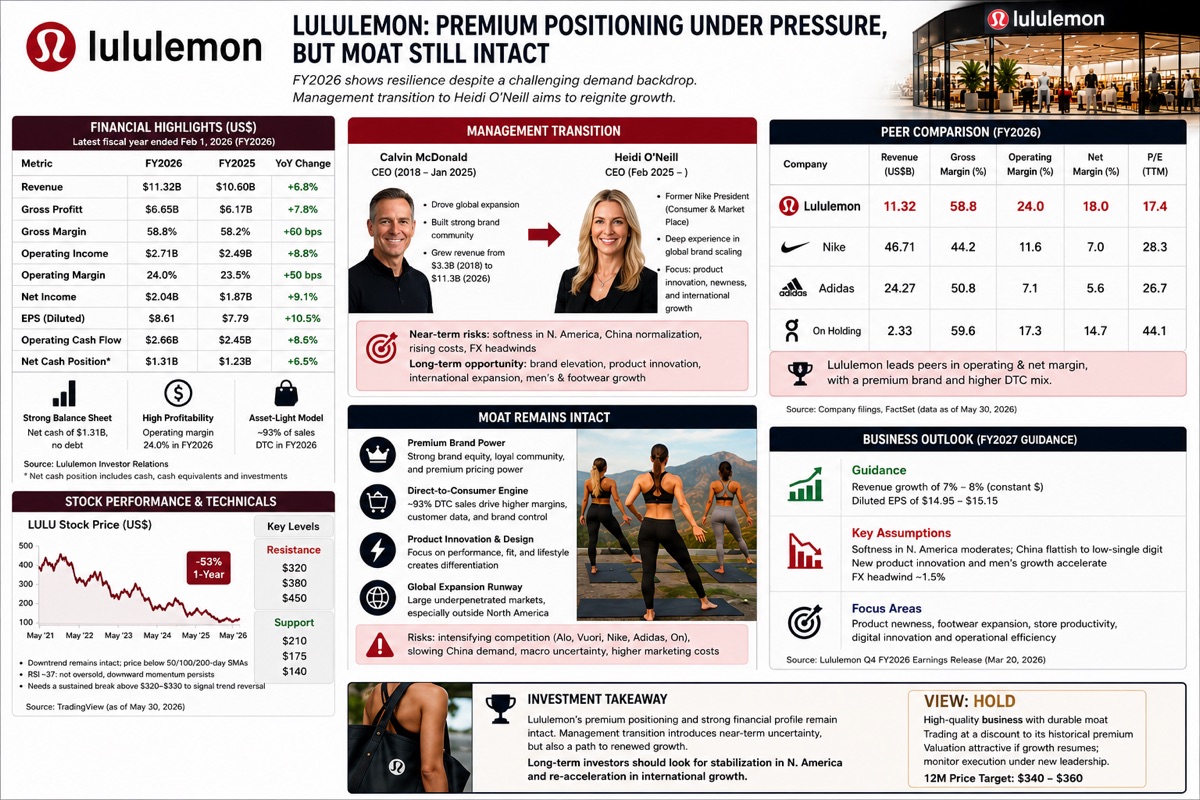

Lululemon’s share price has been punished as investors question whether its premium athleisure moat is fading. The transition from Calvin McDonald to former Nike executive Heidi O’Neill adds execution risk, but also offers an opportunity to reinvigorate product innovation and global expansion. FY2025 revenue reached US$11.1 billion, while Q1 FY2026 revenue rose 4% to US$2.5 billion, although comparable sales grew just 1% and management acknowledged softer demand in North America. (Lululemon)

Its moat remains differentiated. Unlike Nike, Adidas and On, Lululemon dominates the premium yoga and lifestyle apparel niche through direct-to-consumer sales, strong community engagement and premium pricing, producing margins that still exceed most peers. However, competitors including Alo, Vuori and traditional sportswear brands are narrowing the innovation gap, while China—once its growth engine—is showing signs of slowing. (Financial Times)

Fundamentally, Lululemon still boasts a debt-light balance sheet, healthy cash generation and a sizeable net cash position. Technically, the stock remains in a long-term downtrend after losing over half its value, suggesting investors should wait for a sustained higher-high pattern before turning bullish. The business remains highly relevant, but the next 12 months will determine whether management can restore product momentum and prove that its premium brand still commands pricing power.