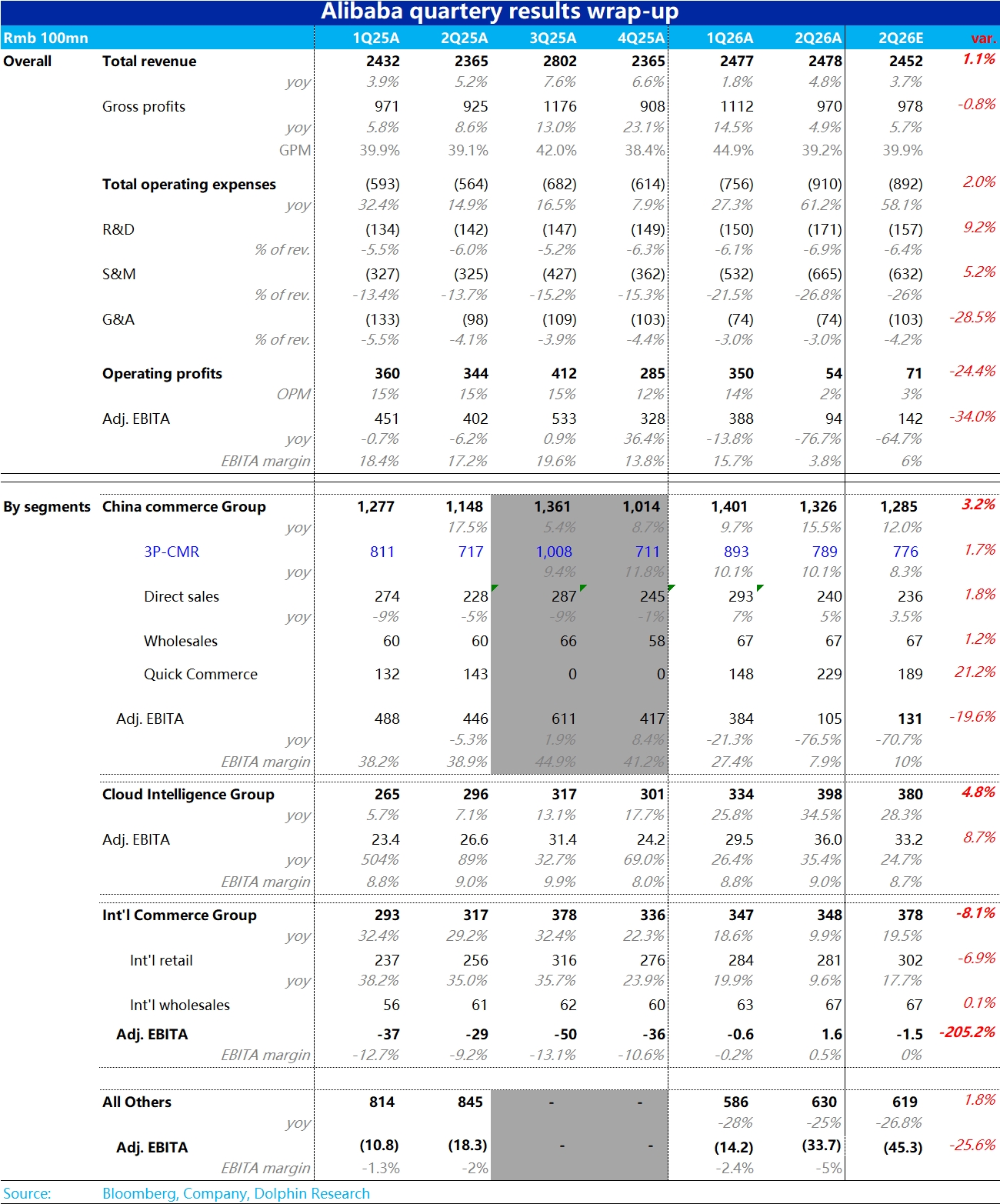

Alibaba F2Q26 Quick Interpretation: The two most concerning issues for the market this quarter—losses caused by food delivery and the growth of the cloud business. For the former, our estimates suggest a loss of around 39 billion, which is at the upper end of the company's previous guidance range, making it an expected but unfavorable news.

Meanwhile, the growth rate of cloud business revenue exceeded expectations, accelerating to 34.5%, with the profit margin remaining flat year-on-year, stronger than the already high expectations.

Bloomberg's consensus forecast for this quarter was not updated in time, thus having limited reference value. Dolphin Research will consider the latest expectations from major institutions:

1) The core Taobao and Tmall business's CMR year-on-year growth rate is 10.1%, consistent with last quarter's growth and in line with market expectations. Considering the base period from last September when a 0.6% merchant service fee was added, the performance is still decent, though not surprising.

2) Including food delivery and travel services, the new Taobao and Tmall (domestic e-commerce group) reported an adj. EBITA of 10.5 billion this quarter, with food delivery losses decreasing by 76.5% year-on-year. The latest major institutions' expectations range from about 7.5 to 10 billion, with actual performance at the upper end of expectations, not as concerning as feared.

3) Another key indicator, Alibaba Cloud's revenue grew by 34.5% year-on-year this quarter, stronger than the market expectation which had been raised to over 30%, making it the most unexpected point of this performance.

However, after excluding internal demand from the group, Alibaba Cloud's growth rate accelerated by 3 percentage points quarter-on-quarter, not as strong as it appears overall. In other words, this quarter, Alibaba's internal demand for cloud services was also stronger.

4) The International E-commerce Group's revenue grew by about 10% this quarter, continuing to slow down significantly. However, the corresponding adj. EBITA for this quarter has already turned positive to 160 million, aligning with the previous shift towards refined operations to improve limited profitability. (Too much investment in food delivery and cloud, indeed leaving no room for overseas business investment).

5) All other bundled businesses reported a loss this quarter, expanding significantly from over 1 billion last year and last quarter to nearly 3.4 billion. However, major institutions had generally raised their loss expectations to 5 billion, with actual losses slightly less. This mainly reflects investments in Gaode's street view ranking and AI 2C directions like Quark and Qianwen. $Alibaba(BABA.US) $BABA-W(09988.HK) $BABA-WR(89988.HK)

The copyright of this article belongs to the original author/organization.

The views expressed herein are solely those of the author and do not reflect the stance of the platform. The content is intended for investment reference purposes only and shall not be considered as investment advice. Please contact us if you have any questions or suggestions regarding the content services provided by the platform.