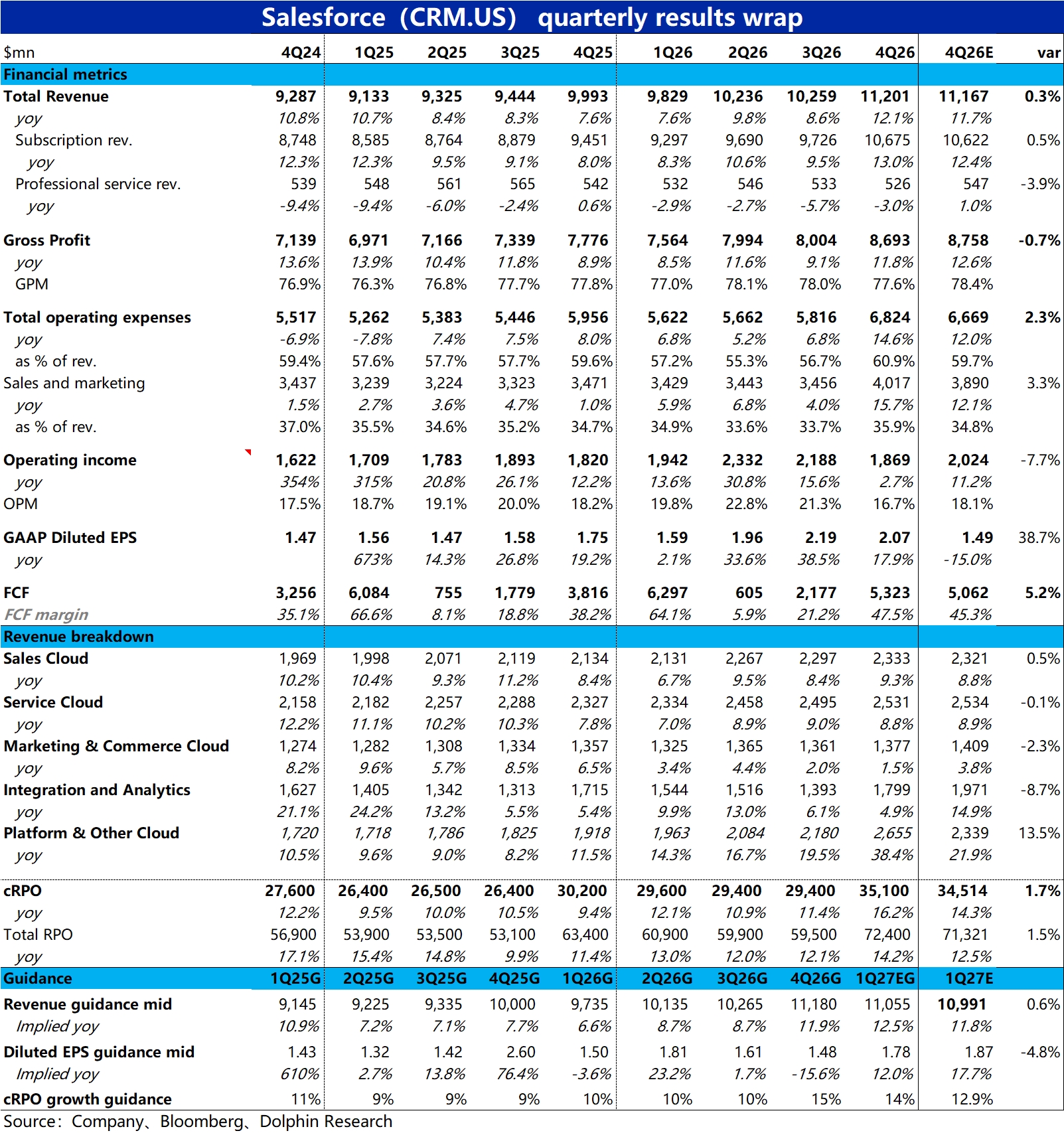

Salesforce 4Q26 First Take: Results were broadly lackluster. Revenue growth ticked up as expected, with no upside surprise, while GPM stayed under pressure and expenses rose sharply across the board, driving a notable GAAP OP miss. cRPO growth also fell short of buyside expectations, skewing market reaction negative.

1) Total revenue and subscription revenue rose 11% and 10% YoY cc, respectively, both accelerating by 2ppt QoQ. Roughly 4ppt of that lift came from consolidating Informatica, underscoring soft underlying growth. Versus expectations, the print merely matched.

2) Across the five major product lines, all segments except Platform (which absorbed Informatica) saw cc growth that was slightly slower vs. last quarter or at best flat. Again, core organic momentum failed to improve.

3) cRPO ended the quarter at $35.1bn, up 13% YoY cc, which appears 2ppt faster than last quarter. However, consolidation contributed about 4ppt, and buyside was looking for 14%–15%, implying a miss.

4) Profitability weakened: GPM declined YoY and QoQ, likely dragged by AI workloads such as Agentforce that carry heavier compute and lower margins. Total opex growth re-accelerated to ~15% YoY (after years in single digits), above both Street expectations and revenue growth, with R&D, S&M, and G&A all moving higher. With growth soft and spend rising, OPM contracted by 1.5ppt YoY.

5) Guidance (cc): next-quarter total revenue +10%–11% YoY, a slight uptick similar to this quarter, with consolidation still a 4ppt tailwind and roughly in line with Bloomberg consensus. cRPO is guided to grow 13%, same as this quarter, showing no acceleration. Diluted EPS guidance is ~5% below Bloomberg, leaving little to cheer on either the top line or the bottom line. $Salesforce(CRM.US)

The copyright of this article belongs to the original author/organization.

The views expressed herein are solely those of the author and do not reflect the stance of the platform. The content is intended for investment reference purposes only and shall not be considered as investment advice. Please contact us if you have any questions or suggestions regarding the content services provided by the platform.