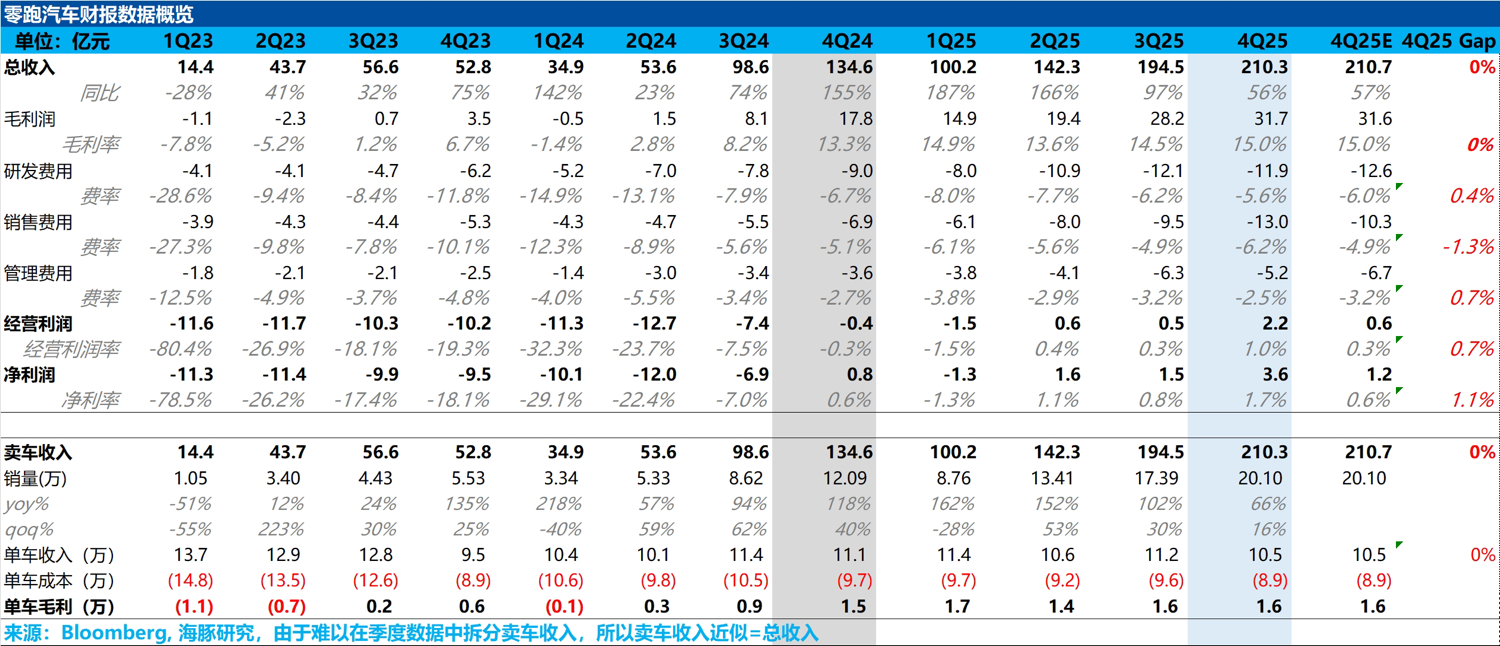

Leapmotor 4Q25 First Take: the company delivered a solid, in-line quarter. It demonstrated steady operating discipline.

Management had guided that heavier promotions would offset scale benefits, leaving GPM flat QoQ. That set a conservative bar.

However, GPM still rose 50bps QoQ to 15%. Despite lower ASPs due to promotions and a mix shift toward lower-priced models, the QoQ uptick was driven by three factors.

Drivers included ongoing cost-down through platformization and in-house R&D/manufacturing, and further scale effects. In Q4, other income also lifted GPM; with faster overseas ramp, carbon credit revenue recognition likely doubled vs. last quarter.

On opex, sales expense was RMB 1.3bn, up QoQ on heavier ad spend and concurrent network expansion. R&D and admin were well controlled and declined QoQ. OP reached RMB 220mn, above the market’s ~RMB 60mn expectations. $LEAPMOTOR(09863.HK)

The copyright of this article belongs to the original author/organization.

The views expressed herein are solely those of the author and do not reflect the stance of the platform. The content is intended for investment reference purposes only and shall not be considered as investment advice. Please contact us if you have any questions or suggestions regarding the content services provided by the platform.