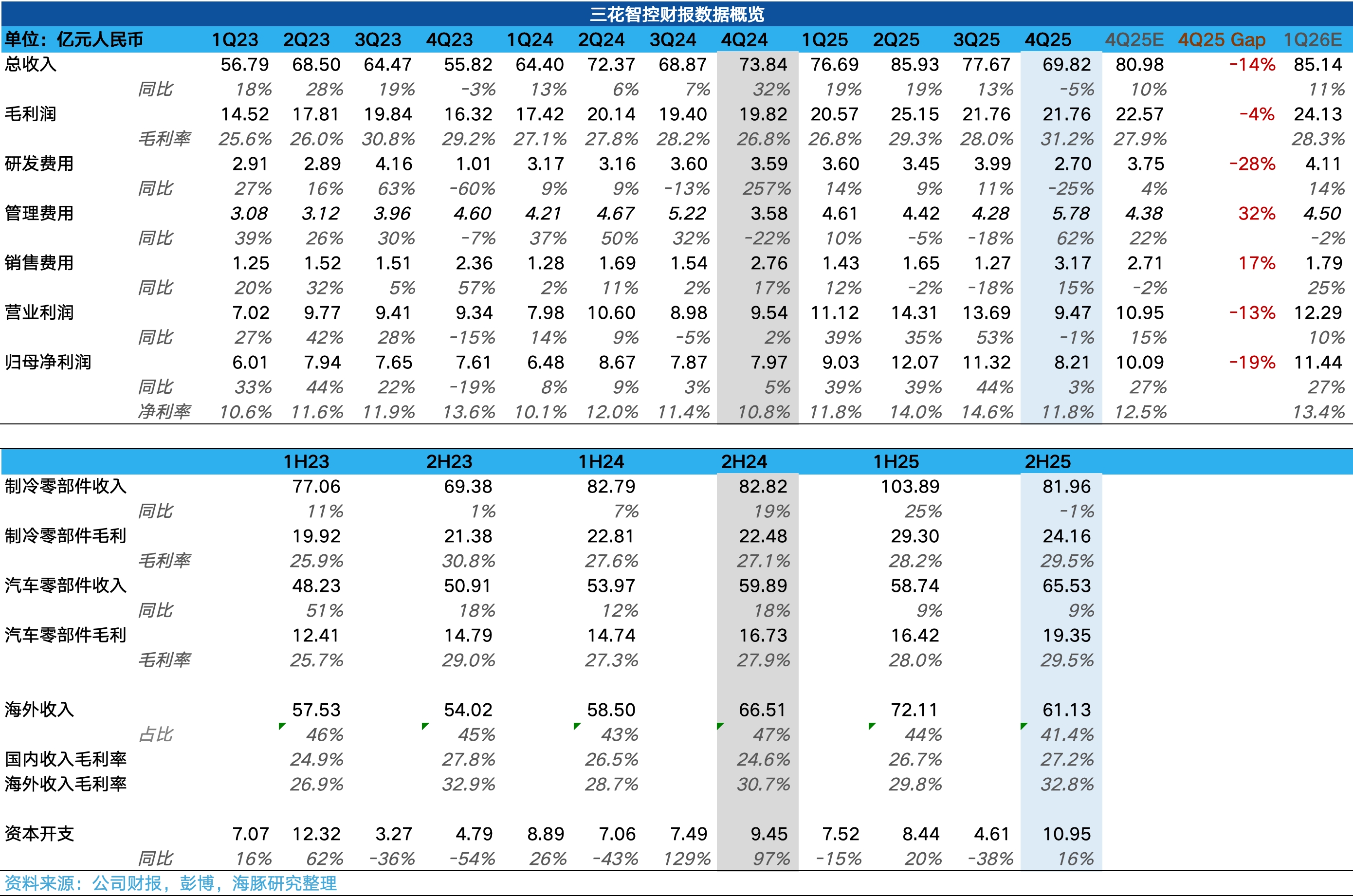

4Q25 First Take: results landed toward the lower end of the pre-announced range, near the floor and below the Street. On revenue, the main drag came from overseas sales in refrigeration, which declined YoY in 2H—particularly in Q4—likely due to U.S. tariff policy.

In detail. Key takeaways follow.

1) Q4 headline financials: revenue was approx. RMB 1bn below consensus, the biggest driver of the profit miss. Mgmt and selling expenses ran above market expectations, while R&D spend was lower, all pointing to external industry pressure. That said, single-quarter GPM reached 31.2%, showing some earnings resilience.

2) Refrigeration: 2H revenue fell 1% YoY. Since Q3 growth was positive, Q4 must have turned negative YoY.

Weakness started in Q3 and became more visible in Q4, partly on a high base from 2024 state subsidies, but mainly due to overseas tariffs, especially the U.S. special tariffs on 'steel derivative products' effective from Jun. The tariff impact weighed on shipments in the quarter.

However, localization is progressing with plants in Mexico, Thailand, and the U.S. ramping. We view the current situation as a transitory pain.

3) Auto parts: performance was also middling, with 2H YoY growth under 10%, well below NEV industry growth, and Q4 YoY revenue growth likely slowing vs. Q3. The softness likely reflects customer mix, notably weaker Q4 sales at a major North American client.

Diversification is reshaping the customer base. The top customer contribution fell to 10.90% in 2025 from 12.62% in 2024.

4) New biz: the humanoid robot line was not separately disclosed, suggesting a small revenue contribution. For data centers, the company repeatedly highlighted project execution in the report, making this a segment to watch.

5) Overall: Q4 missed Street expectations, driven more by industry factors (policy cycles, trade frictions) and customer mix than by internal execution. With capacity localization and customer diversification underway, this looks like a transition period.

Importantly, the ceiling in traditional refrigeration and auto parts is getting closer, so investors should focus on progress in robots and data centers. $Sanhua(002050.SZ) $SANHUA(02050.HK)

The copyright of this article belongs to the original author/organization.

The views expressed herein are solely those of the author and do not reflect the stance of the platform. The content is intended for investment reference purposes only and shall not be considered as investment advice. Please contact us if you have any questions or suggestions regarding the content services provided by the platform.