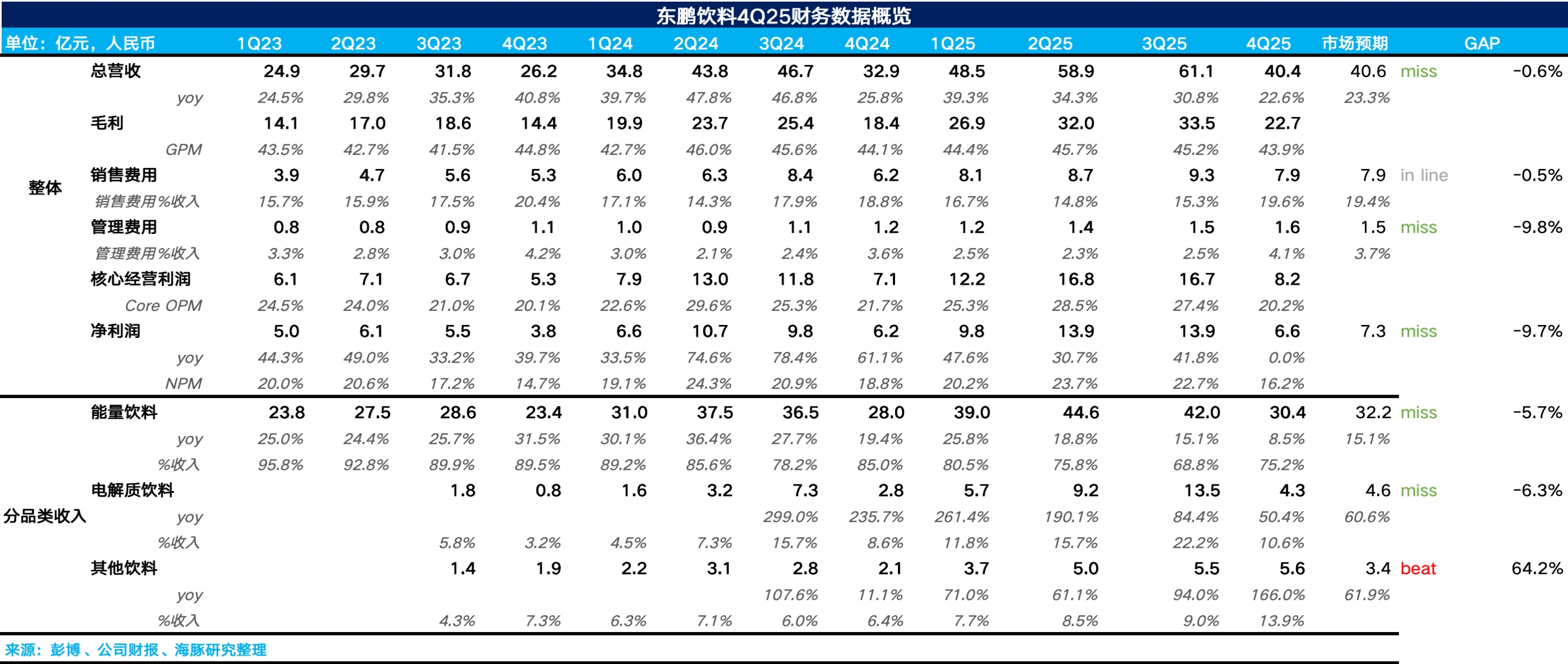

Dongpeng Bev. 4Q25 First Take: Overall, Q4 results remained weak. The core energy drink base continued to decelerate.

By category, energy drinks delivered revenue of RMB 3.0bn (+8.5% YoY). Growth slowed further from Q3, marking the first single-digit print in nearly three years.

As Dolphin Research has flagged, the energy drink category is nearing a ceiling, so growth is naturally easing.

The 'second growth curve' electrolyte drinks posted revenue of RMB 430mn (+50% YoY). Sequential momentum also moderated. Versus the prior ~200% growth, the print is uninspiring.

The only beat came from 'other beverages', up 166% YoY with QoQ acceleration. Dolphin Research believes products such as Daka coffee and Guo Zhi Cha fruit tea, leveraging channel reuse and rapid roll-out, delivered high growth.

By region, the company changed its disclosure basis. Based on channel checks, Guangdong and Guangxi, after years of cultivation and deep distribution, are near a ceiling and grew only low single-digit. Stronger showings came from West and North China, where terminal outlet expansion continues.

On profitability, GPM slipped 20bps to 43.9% on a mix shift toward lower-margin electrolyte water and other beverages. With heavier cooler deployment in Q4, the S&M ratio rose 50bps YoY. Core OPM fell 150bps to 20.2%, missing expectations. For more detail, please see Dolphin Research's take. $EASTROC BEVERAGE(605499.SH) $EASTROC(09980.HK)

The copyright of this article belongs to the original author/organization.

The views expressed herein are solely those of the author and do not reflect the stance of the platform. The content is intended for investment reference purposes only and shall not be considered as investment advice. Please contact us if you have any questions or suggestions regarding the content services provided by the platform.