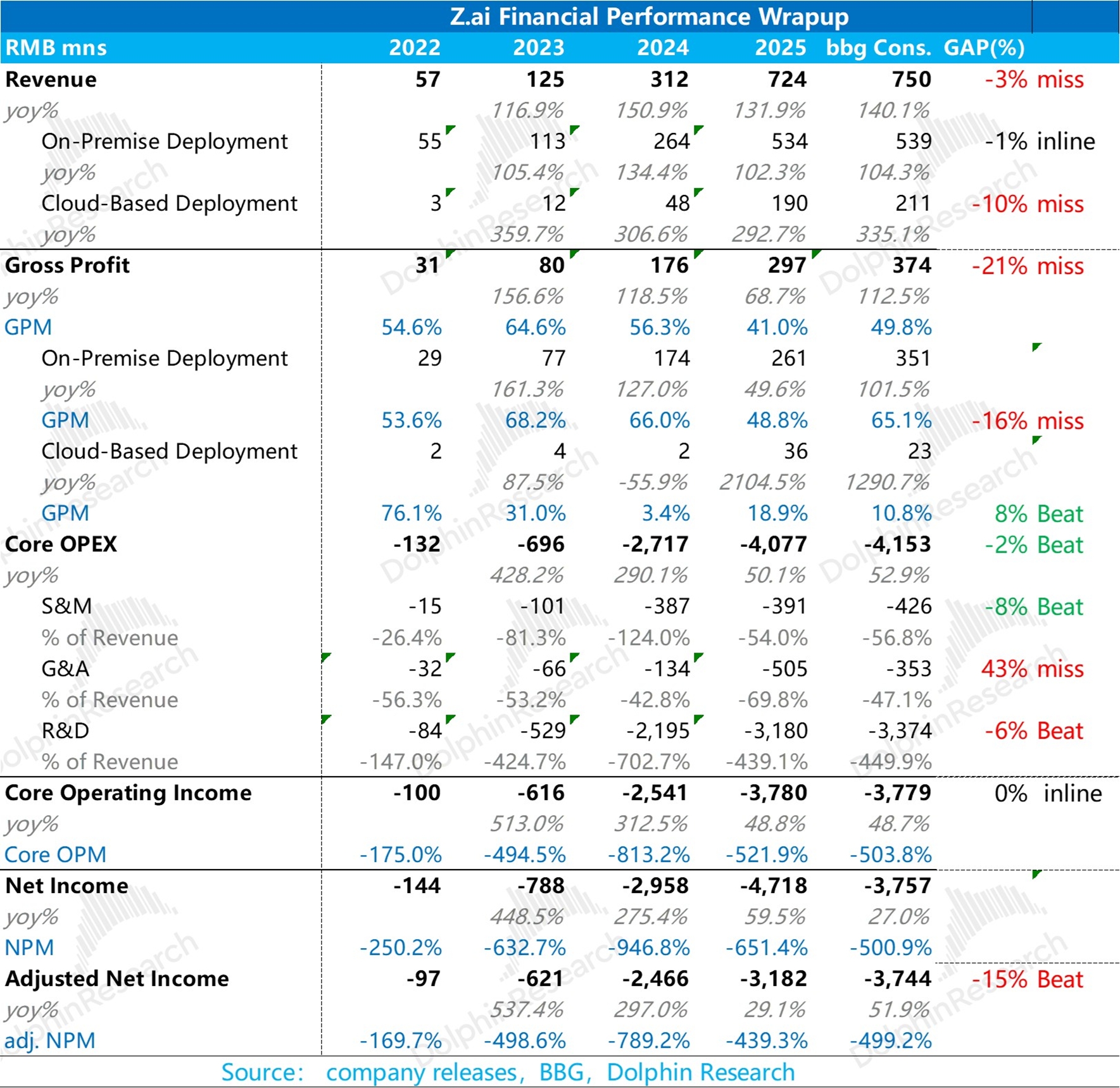

Zhipu 2H25 First Take: a sixfold move in a quarter as the model star stock steals the show. Headline growth reads as a 99% surge in 2H25 revenue, but the underlying picture is fairly muted.

The market clearly priced in an upgrade from on-premise deployments to a standardized, cloud-based sales model. Execution is underway and broadly in line with expectations.

The main issue lies in GPM mix: while on-premise deals face less brutal price competition than open-access APIs, delivery intensity drove up costs. As a result, this higher-margin line, accounting for 70% of 2H25 revenue, saw GPM fall from 59% in 1H to 44% in 2H.

On opex, compute investment was split roughly evenly between halves and remains outsized, totaling RMB 3.2bn for the year, vs. just RMB 720mn of FY25 revenue. The imbalance is stark.

Against this backdrop, movements in the other two expense buckets — sales expenses declining in absolute terms and G&A still growing fast — are footnotes. For 2H overall, relative to the share price rally, there was little in the print worth highlighting.

That said, the market at current valuations appears indifferent to model losses, focusing instead on the scarcity of model 'intelligence' and token consumption.

Since Lunar New Year, the company rolled out the GLM-5 base model, the agent-focused Turbo model for 'Lobster', and the coding-oriented GLM-5.1. Its intelligence benchmark is aligned with top overseas models like Claude Opus. More importantly, Zhipu has been raising prices, with subscription plans up ~30–50% and API rates up over 80%.

Since mid-Feb, the 3x rally already reflects optimism about the business model upgrade. Dolphin Research is more keen to see post-Feb trends in token consumption after the new models and price hikes, but the company did not disclose this in the release; we will watch for color on the call. $KNOWLEDGE ATLAS(02513.HK)

The copyright of this article belongs to the original author/organization.

The views expressed herein are solely those of the author and do not reflect the stance of the platform. The content is intended for investment reference purposes only and shall not be considered as investment advice. Please contact us if you have any questions or suggestions regarding the content services provided by the platform.