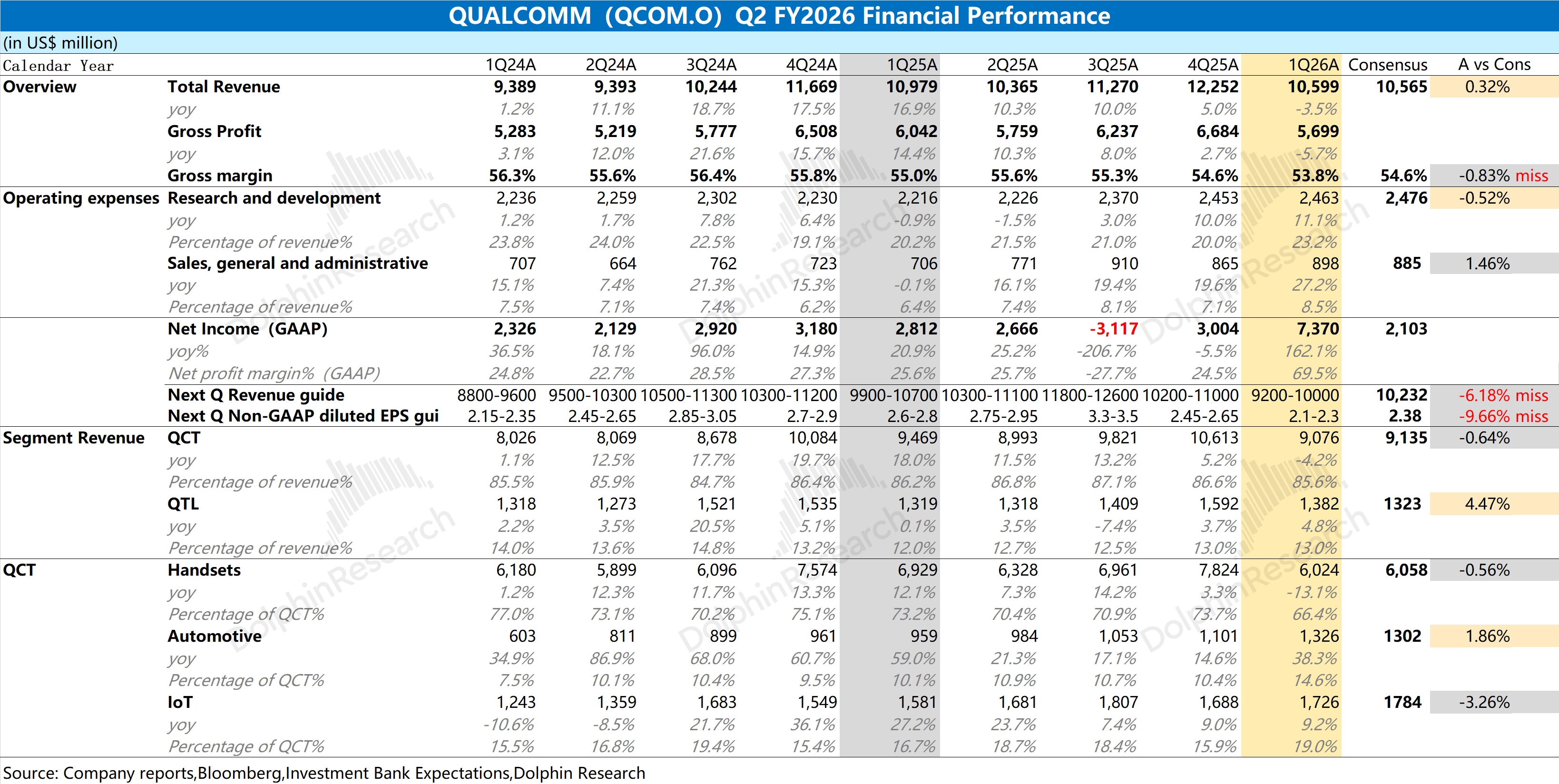

QCOM Q2 FY26 First Take: Revenue was in line with market expectations, while the decline in GPM was driven by a weak downstream handset market and memory shortages/price hikes. These factors weighed on margins in the QCT hardware segment.

Outside the quarter, guidance for next quarter remains soft. The company guides revenue of $9.2–10.0bn, below the Street’s $10.2bn, and Non-GAAP EPS of $2.10–2.30, also below $2.38. This points to continued pressure on revenue and GPM next quarter.

The largest drag comes from handsets: the company expects next-quarter handset revenue of about $4.9bn, down over 20% YoY, mainly due to tight memory supply. Memory shortages continue to bite and the handset market remains sluggish. Apple’s ongoing in-house baseband development also adds pressure for Qualcomm.

The prior share price decline suggests these headwinds are largely understood and priced in. In other words, current results are weak and the market already knows it.

Therefore, even a below-consensus guide is having a diminishing impact on the stock. Versus sluggish legacy businesses, investors are more focused on Qualcomm’s AI progress, including data center AI and on-device AI.

Recent reports of an on-device AI collaboration with OpenAI sparked a double-digit rally in the shares. As long as management delivers more AI partnerships or order updates, it should add to market expectations. For more details, stay tuned for Dolphin Research’s follow-ups and call Trans. $Qualcomm(QCOM.US) $GraniteShares 2x Long QCOM Daily ETF(QCML.US)

The copyright of this article belongs to the original author/organization.

The views expressed herein are solely those of the author and do not reflect the stance of the platform. The content is intended for investment reference purposes only and shall not be considered as investment advice. Please contact us if you have any questions or suggestions regarding the content services provided by the platform.