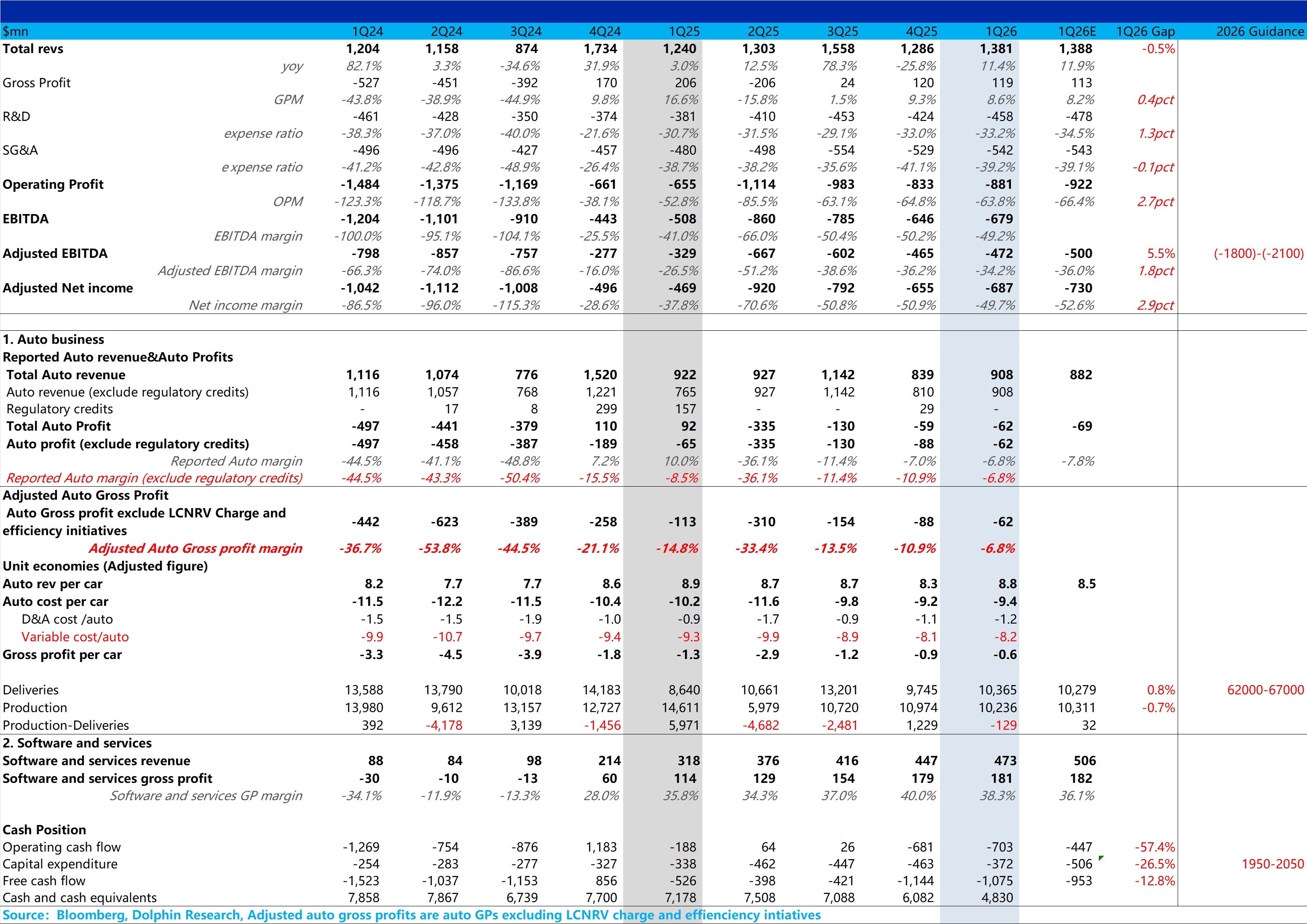

RIVN 1Q26 First Take: Overall, Rivian delivered a decent print. Revenue was roughly in line with estimates, while GP and net loss came in slightly better. Details below:

① Vehicle revenue reached $900 mn, above the $880 mn consensus. ASP was $88k, up from $83k in the prior quarter (+$5k), likely on improved mix (lower EDV share) and some pullback in promo discounts. ASP also topped the market’s $85k estimate.

② Vehicle GPM kept improving QoQ, rising from -10.9% to -6.8% (+410 bps), slightly better than the market’s -7.8% expectation. The ASP uplift offset drag from reduced scale benefits.

③ Adj. EBITDA was -$470 mn, better than the -$500 mn consensus, supported by stronger GP and disciplined R&D spend. Adj. EBITDA margin ticked up QoQ by ~200 bps to -34.2%. However, vs. this print, investors are more focused on R2, a lower-priced volume model, including ramp speed and margin implications; please stay tuned for Dolphin Research’s take and Trans. $Rivian Automotive(RIVN.US)

The copyright of this article belongs to the original author/organization.

The views expressed herein are solely those of the author and do not reflect the stance of the platform. The content is intended for investment reference purposes only and shall not be considered as investment advice. Please contact us if you have any questions or suggestions regarding the content services provided by the platform.