BIDU 1Q26 First Take: Q1 was mixed, a tale of two halves, reflecting recent strategic shifts and a business pivot. With legacy ads already structurally weak, investors seem more focused on whether AI Cloud, Kunlun Chip and buybacks are tracking to plan.

As most sell-side models still follow the old framework, Dolphin Research blends the old and new to surface expectation gaps. This also helps show growth in BIDU's new AI lines.

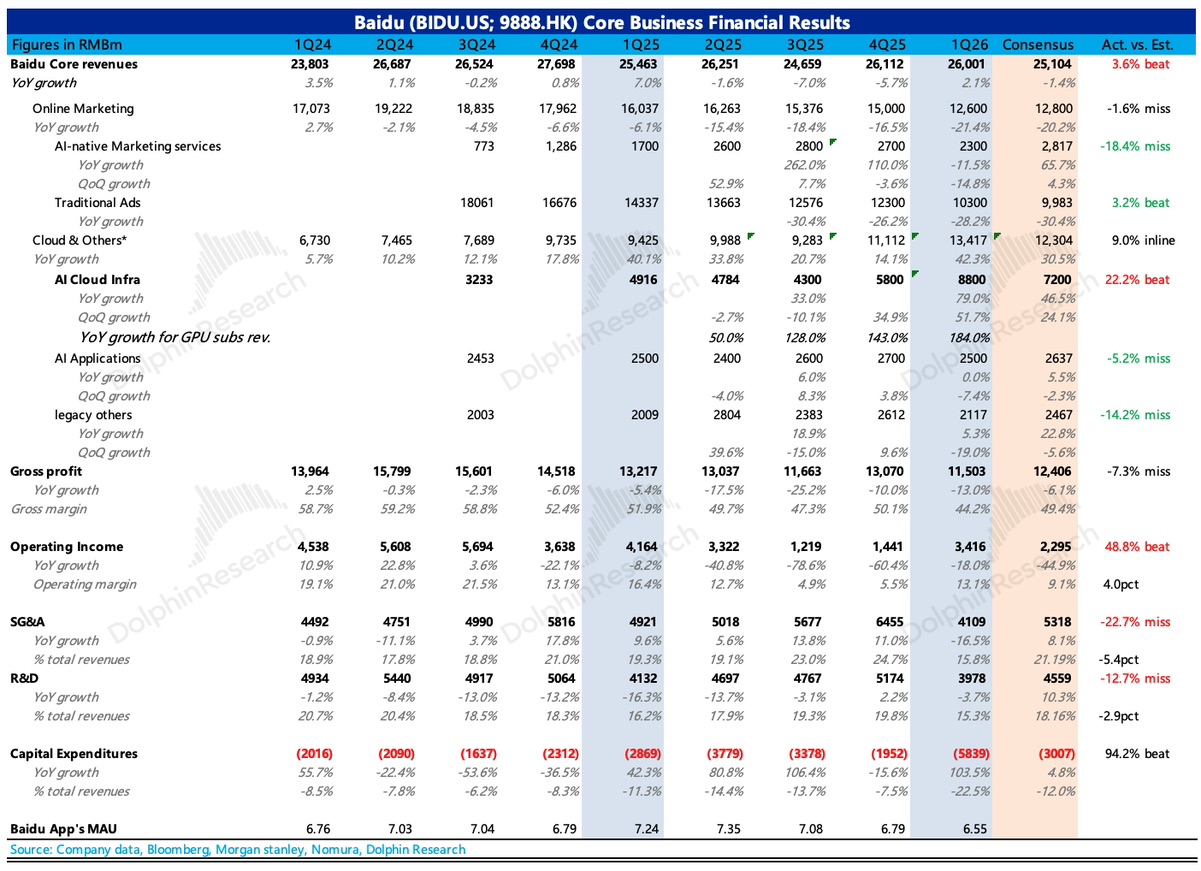

1) Highlights first: the pillars delivered.

(1) AI Cloud beat. Q1 revenue was RMB 8.8bn (+79% YoY), vs. sell-side at RMB 7.0–8.0bn; GPU compute revenue rose 184% YoY.

(2) Opex dropped sharply, margins improved. Notably, opex as a share of revenue fell to 31% from 45% in Q4, largely on lower personnel costs.

SBC tells the same story: stock-based comp fell 24% YoY in Q1. With a higher market cap vs. last year, this implies a sizable reduction in headcount eligible for awards.

Using the old framework, Dolphin Research roughly split margins for ads and cloud. Trend-wise, cloud margins appear to have improved.

2) Pain points: are AI apps losing steam?

(1) Legacy ads -28%. This was expected and there is little to add. Holiday timing played a role, but macro pressure and strategic shifts reflected in headcount changes suggest no inflection yet.

(2) AI apps and AI-native ads are losing momentum. Sequentially they fell 7% and 12%, and AI app revenue (incl. Baidu Wenku, autonomous driving, cloud drive and digital employees) slowed to flat YoY, which is out of sync with industry strength. We flagged this last quarter, likely driven by competition.

3) Buybacks started, likely constrained by CNY and blackout. The two-year $5bn program announced in Feb saw $172mn repurchased in Q1 (roughly one month), which looks a bit light on pacing; we will watch the call for plans ahead.

That said, management appears more committed to shareholder returns this time. With net cash of ~RMB 100bn (ex short-term borrowings) and ample FCF, we expect execution as planned.

4) Investment stepping up. Q1 capex nearly doubled YoY to RMB 5.8bn. Still low vs. other model/cloud majors, and AI Infra revenue of RMB 8.8bn alone more than covers capex.

5) Watch for commentary on Kunlun Chip's IPO plan on the call. In early May, Kunlun Chip completed IPO coaching registration; on a typical timeline, listing could be completed by end-Q3. Given the early filing (submitted in early Jan), a mid-to-early Q3 listing is also possible.$Baidu(BIDU.US)$BIDU-SW(09888.HK)

The copyright of this article belongs to the original author/organization.

The views expressed herein are solely those of the author and do not reflect the stance of the platform. The content is intended for investment reference purposes only and shall not be considered as investment advice. Please contact us if you have any questions or suggestions regarding the content services provided by the platform.