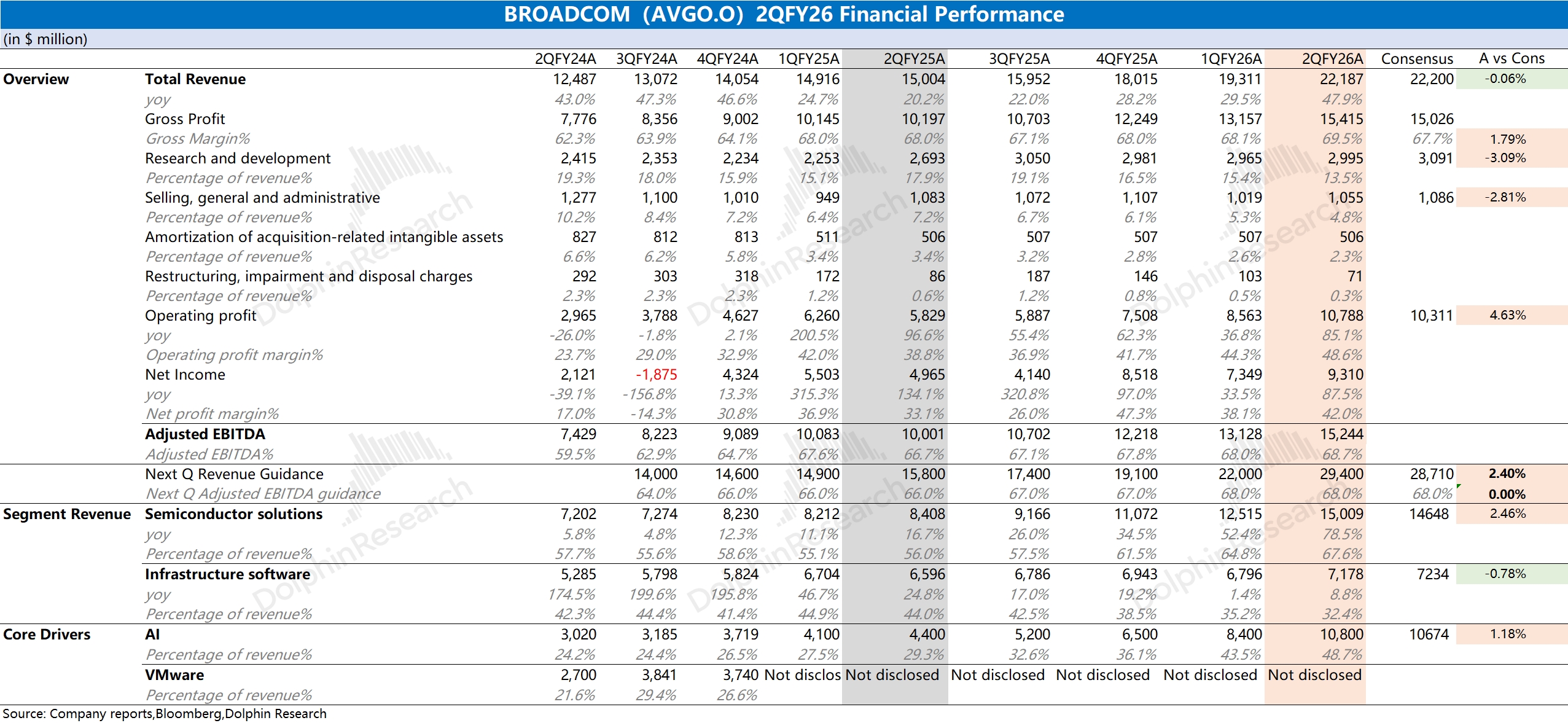

AVGO First Take: revenue and GPM were broadly in line with the Street. Growth was mainly driven by AI.Ex acquisition amortization and restructuring, underlying GPM was 76%, roughly flat QoQ. Over the medium term, a higher mix of lower-margin ASICs could still weigh on overall margins.

For next quarter, management guides revenue to $29.4bn, up $7.2bn QoQ. This is slightly above the Street at $28.7bn, with growth largely from AI.

Leverage (Total Debt/LTM Adj. EBITDA) fell to 1.8x. The debt impact from the VMware acquisition has been absorbed within two years.

AI remains the focal point: the company delivered $10.8bn of AI revenue this quarter, up $2.4bn QoQ. It guides next quarter AI revenue to $16.0bn, up $5.2bn QoQ, below the Street’s $17.0bn.

Because the Anthropic partnership is shifting from full-rack purchases to chip sales, the Street had already trimmed Anthropic’s contribution to AVGO. Even so, management’s guide, while showing faster AI growth, is still below mainstream houses’ lowered expectations.

On the other hand, management guides AI revenue of $56bn for this FY and $100bn+ for next FY, which is unexciting. In fact, most Street models are already at $130bn+ for next FY.

Overall, AVGO’s AI biz. is still accelerating. Backed by orders from Google’s TPU program and Anthropic, and by its strength on the networking side, it should continue to gain AI share. The market is bullish on its high growth, but guidance in this print was underwhelming.

Against high-growth expectations, a relatively soft guide may weigh on sentiment and valuation near term. AI revenues are still accelerating, and the story in AI semis and connectivity remains intact. For more, follow Dolphin Research’s upcoming First Take and Trans. $Broadcom(AVGO.US)

The copyright of this article belongs to the original author/organization.

The views expressed herein are solely those of the author and do not reflect the stance of the platform. The content is intended for investment reference purposes only and shall not be considered as investment advice. Please contact us if you have any questions or suggestions regarding the content services provided by the platform.