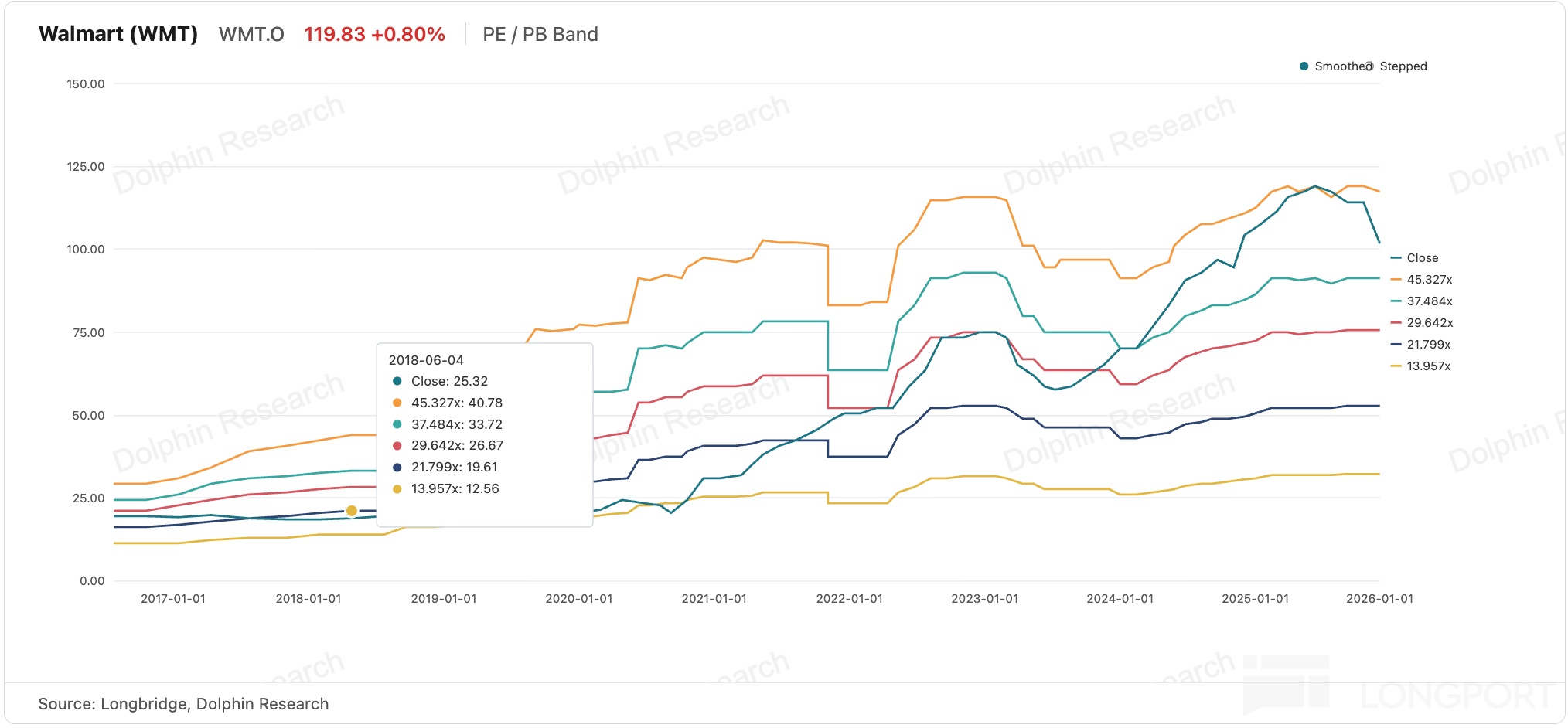

WMT: Still Going Strong; How Much Longer Can the Rerating Run?

This is the final piece in our Walmart series, focusing on what the investment is actually worth. Let's get straight to it.

From our top-to-bottom review, the retail veteran has evolved well beyond a legacy model built solely on everyday low prices and dense store coverage. $Walmart(WMT.US) is no longer just a traditional brick-and-mortar giant.

Its value breaks cleanly into three layers.

Base layer: a wide-moat offline retail core in the U.S. and Intl., delivering moderate growth and highly resilient cash flows. It builds an uncopyable moat through store density, purchasing scale, and supply chain control. This is the valuation foundation and the infrastructure that enables upper-layer platforms.

Middle layer: the long-undervalued Sam's Club. In the U.S., it is the third growth engine catching up with Costco. In today’s consumption environment, it is growing close to 40% in China, becoming a rare localization template amid the domestic retail red ocean.

Top and most elastic layer: atop the self-run retail base, a platform economy of 3P merchants, ads, and membership. It is asset-light with high GPM, and still has headroom for monetization.

Walmart’s rerating from an old-school offline retailer to an omnichannel retail-plus-platform story reflects two shifts. First, a renewed appreciation for offline retail assets and the post-Covid second wave of online gains for global retailers. Second, the profit unlock and revaluation from asset-light online 3P platform economics.

The questions now are how far this rerating has run and how much is left. This note focuses on answering that.

I. What is Walmart’s investment value?

We have one last question to settle: what is a retailer with very strong offline defense, rising online optionality, and a thickening profit mix actually worth today. That is the crux for this large-cap compounder.

The challenge is the lack of a single yardstick. Do we assign Target-like 15x PE for a mature, low-growth retailer, Costco-like 50x PE for a sticky membership warehouse, or simply borrow Amazon’s retail plus ad platform framework. Any single multiple will be misleading.

The core reason is that Walmart reports by U.S., Intl., and Sam’s, but each segment mixes very different economic assets. There is heavy-asset, low-GPM, scale-driven 1P retail across stores and 1P e-comm, alongside asset-light, high-GPM, faster-growing platform businesses such as 3P marketplace, ads, and membership. There are also still-lossmaking but market-priced strategic stakes like Flipkart and PhonePe in India.

Therefore, we re-cut Walmart by business model rather than geography and apply SOTP. Heavy-asset retail is valued on EV/EBIT vs. Kroger/Target/Costco, while the asset-light platform is valued on discounted forward profits vs. Amazon.

Let’s break it down piece by piece.

1) Offline retail core — the strategic foundation

a) Walmart U.S.

Start with the core base. The U.S. store network is already highly saturated, so the scale expansion dividend is largely harvested.

Penetration into lower- and middle-income cohorts is near a ceiling. In offline grocery and consumables, Walmart holds a dominant 20%+ share.

Our view: the U.S. offline core is a mature business unlikely to return to high single-digit growth. With mild inflation pass-through and incremental mix upgrades, a 3–4% mid-cycle revenue CAGR is the base case.

In FY2026 (year-end 2025), Walmart U.S. generated $483 bn in total revenue. With e-comm at 20% penetration, the implied e-comm revenue is $96.6 bn.

Given the 1P model mirrors physical retail economics — Walmart buys inventory, holds stock, takes obsolescence risk, and books revenue on a gross basis — and a large portion of 1P orders fulfill through stores via BOPIS and store-ship, we combine store sales and 1P e-comm. We then value the integrated omnichannel retail model on EV/EBIT.

Sell-side checks suggest 1P accounts for roughly 90% of e-comm, or about $87 bn. Importantly, Walmart U.S. is not a generic mature retail asset but a foundation asset with a deep moat. Roughly 90% of Americans live within reach of its stores, reinforced by unmatched purchasing scale, supply chain efficiency, and the everyday low price brand promise.

This moat explains why, unlike many Chinese offline retailers that struggled against online disruption, Walmart preserved its base and cash flows despite Amazon’s pressure. On a 1P EBIT margin of 4.2% (ex-3P and ads) and 3.5% growth, FY2027 EBIT is ~$20 bn.

Crucially, the 1P/store base underpins all high-margin platforms. The 3P marketplace’s traffic and store-warehouse fulfillment, ad audiences, and the Walmart+ value proposition all rest on nearly 200 mn weekly active store shoppers, scale procurement, and the fulfillment grid. With 1P e-comm losses narrowing and margins normalizing, we assign a premium to traditional retailers.

We apply 25x EV/EBIT vs. 12–15x for peers, implying enterprise value of about $550 bn.

b) Sam’s Club (U.S.)

As discussed, Sam’s is pushing digital, but its online business is largely a 1P model of curbside pickup and delivery. The contribution from 3P marketplace and ads is minimal for now.

We therefore value Sam’s as a whole against warehouse club comps Costco and BJ's Wholesale. The approach aligns with its business model.

In FY2026, Sam’s U.S. revenue was $93 bn. With continued gains from private label Member’s Mark and digital, Sam’s is growing faster than Walmart’s mature core as it closes the gap with Costco.

Mgmt. targets a doubling of members, sales, and profit over 8–10 years, implying 7–9% CAGR. On a mid-case of 8% FY2027 revenue growth and EBIT margin lifting to 2.6% on better member mix, FY2027 EBIT is about $2.6 bn.

On valuation, Costco trades at 30–35x EV/EBIT and BJ at 15–18x. Given Sam’s sits between the two on sales density and member quality, and is converging toward Costco, we assign 25x EV/EBIT, implying EV of roughly $65 bn.

c) Intl.

Before forming a view, we make two normalizations. Add back the one-off non-cash PhonePe equity comp of about $0.7 bn, and add back Flipkart’s operating losses of roughly $0.8 bn that we value separately.

That yields FY26 Intl. offline retail EBIT of about $6.6 bn. (Note: PhonePe is a digital payments firm in India and Flipkart is a 3P marketplace; both are Walmart-controlled, akin to Alipay and Taobao.)

Driven by high-quality Walmex, fast-growing Sam’s China, and Canada, Intl. grows faster than the mature U.S. core. We assume 7% growth in FY2027, flat vs. last year, implying EBIT of $7.1 bn.

On valuation, Intl. quality sits between Walmex and more volatile EM retail. It merits less than the 25x certainty premium of the U.S. core but more than the 8–10x of generic EM retail. We assign 15x EV/EBIT, implying EV of about $106.5 bn.

2) 3P marketplace + ads + membership — the high-margin platform

Before modeling, we size each piece and benchmark against Amazon. The central question is how close Walmart’s platform monetization can get to Amazon’s by 2030.

3P marketplace: Third-party data from Market Pulse suggests Walmart’s 3P GMV is about $18 bn, roughly 11% of its e-comm GMV. Amazon, after two decades, has 3P at roughly 70% of GMV.

Walmart’s DNA is still 1P buyer-merchant, and marketplace only began to scale around 2020. Building merchant trust is a marathon, so we assume 3P mix rises by 1–2ppts per year to about 15–20%.

On take rate, Walmart is using lower fees to win sellers from Amazon. We assume a take rate of 18–20%, below Amazon’s ~30% ex-ads.

Ads (Walmart Connect): In 2025, global ad revenue was $6.4 bn, up 46% YoY. The ad-to-GMV penetration is about 3.9%, less than half of Amazon’s 8.3%.

As noted in our prior piece, Walmart is still in the early monetization window. With superior ROI for merchants at this stage, we assume ad penetration continues to rise toward Amazon’s level over time.

Membership (Walmart+): 2025 Walmart+ revenue was roughly $2.6 bn, up 15% YoY. Launched only five years ago, Walmart+ remains far less penetrated than Prime with similar service pillars.

We assume Walmart+ grows broadly in line with GMV, driven by value positioning among lower- to middle-income households. This anchors our mid-case.

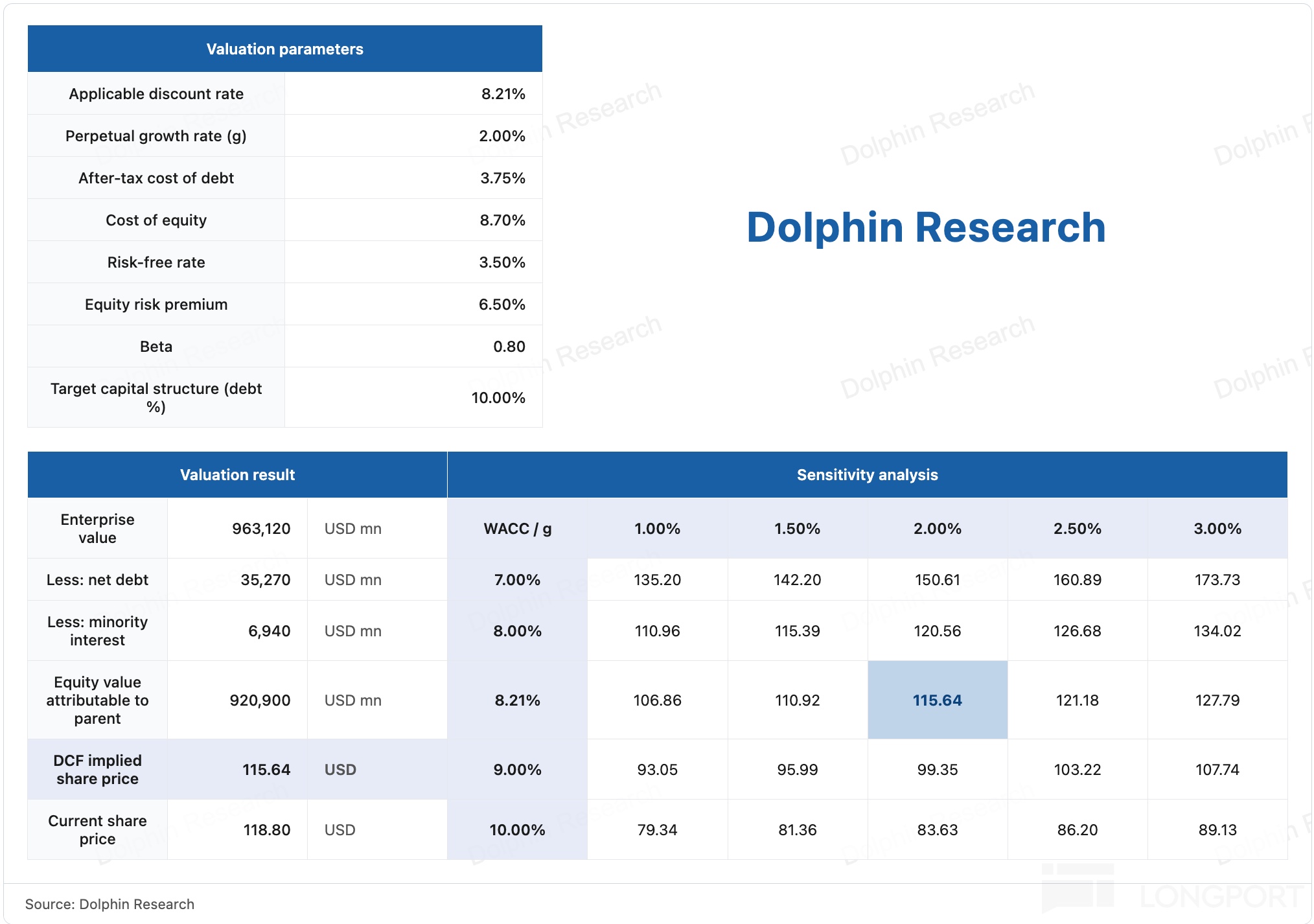

Given these businesses are still early in profit release, we value them on mid-cycle 2030 operating profit and discount back at an 8.2% WACC. We run bear, base, and bull scenarios for key assumptions.

At a current market cap of about $950 bn and net debt of roughly $35 bn, EV is about $985 bn. Netting out the offline store retail, Sam’s, and Intl. EV of about $723.5 bn plus the separately valued India digital assets at $38.3 bn leaves an implied $223.2 bn for the platform trio.

This is broadly in line with our base-case value of $235.5 bn. It suggests that with a premium already ascribed to the offline U.S. 1P foundation for its moat, the market prices the platform flywheel around a base-case outcome.

In other words, platform monetization is more upside optionality than the main pillar of today’s valuation. Given 3P is still relatively small, we stay cautiously optimistic and do not underwrite the bull case into fair value yet.

We cross-check with a DCF, which aligns closely with the SOTP. Assuming a steady revenue CAGR of about 5%, the base case embeds a steep margin ramp.

As ads and membership, both high-GPM, scale up, company-level OPM would need to lift from 4.3% to 7.4% over five years, or about +62 bps per year, to support the current price. That is a demanding trajectory.

This corroborates our SOTP conclusion. At today’s price, investors are not buying a low-growth retailer at a 4% margin but a structural margin expansion story.

For a near-$1 tn retailer growing mid-single digits, a +300 bps OPM lift over five years is a tall order. Delivery hinges on whether the high-margin ad engine scales as planned.

Put simply, both DCF and SOTP converge on the same takeaway: the premium you pay is a bet on flywheel-driven margin expansion. (Chart below shows the DCF under the base case.)

Takeaway: Not cheap, but not without reason

Practically, a more comfortable entry range would be $100–110, pressing PE below 35x. That roughly prices the platform flywheel between bear and base, offering better odds. At current levels, Walmart looks like a great company to track and hold long term, albeit at a full valuation.

<End>

Related Dolphin Research on Walmart:

Walmart: What Powers the Trillion-Dollar Retail Myth?

Walmart: The Veteran’s Surprise Charge into E-comm and the Rerating Logic

The Costco Inside Walmart: How Sam’s Club Scales, and the Counter-Play

Risk disclosure and statements for this article: Dolphin Research disclaimer and general disclosures

The copyright of this article belongs to the original author/organization.

The views expressed herein are solely those of the author and do not reflect the stance of the platform. The content is intended for investment reference purposes only and shall not be considered as investment advice. Please contact us if you have any questions or suggestions regarding the content services provided by the platform.