Competitive Landscape and Strategic Analysis of Leading Players in the Global Semiconductor Precursor Delivery System Market: Who is Defining 'Precise Delivery'?

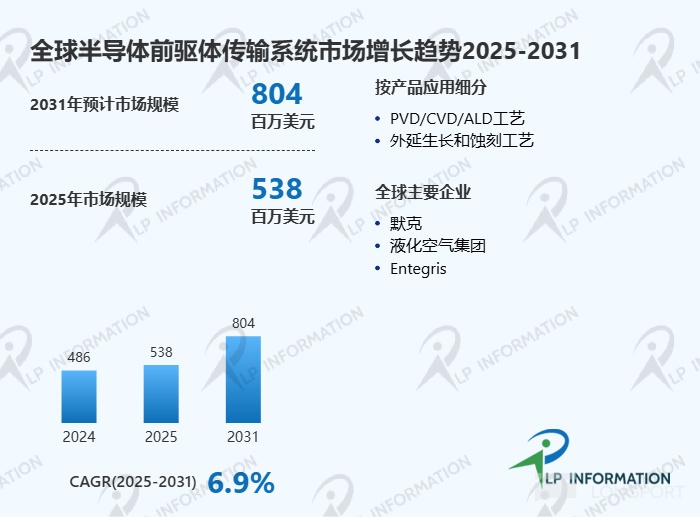

According to preliminary research data from market research firm LP Information, the global semiconductor precursor delivery system market size in 2024 is approximately US$486 million, and is expected to grow to US$804 million by 2031. The compound annual growth rate (CAGR) from 2025 to 2031 is estimated to be around 6.9%. Against the backdrop of continuous advancement in advanced process nodes and increasing complexity of thin-film deposition processes, this equipment segment is becoming a key growth area within the semiconductor manufacturing equipment system.

I. Product Definition and Industry Chain Structure: The "Chemical Delivery Nervous System" Supporting Advanced Processes

A semiconductor precursor delivery system is equipment used to deliver precursors, safely and precisely transporting liquid or solid precursors (such as silane, TEOS, tungsten hexafluoride, etc.) to the reaction chambers of Chemical Vapor Deposition (CVD) or Atomic Layer Deposition (ALD). Depending on the type of precursor, delivery systems can be categorized into Liquid Delivery Systems (LDS) and Solid Delivery Systems; while gaseous precursors are typically supplied via Gas Cabinet, gas panel, VMB/VMP.

The scope of this article does not include supply systems for gas delivery (such as Gas Cabinet, Gas Rack, etc.).

From the perspective of the industry chain, the upstream mainly includes suppliers of high-purity chemical materials, special metal materials (stainless steel, nickel-based alloys), precision valves, and sensors; the midstream consists of system integrators and equipment manufacturers responsible for designing and assembling high-reliability delivery systems; the downstream corresponds to wafer fabs and advanced process production lines, applied in logic chip, memory chip, and third-generation semiconductor manufacturing segments. This industry chain is characterized by high barriers, high cleanliness, and a strong certification cycle.

II. Technology Development Trends: Evolving Towards High Precision, Integration, and Intelligent Control

As process nodes advance to 3nm and beyond, precursor delivery systems are facing higher precision and more stringent safety requirements. Current technological evolution is mainly reflected in three directions:

First, enhanced multi-precursor collaborative delivery capability to support complex multi-layer thin-film structures (such as high-k dielectric stack structures);

Second, intelligent process monitoring, achieving closed-loop control through real-time optical and mass spectrometry monitoring to improve deposition uniformity;

Third, system integration development, with multi-process cluster tools reducing contamination risks and improving production line efficiency.

Simultaneously, corrosion-resistant materials and sealing technologies are also continuously upgraded to meet the demands of corrosive chemical delivery.

III. Market Structure Analysis: Europe and the US Dominate, China Accelerates Catching Up

The global market is highly concentrated within the European, American, Japanese, and Korean corporate systems. Among them, Merck Group and Air Liquide form the first tier, holding close to 40% of the market share; the second tier includes companies like Entegris, CSK, and Yake Technology, collectively accounting for over 40%.

Furthermore, Chinese companies such as Jingshi Technology are gradually breaking through the bottleneck of domestic substitution, achieving share gains in some mid-range application markets, but gaps remain in high-end processes and core material compatibility.

Regionally, Europe remains the world's largest production base, accounting for nearly 40%, while China, driven by policy support and fab expansion, has become one of the fastest-growing regions, with its market share expected to continue increasing in the future.

IV. Industry Policies and Supply Chain Environment: Domestic Substitution and Technology Security in Parallel

Against the backdrop of global semiconductor supply chain restructuring, US tariff policies and export controls have significantly impacted the flow of high-end semiconductor equipment and materials, prompting countries to strengthen their local supply chain security.

In China, policies promoting the domestic production of semiconductor equipment continue, supporting the autonomous and controllable development of high-end process equipment and key components, accelerating the introduction of domestic precursor delivery system manufacturers into fab production lines. Meanwhile, Europe and Japan maintain their advantage in the high-end market through technical standards and industry alliances.

V. Market Drivers: Advancement of Processes and Increased Material Complexity

Industry growth is primarily driven by the following factors:

First, the continuous evolution of advanced logic and memory chips towards smaller nodes, which constantly raises the precision requirements for precursor delivery;

Second, the expanding application of ALD and high-k materials, significantly increasing the demand for multi-precursor collaborative delivery;

Third, the rapid development of third-generation semiconductors (SiC, GaN) driving the expansion of new deposition processes.

Additionally, the global fab expansion cycle and increased capital expenditure also directly drive equipment demand.

VI. Market Obstacles: High Barriers and Long Certification Cycles Constrain Expansion Speed

Despite clear market prospects, the industry still faces multiple challenges:

First, high-purity chemical delivery systems have extremely high requirements for materials and sealing technology, resulting in a high R&D threshold;

Second, long customer certification cycles, typically requiring extended process validation periods;

Third, the high-end market has long been monopolized by international leaders, making entry difficult;

Fourth, the supply chain is significantly affected by geopolitics, creating uncertainty.

VII. Industry Development Opportunities: Resonance Between Domestic Substitution and Advanced Process Expansion

Future growth opportunities are mainly concentrated in three areas:

First, accelerated domestic substitution, providing an entry window for local Chinese equipment companies;

Second, advanced process expansion driving sustained growth in demand for high-end ALD/CVD systems;

Third, new materials and new structure chips (such as GAA transistors) driving increased process complexity, thereby stimulating system upgrade demand.

Simultaneously, with the rise of green manufacturing and safety standards, systems with high reliability and low pollution control capabilities will have a greater competitive advantage.

VIII. Regional Market Outlook: Asia Becomes the Growth Core

From a regional structure perspective, North America and Europe still dominate the high-end market, but Asia, especially China, is becoming the world's fastest-growing region. With continued fab expansion and the improvement of local supply chains, the Asia-Pacific region is expected to further increase its global market share in the coming years, becoming the core engine of industry growth.

IX. Conclusion

Overall, as a key "chemical infrastructure" in advanced processes, the semiconductor precursor delivery system market continues to expand alongside chip process upgrades. The future industry will follow three main development trends: "high precision, integration, and intelligence." Meanwhile, the competitive landscape will gradually evolve from European and American dominance towards multipolarity, with the market participation of Chinese manufacturers expected to continue increasing.

The copyright of this article belongs to the original author/organization.

The views expressed herein are solely those of the author and do not reflect the stance of the platform. The content is intended for investment reference purposes only and shall not be considered as investment advice. Please contact us if you have any questions or suggestions regarding the content services provided by the platform.