SRS Tax Benefits: Deferred Taxation Strategy Explained

Learn how Singapore's Supplementary Retirement Scheme offers three tax features: upfront contribution relief, tax-deferred growth, and reduced taxation on retirement withdrawals.

TL;DR: The Supplementary Retirement Scheme (SRS) offers Singapore residents three tax features: dollar-for-dollar tax relief on contributions, tax-deferred investment growth, and only 50% of withdrawals being taxable at retirement. Used as part of a planned approach, this deferred taxation structure may help reduce overall tax payable across working and retirement years, depending on individual circumstances.

Planning for retirement involves both tax efficiency and long-term saving. For Singapore residents, the Supplementary Retirement Scheme (SRS) provides a structured, government-backed pathway to reduce taxable income today while growing investments on a tax-deferred basis. Understanding the SRS tax benefits and how deferred taxation works is useful for anyone looking to manage their financial position over the long term. This guide breaks down exactly how the scheme works, who benefits most, and how to apply it effectively.

What Is the Supplementary Retirement Scheme?

The SRS is a voluntary savings scheme introduced by the Singapore government in 2001. It complements the Central Provident Fund (CPF) by allowing individuals to set aside additional savings for retirement, with tax incentives as the central feature. Unlike CPF, contributions to the SRS are entirely voluntary, and participants choose how much to contribute each year, up to the annual cap.

The scheme is open to Singapore Citizens, Permanent Residents (PRs), and foreigners residing in Singapore. SRS accounts can be opened at one of three appointed banks: DBS/POSB, OCBC, or UOB. You may only hold one SRS account at any time.

Why Deferred Taxation Matters

Deferred taxation means you pay less tax now and delay your obligations to a future date, typically when your income, and therefore your tax rate, is lower. For most working professionals, income peaks during their career years. By contributing to your SRS account and reducing taxable income during those higher-earning years, then withdrawing at a lower effective rate in retirement, you benefit from the difference in tax rates across your lifetime.

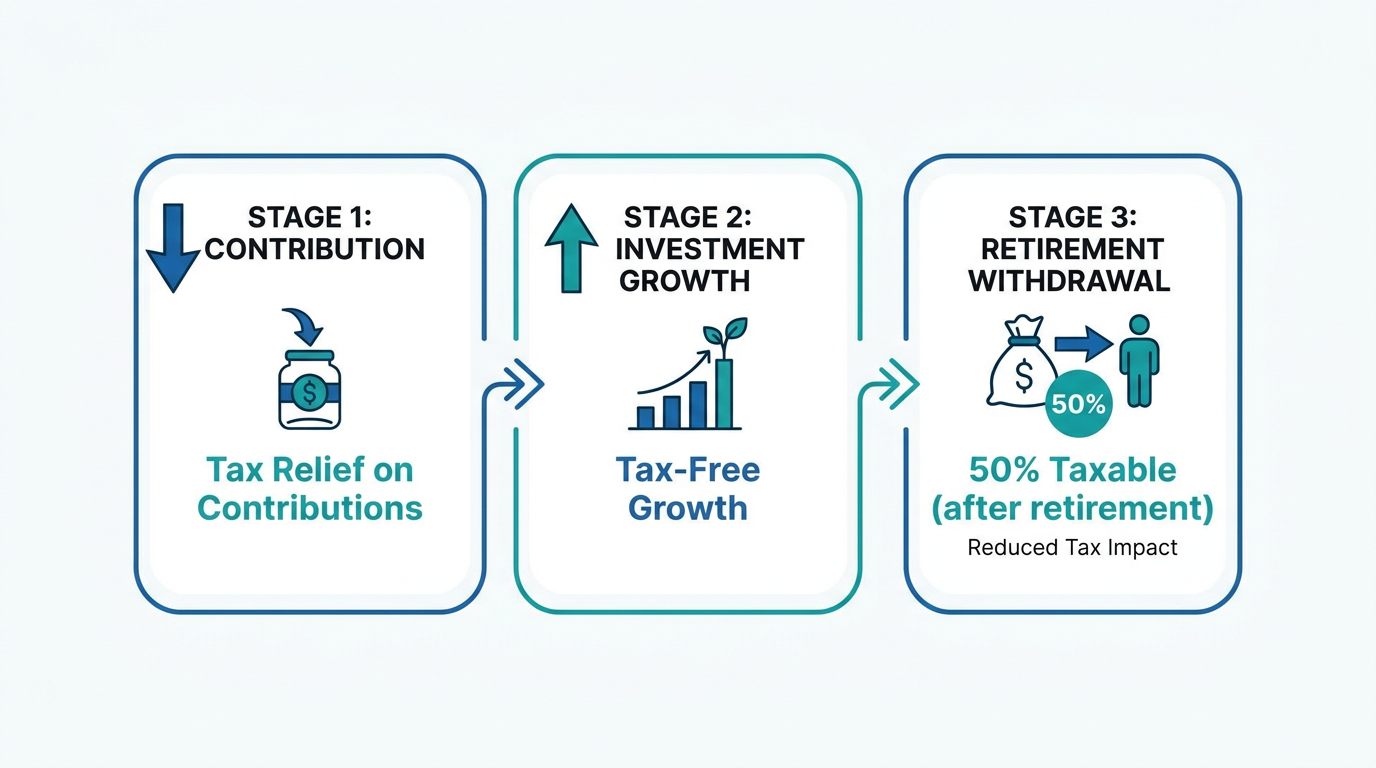

The Three Layers of SRS Tax Benefits

The SRS offers tax features across three stages. Each layer can work together to support your overall tax position.

Layer 1: Tax Relief on Contributions

Every dollar contributed to your SRS account reduces your chargeable income by the same amount. This dollar-for-dollar tax relief is automatically applied by the Inland Revenue Authority of Singapore (IRAS) based on information from your SRS operator. You do not need to file a separate claim in your income tax return.

According to IRAS, the annual contribution cap is SGD 15,300 for Singapore Citizens and PRs, and SGD 35,700 for foreigners. The higher limit for foreigners reflects the absence of CPF tax relief in their case.

Note: A personal income tax relief cap of SGD 80,000 per year applies to the combined total of all reliefs claimed, including SRS contributions.

Layer 2: Tax-Deferred Investment Growth

Funds inside your SRS account can be invested in shares listed on the Singapore Exchange (SGX), bonds, unit trusts, exchange-traded funds (ETFs), and qualifying insurance products. Dividends, interest, and gains generated are credited back into your SRS account and retain their tax-deferred status while held in the account. This allows your investments to compound without annual tax drag.

For guidance on selecting suitable SRS investment vehicles, you can explore SRS investment options and tax-advantaged fund guides or browse the resources available on the Longbridge Academy.

Layer 3: Reduced Taxation on Withdrawals

At retirement, only 50% of each SRS withdrawal is subject to income tax, according to IRAS. This concession, combined with the typically lower income of many retirees, means the effective tax rate on SRS withdrawals may be relatively low, though the actual outcome depends on your total income in each year. Withdrawals can be spread over up to 10 years from the date of your first penalty-free withdrawal, giving you flexibility to manage annual taxable income.

SRS Withdrawal Strategy: Maximising Tax Efficiency

When and how you withdraw from your SRS account has a significant impact on the overall benefit. Timing your withdrawals carefully is one of the most important aspects of an effective SRS plan.

Locking In Your Retirement Age

Penalty-free withdrawals are permitted from the statutory retirement age that was prevailing when you made your first SRS contribution. According to IRAS, this withdrawal age is fixed at the point of your first contribution and does not change even if Singapore's statutory retirement age is subsequently revised. For SRS members whose first contribution was made while the prevailing statutory retirement age was 62, the penalty-free withdrawal age remains 62. Because this age is locked in at the time of your first contribution, the rules that applied then continue to govern your withdrawals.

Withdrawing before your locked-in statutory retirement age incurs a 5% penalty on the withdrawn amount, and the full amount, rather than just 50%, becomes taxable, according to IRAS. This makes early withdrawal costly in tax terms and is generally something members seek to avoid.

The 10-Year Spread Approach

Spreading withdrawals over the full 10-year window is a commonly discussed approach for minimising tax. To illustrate with a hypothetical example: an individual with SGD 400,000 in their SRS account who withdraws the entire sum in one year faces a large taxable amount. However, by withdrawing SGD 40,000 per year for 10 years, only SGD 20,000 is taxable annually. Based on current Singapore resident income tax rates, the first SGD 20,000 of chargeable income is taxed at 0%, according to IRAS, meaning each annual withdrawal in this scenario may attract little or no tax in the absence of other significant income. (This example is for illustration purposes only and does not constitute investment or tax advice.)

Tip: The 10-year spread tends to be most relevant when SRS funds are your primary income in retirement. If you have other income sources, consider consulting a qualified financial adviser about a suitable pace for your circumstances.

Special Circumstances

If SRS funds are withdrawn in full on the grounds of terminal illness, or deemed withdrawn upon death, a tax exemption of up to SGD 400,000 may apply, subject to conditions set out by IRAS. Where prior withdrawals have been made, the exemption amount is reduced accordingly.

Contribution Limits and Annual Deadlines

| Category | Annual Contribution Cap |

|---|---|

| Singapore Citizens and PRs | SGD 15,300 |

| Foreigners | SGD 35,700 |

Source: IRAS.

Contributions must be credited to your SRS account before the bank's cut-off on 31 December each year to qualify for relief in the following Year of Assessment. Partial contributions are permitted, so you can adjust based on your financial situation each year.

Investing Your SRS Funds

Leaving SRS funds uninvested earns only minimal interest. To capture the scheme's full potential, actively investing your balance is important. Eligible instruments include shares, ETFs, government bonds, and qualifying insurance products. Investors interested in income-oriented strategies may find dividend ETFs for building passive income a useful starting point.

For those exploring multi-market access, Longbridge provides investment exposure across Singapore, US, and Hong Kong markets. Understanding the full range of available investment products helps align SRS investments with your broader portfolio goals.

Frequently Asked Questions

Is SRS tax relief automatically applied?

Yes. According to IRAS, SRS tax relief is applied automatically based on information provided by your SRS operator. You do not need to claim it manually in your annual income tax return.

What happens if I withdraw from my SRS account early?

Withdrawing before your locked-in statutory retirement age incurs a 5% penalty on the withdrawn amount, and the full amount is subject to income tax rather than just 50%. This significantly reduces the scheme's tax advantages and should be avoided unless necessary.

Can foreigners benefit from SRS?

Yes. Foreigners residing in Singapore are eligible for SRS and have a higher annual contribution cap of SGD 35,700 compared with SGD 15,300 for Citizens and PRs. Foreigners may withdraw penalty-free after 10 continuous years from the date of their first contribution, regardless of the statutory retirement age.

Does my SRS investment carry risk?

The SRS account principal deposited at the bank is not directly subject to market risk. However, if you invest your SRS funds in shares, ETFs, or other market-linked products, the value of those investments may rise or fall. Investment returns are not guaranteed, and your risk tolerance and financial objectives should guide your investment choices.

Conclusion

The Supplementary Retirement Scheme offers a structured, tax-efficient framework for long-term retirement planning. Its three-layered structure, covering contribution relief, tax-deferred growth, and a 50% taxable concession on withdrawals, can create compounding advantages, and starting earlier generally allows more time for these to accumulate. Making the most of the scheme typically involves consistent contributions, active investment of SRS funds, and a well-planned withdrawal approach in retirement. As with any tax matter, individual circumstances vary, and you may wish to seek advice from a qualified tax or financial professional.

The choice of financial instruments depends on your investment objectives, risk tolerance, market outlook, and experience level. Regardless of the method selected, it is essential to fully understand its mechanics, risk characteristics, and execution rules, while maintaining a robust risk management plan. You can learn more about investment strategies through the Longbridge Academy or by downloading the Longbridge App.