US Dividend Withholding Tax: What Singapore Investors Need to Know

US dividend withholding tax deducts 30% from dividends before Singapore investors receive them. Discover how it works, what it affects, and practical approaches to reduce its impact.

TL;DR: Singapore investors face a 30% US dividend withholding tax on dividends paid by US-listed stocks and exchange traded funds (ETFs), with no treaty relief available. Understanding this tax — and the approaches available to manage it — is important for investors with US equity exposure.

Investing in US markets is appealing for Singapore investors: deep liquidity, globally recognised companies, and long-term equity growth. However, one cost that is easy to overlook is the US dividend withholding tax. Unlike capital gains, which are not taxed for non-US residents, dividends are subject to a mandatory deduction before they ever reach your brokerage account. For Singapore-based investors, this rate is a flat 30%.

This guide explains how US dividend withholding tax works, why Singaporeans are subject to the full rate, which investments are affected, and what practical approaches exist to manage its impact on your returns.

What Is US Dividend Withholding Tax?

US dividend withholding tax is a tax levied by the United States government on dividend income paid to non-resident investors — individuals who are not US citizens or permanent residents. Rather than requiring foreign investors to file a US tax return, the tax is deducted at source: your broker or the fund administrator withholds the amount before distributing the remainder to you.

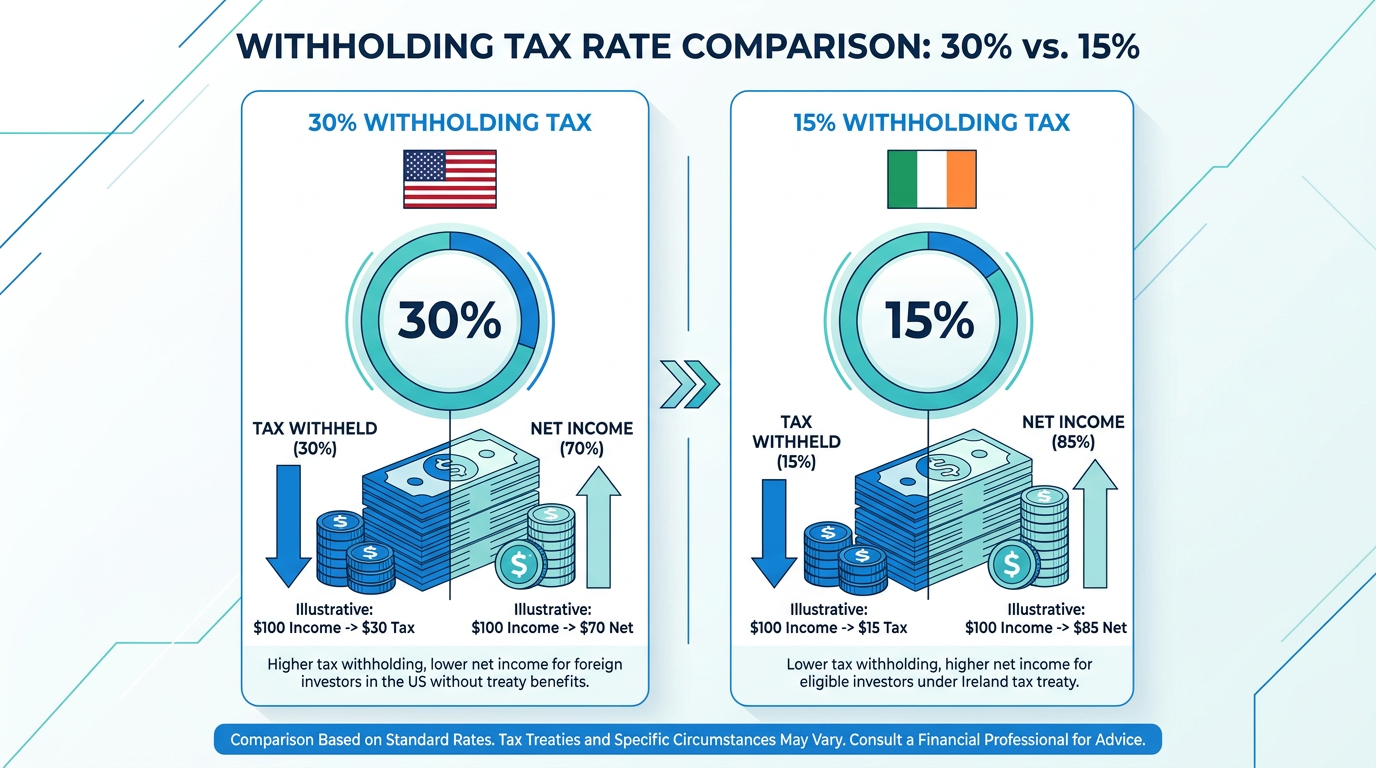

The statutory rate is 30%, as defined under Section 871 of the US Internal Revenue Code (see the US Internal Revenue Service at irs.gov). The US has bilateral income tax treaties with a number of countries that can reduce this rate — in many cases to 15% — for investors resident in those nations. Singapore is not among them; there is currently no income tax treaty between Singapore and the United States that covers dividend withholding.

This means that when a US company or a US-domiciled ETF pays you a dividend, the default 30% is automatically deducted before you receive anything.

How the Deduction Works in Practice

When a US-listed stock or fund declares a dividend, the paying agent withholds 30% and remits it directly to the US Internal Revenue Service (IRS). You receive the net amount: for illustration purposes only, this would be 70 cents for every USD 1.00 declared. No US tax return is required; the process is automatic.

To facilitate this, your broker will typically ask you to complete a W-8BEN form (Certificate of Foreign Status of Beneficial Owner for United States Tax Withholding and Reporting) before trading US-listed securities. This form confirms your status as a non-US person and establishes which withholding rate applies. Without it, the default withholding rate could be even higher.

What Singapore's Tax Authority Says

According to the Inland Revenue Authority of Singapore (IRAS) at iras.gov.sg, dividend income received from foreign investments is generally not taxable in Singapore, since Singapore does not levy a personal dividend tax. However, because no US-Singapore tax treaty exists, you cannot claim a foreign tax credit in Singapore for the 30% already withheld by the US.

Which Investments Are Affected?

The 30% withholding tax applies to dividend and distribution income from any US-domiciled investment vehicle. The domicile of the investment — where it is registered — determines the applicable tax treatment, not where it is listed.

Affected categories include:

- US-listed stocks: Dividend-paying companies incorporated in the United States

- US-domiciled ETFs: Funds registered under the US Investment Company Act

- US Real Estate Investment Trusts (REITs): Required to distribute at least 90% of taxable income, making them particularly susceptible to withholding tax drag

- US-listed American Depositary Receipts (ADRs): Depending on the underlying structure, these may also be subject to withholding

Capital gains are not affected. If you purchase US-listed shares and sell them at a profit, no US withholding tax applies. The 30% applies only to dividend and certain distribution income.

The Hidden Cost: US Estate Tax

Beyond dividend income, Singapore investors holding US-situs assets face a second, less visible risk: the US estate tax.

When a non-US-domiciled individual passes away holding US-situs assets — which include US-listed stocks, ETFs, and bonds held in a brokerage account — the US federal estate tax may apply to the value of those assets.

The estate tax exemption available to non-resident aliens is generally cited as USD 60,000, a figure that is considerably lower than the federal estate tax exemption available to US citizens and domiciliaries. Investors should verify the current exemption amount with the US Internal Revenue Service (irs.gov) or a qualified tax adviser, as these figures can change.

Why This Matters for Smaller Portfolios

Even a modest US equity portfolio can exceed the USD 60,000 threshold, which many Singapore investors may cross as their portfolios grow. The US federal estate tax is progressive, with rates that rise on amounts above the exemption (refer to the US Internal Revenue Service at irs.gov for the current rate schedule). This liability is worth understanding before it becomes a concern for your beneficiaries.

The estate tax issue does not arise from Singapore-listed or Ireland-domiciled holdings — only from assets classified as US-situs property. If your US-situs holdings are significant, consulting a qualified financial planner or tax adviser is advisable.

Approaches to Managing Dividend Withholding Tax

While there is no way to entirely eliminate US dividend withholding tax when investing in US-domiciled securities as a Singapore resident, several approaches may help reduce its impact on your overall portfolio.

1. Ireland-Domiciled UCITS ETFs

Ireland has a bilateral tax treaty with the United States that, under that treaty, reduces dividend withholding to 15% at the fund level. Ireland-domiciled UCITS (Undertakings for Collective Investment in Transferable Securities) ETFs that hold US equities therefore generally have 15% — rather than 30% — withheld on dividends received from their US holdings. Ireland does not impose additional withholding on distributions to non-Irish investors. The applicable rates should be verified against the relevant US-Ireland treaty and the fund's documentation.

Some Singapore investors consider UCITS ETFs that track US indices rather than their US-listed equivalents because of this different withholding treatment, even when both follow the same underlying benchmark; whether this is appropriate depends on individual circumstances, and investors may wish to consult a qualified tax adviser. Ireland-domiciled ETFs are also often structured as accumulating funds — reinvesting dividends rather than distributing them — which can reduce the frequency of taxable events.

Note: Always verify the domicile of an ETF by checking its prospectus or Key Investor Information Document (KIID), not simply where it is listed. An ETF can be listed on the Singapore Exchange (SGX) while being domiciled in Ireland or the US, each with different tax implications.

2. Focus on Growth-Oriented, Low-Dividend Holdings

If your US equity exposure is concentrated in growth-oriented companies or accumulating ETFs that pay little or no dividends, the dividend withholding tax has minimal practical impact. Capital appreciation — the primary return driver for growth-focused investments — is not subject to US withholding for non-residents.

This does not suggest avoiding dividend-paying assets entirely, but it is worth factoring the withholding cost into your return expectations.

3. Allocate Income-Generating Investments to Singapore or Other Markets

Singapore operates a one-tier corporate tax system under which dividends paid by Singapore-incorporated companies are fully exempt from further tax. There is no withholding tax on dividends from Singapore-listed companies, a difference in tax treatment that some income-focused investors take into account when building passive income from dividend ETFs.

Diversifying income-generating holdings across Singapore-listed stocks, Real Estate Investment Trusts (REITs), and ETFs — rather than concentrating exposure in US-listed securities — can reduce withholding tax drag. The Longbridge products page provides an overview of investment products available across Singapore, US, and Hong Kong markets.

4. Account Structure Considerations

Investors using the Supplementary Retirement Scheme (SRS) or the Central Provident Fund Investment Scheme (CPFIS) should be aware that these accounts do not exempt holdings from US dividend withholding tax. The tax is applied at the source level by US payers regardless of the account type used — there is no mechanism by which an SRS or CPFIS wrapper eliminates this obligation.

Dividend Withholding Tax at a Glance

| Factor | Detail |

|---|---|

| Standard withholding rate (Singapore investors) | 30% |

| Reduced rate via Ireland-domiciled UCITS ETFs | 15% |

| Capital gains tax for non-US residents | None |

| US estate tax exemption (non-resident aliens) | USD 60,000 |

| Singapore dividend tax on locally distributed dividends | None |

| Tax treaty between US and Singapore | None |

| Form required to confirm non-US residency | W-8BEN |

Note: The figures above are general references that may change over time. Verify current rates and requirements with a qualified tax adviser, the US Internal Revenue Service (irs.gov) for US tax matters, or the Inland Revenue Authority of Singapore (IRAS) at iras.gov.sg for Singapore tax matters.

Frequently Asked Questions

Does the 30% withholding apply to ETFs as well as individual stocks?

Yes. If the ETF is domiciled in the United States, dividends distributed to Singapore investors are subject to the 30% withholding rate. This applies regardless of the underlying holdings of the ETF. If the ETF is domiciled in Ireland, a 15% rate applies at the fund level, and no further withholding is imposed by Ireland on distributions to non-residents.

Will I be taxed again in Singapore on US dividends I receive?

Singapore does not levy personal income tax on foreign dividend income under its territorial tax system. The 30% deducted by the US is the extent of the tax cost. No US-Singapore tax treaty exists, so you cannot claim a foreign tax credit in Singapore for the amount withheld.

Does where my broker is located affect the withholding tax?

No. The withholding tax is determined by the domicile of the investment and the investor's country of residence, not the broker's location. A Singapore investor purchasing US-domiciled securities through any brokerage platform will be subject to the same 30% withholding.

What is the W-8BEN form and do I need to submit it?

The W-8BEN form is a declaration to the US tax authorities confirming your status as a non-US person. It establishes the 30% withholding rate for Singapore residents and confirms you are not subject to US capital gains tax. Your broker will typically prompt you to complete this form when opening a US trading account.

Are US REITs more heavily impacted by withholding tax?

US Real Estate Investment Trusts (REITs) must distribute at least 90% of taxable income to shareholders annually. Because they pay out a higher proportion of income, the withholding drag is proportionally larger. Investors seeking dividend income from REITs may wish to weigh this cost against Singapore-listed REITs, where dividend distributions are not subject to withholding.

Conclusion

US dividend withholding tax is an often-overlooked cost for Singapore investors with US equity exposure. At 30% — with no treaty reduction available — it meaningfully reduces income from US-domiciled dividend-paying investments. Understanding which investments are affected, how the mechanism works, and what practical approaches exist forms an important part of building a well-informed investment strategy.

Whether you are building a growth portfolio, seeking dividend income, or diversifying across markets, factoring in tax costs alongside returns gives you a clearer picture of actual outcomes.

The choice of financial instruments depends on your investment objectives, risk tolerance, market outlook, and experience level. Regardless of the method selected, it is essential to fully understand its mechanics, risk characteristics, and execution rules, while maintaining a robust risk management plan. You can learn more about investment strategies through the Longbridge Academy or by downloading the Longbridge App.