$TENCENT(00700.HK) Who did they provoke? Who knows?

Boss's Boss

Boss's BossSuggestions for you to follow

B

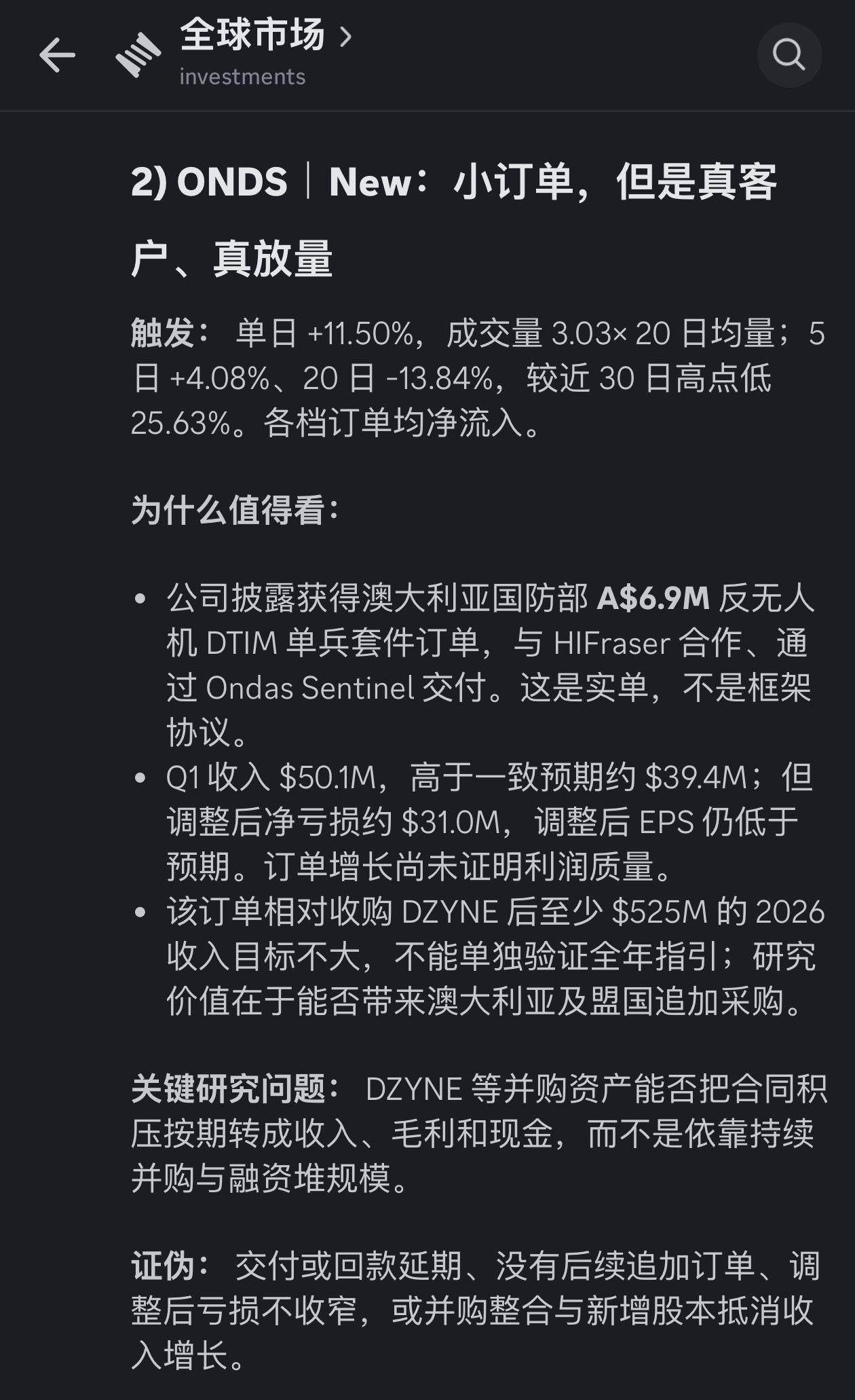

$Ondas(ONDS.US) is worth considering for a long position. Planning to re-enter.

My stock US market auto-tracking Agent also sent me a reminder .

Ondas

USONDS

B

$Rocket Lab(RKLB.US)$Tesla(TSLA.US) are both victims of Korean retail investors deleveraging. Because the concentration of Korean retail investors investing in these two stocks is also very high. At least that's how it feels from what I see on X.

Rocket Lab

USRKLB

B

$Alibaba(BABA.US)This is the reason I bought Alibaba

Repost:

Benchmark test results for the Qwen3.8-Max preview version have leaked.

According to benchmark test results obtained internally from @Alibaba_Qwen, the Qwen3.8-Max preview version trails Fable 5 by only 12.6 points in coding, while its performance has already surpassed Opus 4.8 Max in actual Cowork agent tasks.

The benchmark covers 400 real-world agent tasks.

Compared to Fable 5, 73.2% of coding task results are identical.

In Cowork tasks, Qwen3.8-Max leads:

- Opus 4.8 Max: 5 points

- Kimi K3: 8 points

- GLM-5.2: 17.1 points

- Previous generation Qwen3.7-Max: 44.4 points

And this is just the preview version.

Sources say that some ready improvements have not yet been deployed, and the final version will be even more powerful.

Qwen3.8's current goal is Fable 5, and Opus has already been surpassed

Alibaba

USBABA

B

$XTALPI(02228.HK) A mere 400 million HKD in trading volume, and it crashed 10%. Liquidity has completely dried up. Where did all the money go?

B

$XTALPI(02228.HK) This is a sign of a stock market crash. Friends, be cautious if you have high leverage.

XTALPI

HK02228

B

$XTALPI(02228.HK)$Tesla(TSLA.US)If the AI bubble is to burst, it must be due to the comprehensive failure of AI applications. Or rather, the future of AI changing humanity lies in the full flourishing of AI applications. The most representative areas in this regard are AI applications in biopharmaceuticals and applications of related machinery represented by autonomous driving.

B

$XTALPI(02228.HK) is so tough, guys. I got hammered again $Netflix(NFLX.US)

Didn't expect that in these past few days, the one that treated me best was still $IShares Ethereum Trust ETF(ETHA.US)

XTALPI

HK02228

B

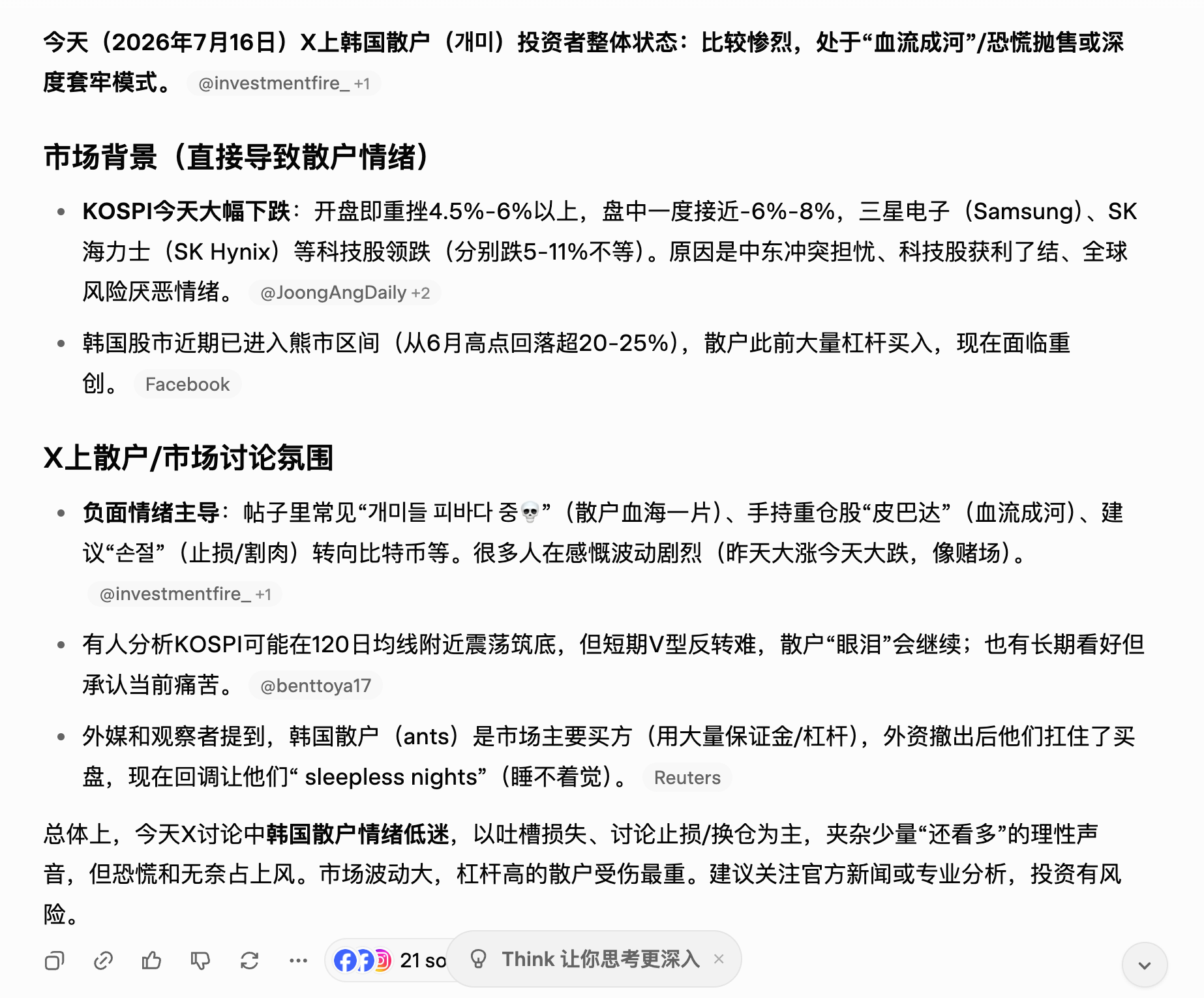

$XL2CSOPHYNIX(07709.HK) The Korean market is closed for a holiday, no trading. What to do? Can only be short against short.

XL2CSOPHYNIX

HK07709

B

$Rocket Lab(RKLB.US) This is really completely incomprehensible. What's the reason for the drop? Can only say that quant trading is too powerful.

Rocket Lab

USRKLB

B

$XTALPI(02228.HK) will return to 15 first? Or will $Rocket Lab(RKLB.US) return to 150 first?

I just want to quietly hold and wait for a big piece of news. It's really hard.

XTALPI

HK02228

B

The stage peak of the South Korean stock market, or the stage peak of AI storage, might be overall positive for the Hong Kong stock market. Some liquidity will return. The definition of stock prices by liquidity, to a large extent (within the standard retail investor framework), is much more important than fundamentals.

B

I want to create a #I'm Even More Miserable Than You topic group, can we get 500 people to respond? Can Longbridge start one? I'll die of boredom if I don't talk, but I just want to find a friend who's even more down than me so we can wipe each other's tears.

B

$XL2CSOPHYNIX(07709.HK)At this point, I feel most sorry for my family. I just went to check on my Korean friends, are you guys okay? The answer was silence😶.

XL2CSOPHYNIX

HK07709

B

$Sony Group Corporation(6758.JP) I think Sony has held steady at this level. I sold a batch of puts at 3378, expiring at the end of the month, and I'll see if they get exercised. If they are, I'll gladly accept it.

B

$XTALPI(02228.HK) Why not speak up? It's not because people have left, nor is it because the stock is gone, but because in the current situation, with insufficient liquidity, anything said is wrong.

XTALPI

HK02228

B

$XTALPI(02228.HK) can only imagine the young Koreans standing on the tallest building in Seoul right now.

Speaking of which, Jingtai fell from 15 to 7.5

Little Rocket fell from 150 to 75

Damn it, it's really messing with me.

XTALPI

HK02228

B

$XTALPI(02228.HK) It's so hard🤯 Getting beaten up from all sides.

XTALPI

HK02228

B

Mr. Zhou's technical analysis of 2228.HK

Regarding the interpretation of Mr. Zhou's $XTALPI(02228.HK) chart: Jason: Understandable. The core of this friend's chart is not the complex indicators themselves, but rather expressing a relatively clear technical view: 2228 has emerged from a long-term downtrend and is undergoing a bottom reversal; 7.9–8.0 is the first breakout level, and 9.5–10 is the main resistance zone. I break down the chart into several layers: 1. Descending Wedge Breakout The two blue descending trendlines in the chart form a structure similar to a descending wedge / converging downtrend channel. His point is: it fell all the way from last year's high...

B

$XTALPI(02228.HK) The short positions from the past month are all underwater now, not sure if it will trigger a short squeeze or if it has already started. @Zhou Shuren's Trader Care to give us an analysis, Mr. Zhou?

XTALPI

HK02228

B

$XTALPI(02228.HK) community is really quiet, but it's completely understandable. The past six months have really tormented retail investors. Isn't a double Hynix ETF better? Managing a portfolio well is truly difficult.

I feel that AI-related trading may have reached a turning point. Capital and hot spots are about to shift. Personally, I'm still betting on the AI application track. Holding on tight and not letting go.

XTALPI

HK02228

B

$XTALPI(02228.HK) The trading volume is still relatively low. It needs a surge in volume to make the shorts despair.

XTALPI

HK02228

B

$XTALPI(02228.HK) Hmm, ahem, about to take off. Boarding soon 😄 Hope everyone has a happy week

XTALPI

HK02228

B

$XTALPI(02228.HK) How will AI change our lives? Everything in life?

The year 26/27 will be a year of continued growth in AI applications. Jingtai's AI TOKENS story should start soon. My feeling is

XTALPI

HK02228

B

Last Friday, the robot concept drove $AVONFLOW(301575.SZ) up in a wave. It seems the market has already started to gradually understand its potential. Of course, the A-share market is more about trading first. But this company still has a robot component supply chain story to tell. I hold a very small amount.

AVONFLOW

SZ301575