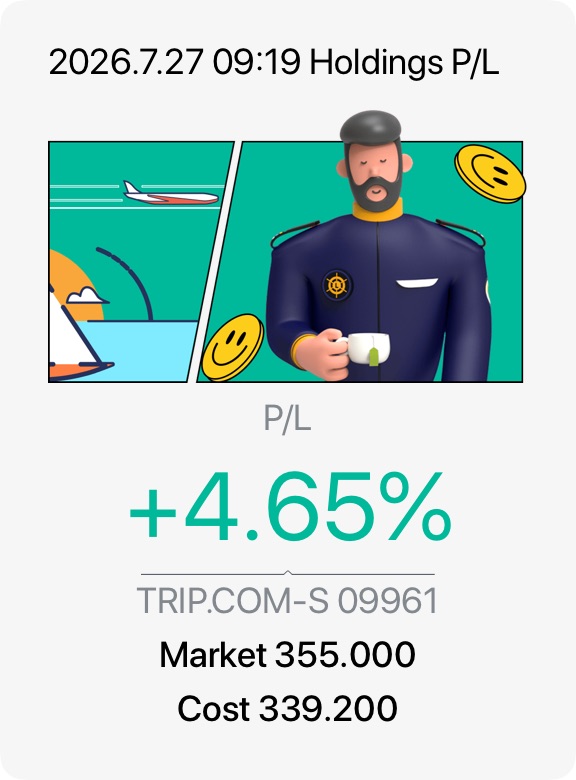

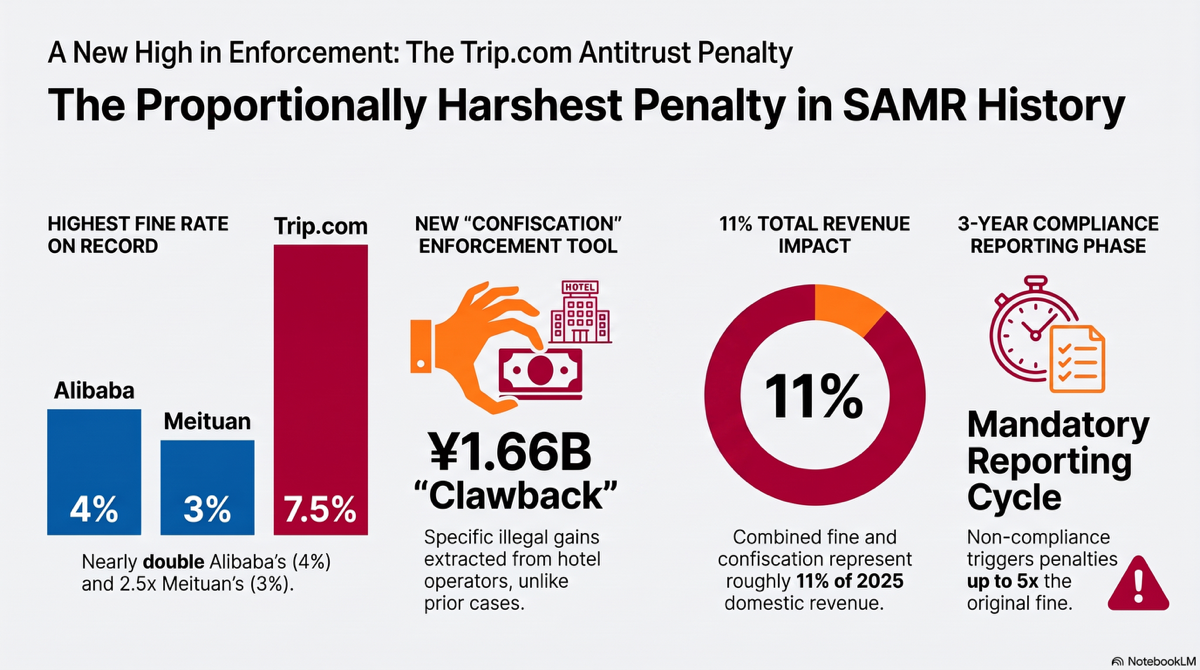

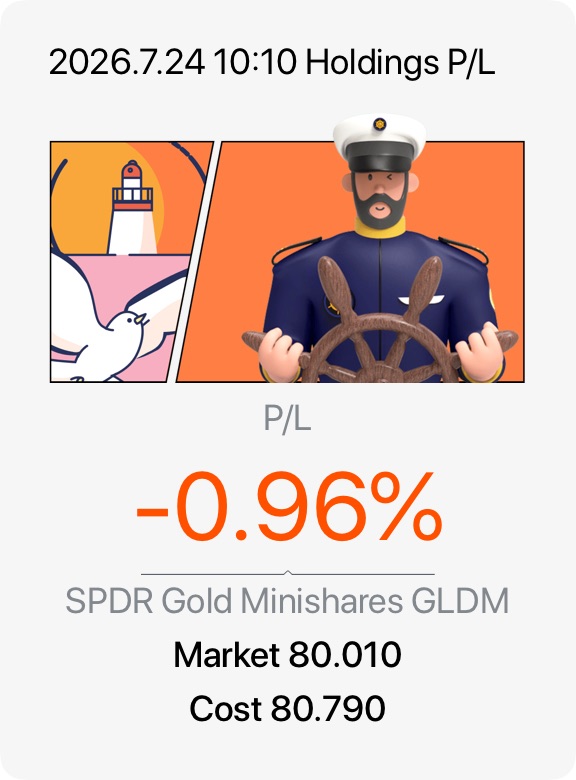

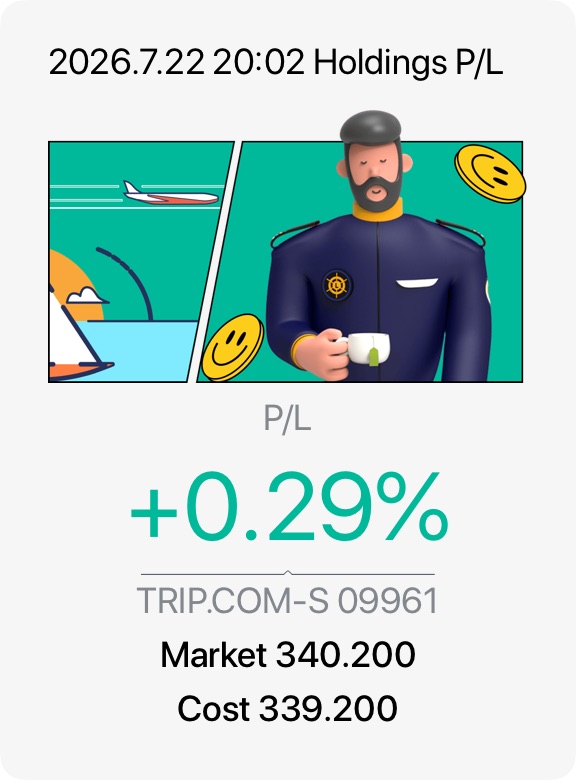

I am glad to see Trip.com is not trading below its friday price today 😆. There is no panic selling as some had feared. Good news.

Overall, I remain optimistic about the Hong Kong market. I believe Chinese authorities will step in to support it, we won’t see any major crash unless overall market trend change drastically. Hence, Chinese authorities intervene gives investors and companies much-needed confidence.

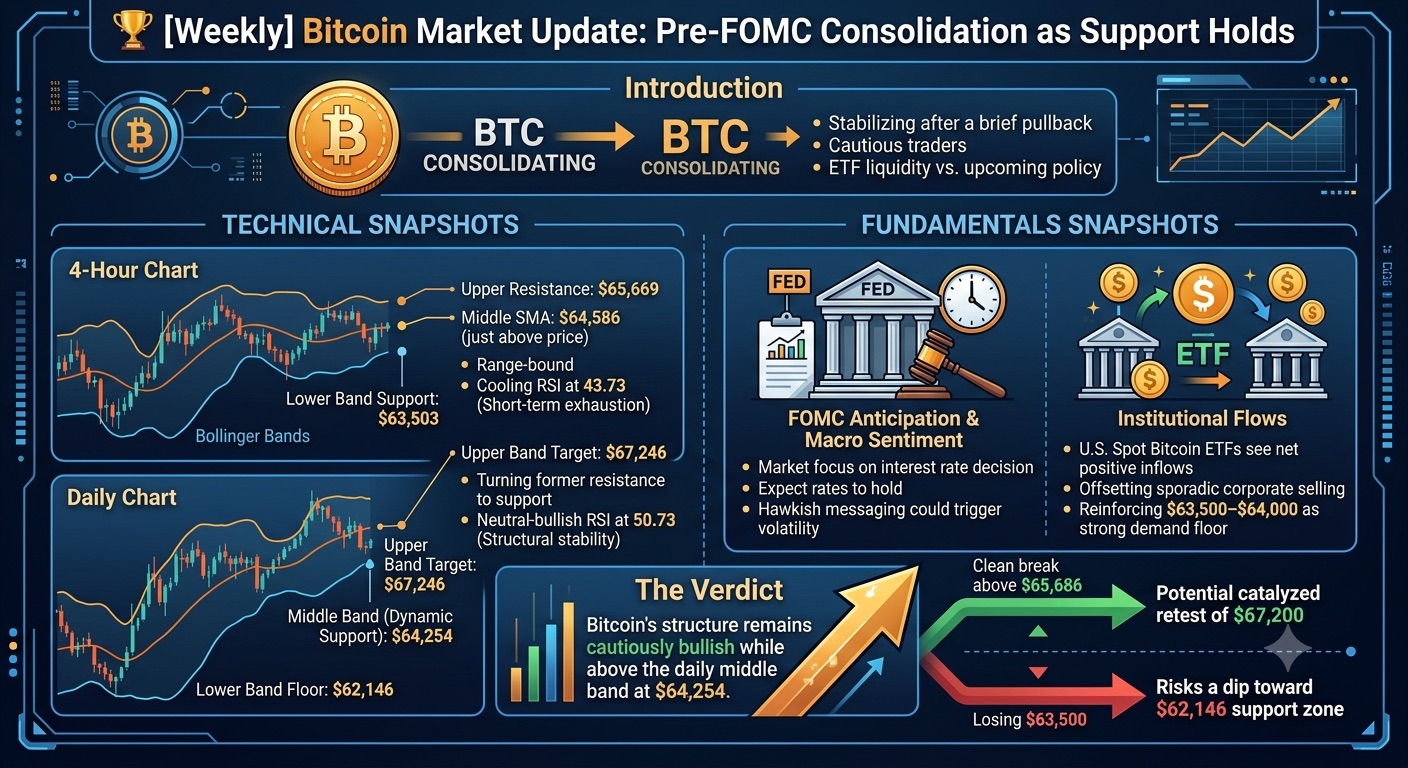

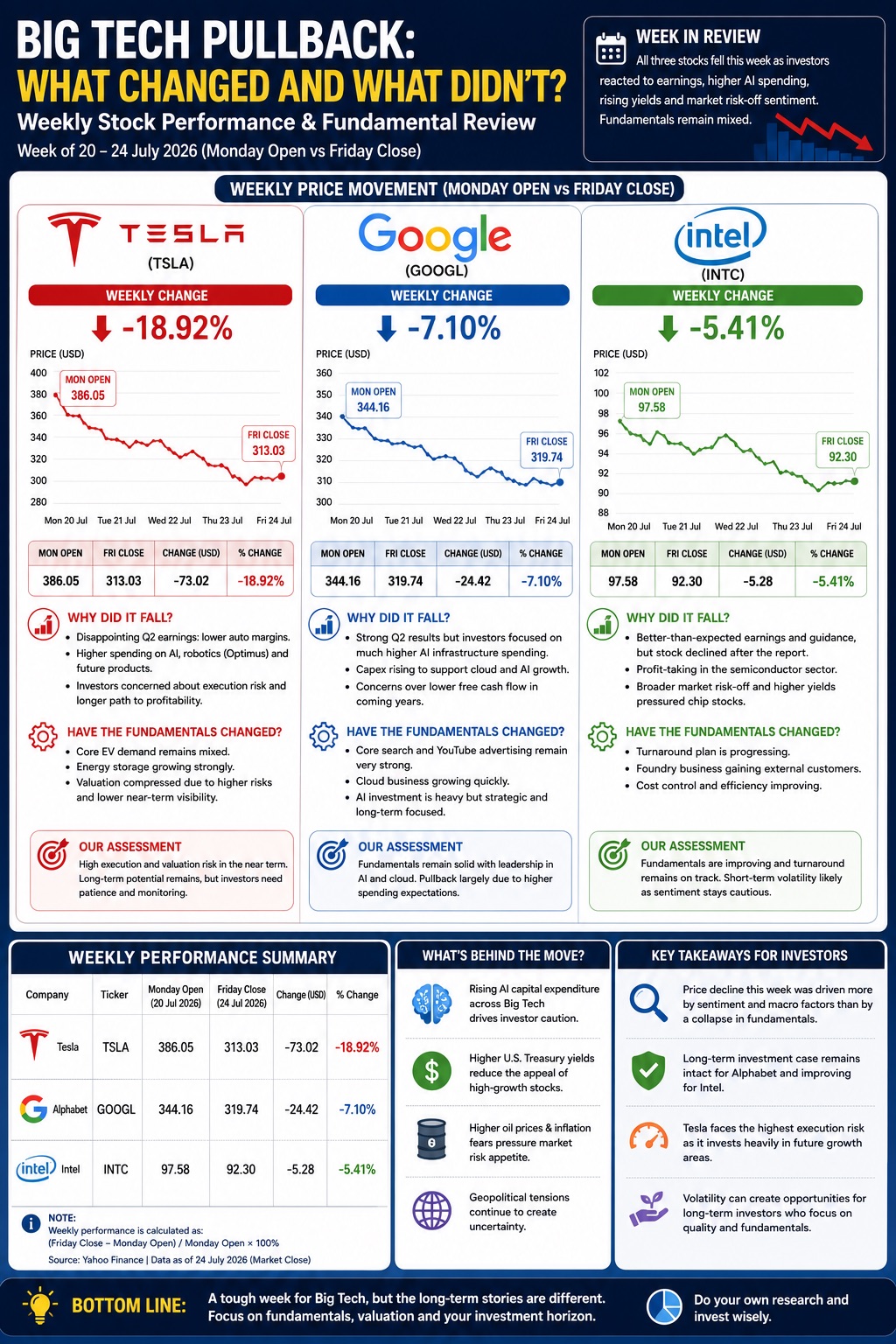

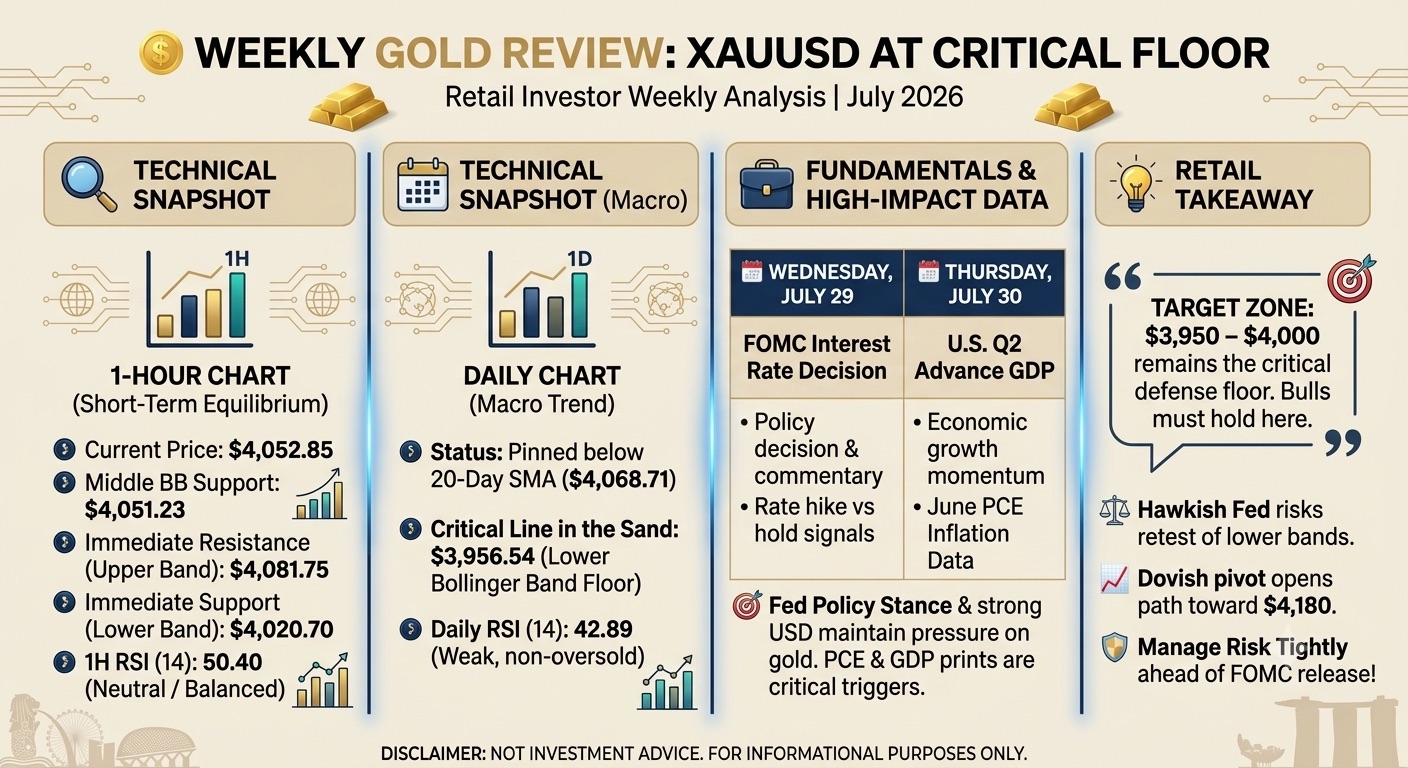

This week is all about the Fed meeting . I expect stocks and metals to swing wildly like a roller coaster, especially tech names. Buckle up for a bumpy ride! 😆 . No “BUY” button for this week just ride my Green dragon 🐉☺️.