$Mapletree Log Tr(M44U.SG)

Investment Outlook: Mapletree Logistics Trust (MLT)

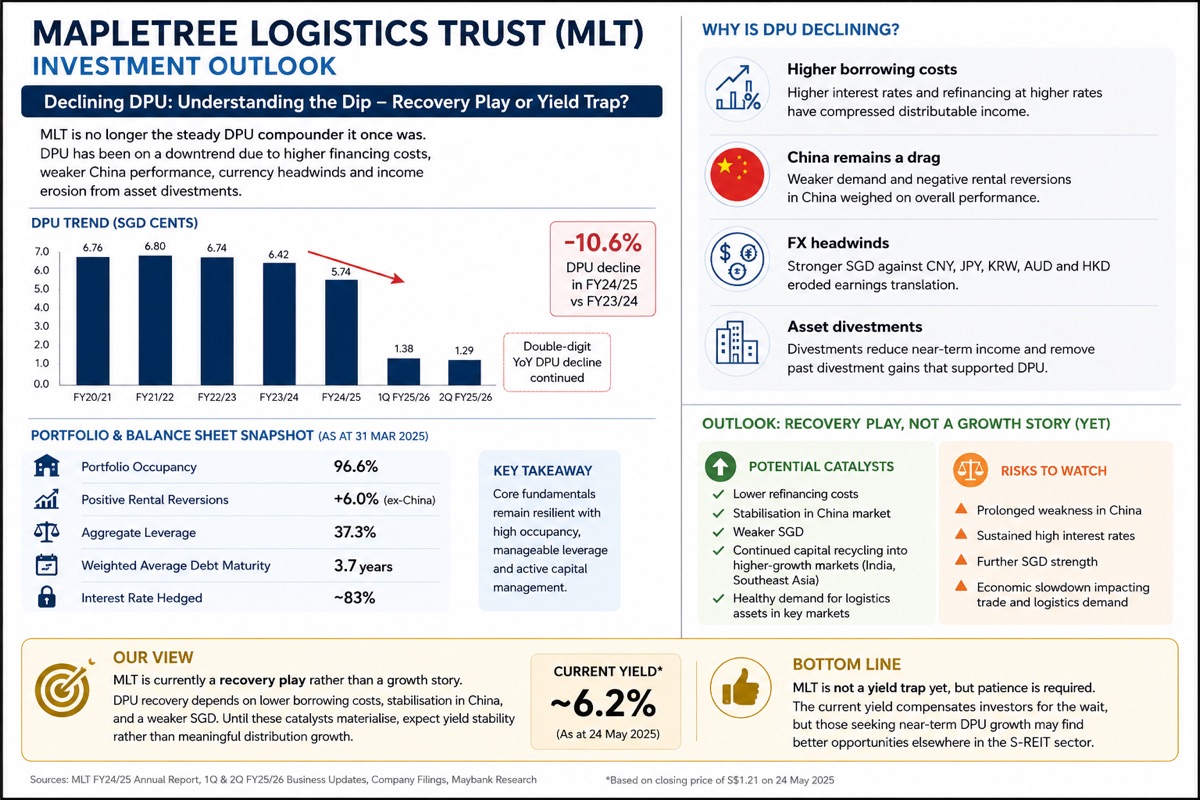

Mapletree Logistics Trust is no longer the “steady DPU compounder” that many income investors bought a few years ago. FY2024/25 DPU fell 10.6% year-on-year, and subsequent quarters in FY2025/26 continued to record high single-digit to double-digit DPU declines.

The reasons are clear:

* Higher borrowing costs have compressed distributable income despite stable portfolio occupancy.

* China remains a drag, with weaker demand and negative rental reversions.

* A strong SGD against regional currencies (CNY, JPY, KRW, AUD, HKD) has eroded earnings translation.

* Asset divestments, while strategically sensible, reduce near-term income and remove past divestment gains that had supported DPU.

That said, I would not classify MLT as a yield trap yet. Occupancy remains above 96%, rental reversions outside China are positive, gearing is manageable, and management is actively recycling capital into higher-growth markets such as India and Southeast Asia.

My assessment: MLT is currently a recovery play rather than a growth story. DPU recovery depends on lower refinancing costs, stabilisation in China, and a weaker SGD. Until these catalysts materialise, investors should expect yield stability rather than meaningful distribution growth. The current yield compensates investors for patience, but those seeking near-term DPU expansion may find better opportunities elsewhere in the S-REIT sector.

The copyright of this article belongs to the original author/organization.

The views expressed herein are solely those of the author and do not reflect the stance of the platform. The content is intended for investment reference purposes only and shall not be considered as investment advice. Please contact us if you have any questions or suggestions regarding the content services provided by the platform.