$Kep Infra Tr(A7RU.SG)

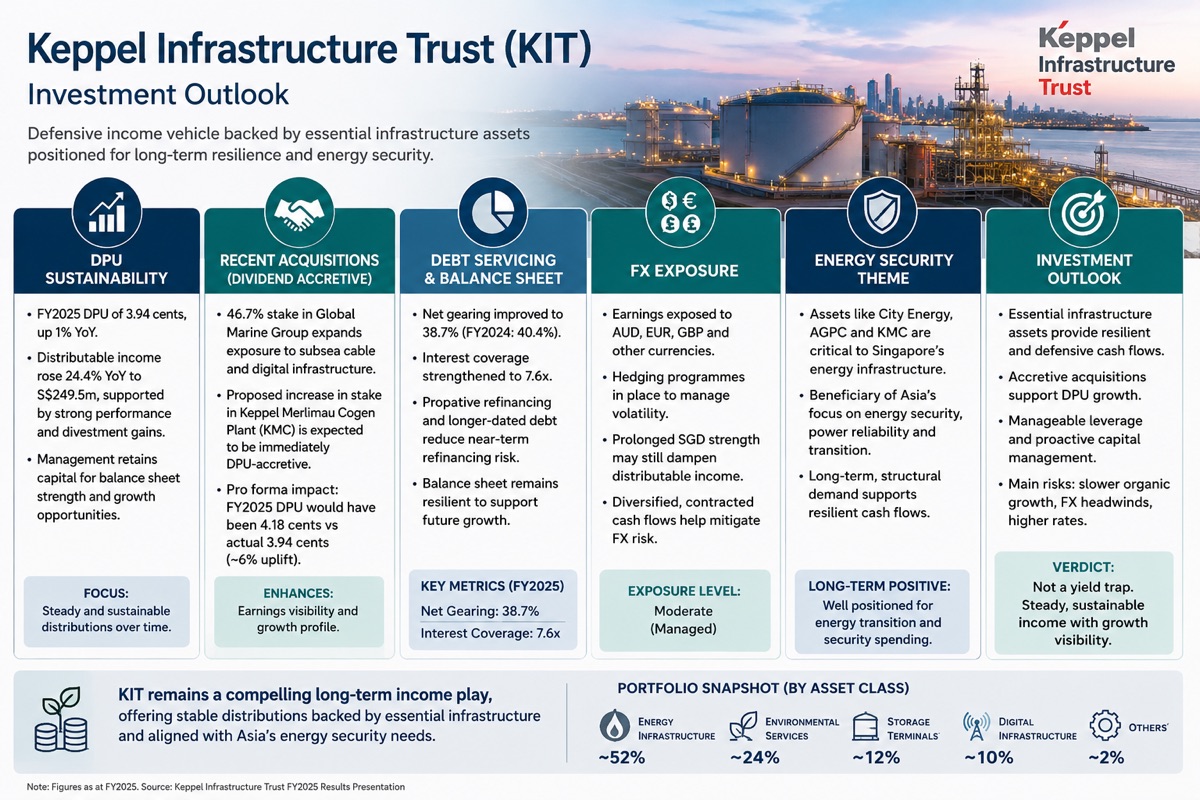

Keppel Infrastructure Trust (KIT) offers a relatively defensive income proposition backed by essential infrastructure assets spanning energy, environmental services, storage and digital connectivity. Unlike traditional REITs, its revenues are largely supported by regulated or long-term contracted cash flows, enhancing DPU resilience.

Recent acquisitions, including Global Marine Group and the increased stake in Keppel Merlimau Cogen Plant, strengthen exposure to energy security and digital infrastructure. The Merlimau transaction is expected to be DPU-accretive, providing a visible growth catalyst.

Balance sheet risk appears manageable, with gearing below 40% and healthy interest coverage. While higher-for-longer interest rates remain a headwind, proactive refinancing has reduced near-term debt servicing concerns.

Foreign exchange exposure to AUD, EUR and GBP remains a risk as a stronger Singapore dollar could dilute overseas earnings despite hedging measures. Nevertheless, KIT’s diversified portfolio helps mitigate concentration risk.

The long-term investment thesis remains anchored on Asia’s growing demand for energy security, power reliability and critical infrastructure. While DPU growth is unlikely to be rapid, KIT does not currently resemble a yield trap. Instead, it appears positioned to deliver steady and sustainable distributions, supported by accretive acquisitions and resilient infrastructure cash flows.

The copyright of this article belongs to the original author/organization.

The views expressed herein are solely those of the author and do not reflect the stance of the platform. The content is intended for investment reference purposes only and shall not be considered as investment advice. Please contact us if you have any questions or suggestions regarding the content services provided by the platform.