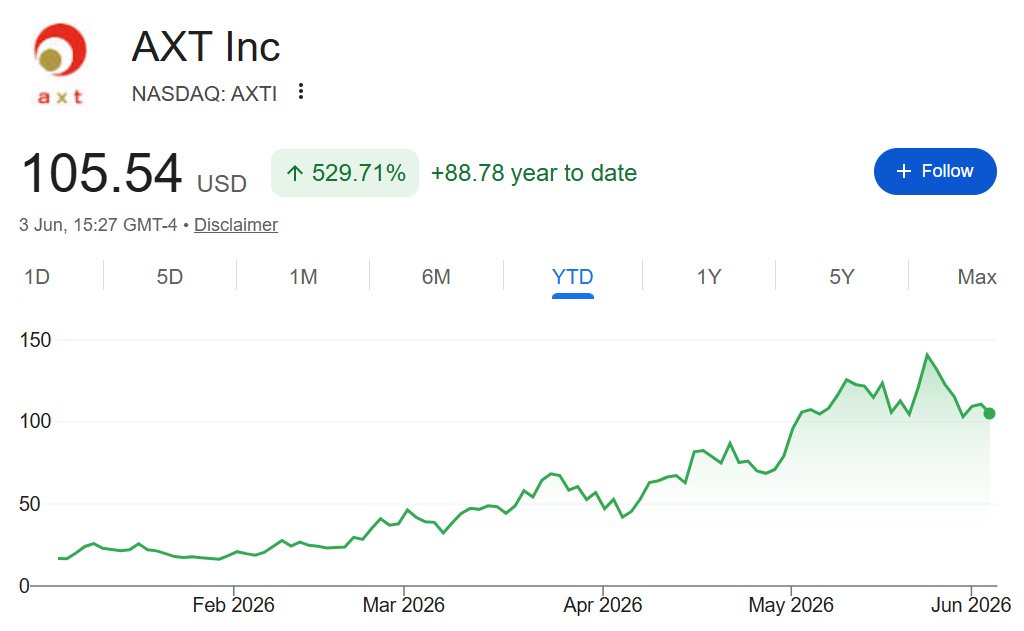

Everything's gone quiet around $AXT(AXTI.US) suddenly?

They're still a vital InP substrate bottleneck:AI capex ↓More GPUs↓Optical interconnect↓Optical transceivers (800G → 1.6T → 3.2T)↓Each transceiver needs EML/DFB/CW lasers↓Those are fabbed on InP substrates↓$AXT(AXTI.US) (and Sumitomo) supply the substratesNear term story is 800G/1.6T pluggables. CPO inflection will be "late 2027 and beyond" (management guidance).With 2X InP capacity by end of 2026. I.e. demand > supply.And fresh capex in 6-inch InP R&D for next-gen EML/SiPho:Larger diameter = more die per wafer = lower unit cost + is required by some advanced device roadmaps.But ofc, a ton of pricing-in has happened already:Probably looking further ahead to 6-inch InP ramp for 1.6T and probably even CPO (2027+ story).Personally don't see anything wrong with trimming at these levels (I did last week to rotate some gains elsewhere)But keeping some exposure makes sense imo since a ton of capex flows direct to them. So we should see a QoQ improvement in reported earnings as backlog converts etc.

The copyright of this article belongs to the original author/organization.

The views expressed herein are solely those of the author and do not reflect the stance of the platform. The content is intended for investment reference purposes only and shall not be considered as investment advice. Please contact us if you have any questions or suggestions regarding the content services provided by the platform.

Post your comment

No Comments