[IPO Analysis] Is it really worth subscribing to Anjoy Foods' Hong Kong IPO?

In the past two weeks regarding IPO subscriptions in Hong Kong stocks, I shared about Haitian Flavoring and Yunzhisheng, maintaining a pace of sharing one company per week. As this week is almost over, I'll stick to this routine and share the company I want to talk about today on the last working day—$Anjoy Food(02648.HK).

Here’s my take: Be cautious when subscribing; don’t be too impulsive.

Before analyzing the reasons with you, let’s first understand this company:

Anjoy Food was founded in 2001 and initially made a name for itself with frozen hotpot ingredients like fish balls, crab sticks, and beef balls. It has now become one of the leaders in China’s frozen food industry. Its main business includes three segments:

- Fish paste products (e.g., balls)

- Frozen rice and flour products (e.g., dumplings, glutinous rice balls)

- Frozen prepared dishes (e.g., pre-made meals)

In recent years, it has also ventured into "pre-made dishes" and To C brands like "Chan Gongfu" and "Dongpin Xiansheng," but compared to the established reputation of Anjoy, I’d say these brands still have a long way to go.

Simply put, it’s not a new consumer brand that relies on internet fame or viral products but a traditional food manufacturing company that thrives on "production capacity + distribution channels."

Financially speaking, it’s just average—nothing exciting.

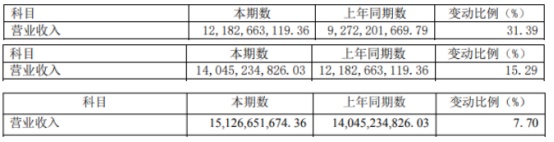

1. Revenue

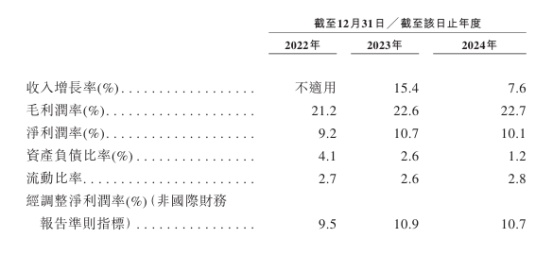

From 2022 to 2024, the company’s revenue was 12.18 billion yuan, 14.05 billion yuan, and 15.13 billion yuan, respectively, but the growth rate dropped from 31.39% to 15.29% and then to 7.7%. The growth has clearly slowed, shifting from high growth to single-digit growth.

2. Net profit attributable to shareholders

The decline in growth is even more pronounced, plummeting from 61.37% and 34.24% to a near standstill at 0.46%.

3. Gross margin

From 2022 to 2024, the gross margins were 21.2%, 22.6%, and 22.7%, respectively (industry average: 18%).

Beyond the numbers, another point worth noting is the negative sentiment among retail investors toward Anjoy’s Hong Kong listing.

At the December 2024 shareholders’ meeting, the proposal for Anjoy to issue H-shares and list on the Hong Kong Stock Exchange was approved with only 70% of the votes in favor from A-share holders. Among shareholders with less than 5% stakes, there were 30.89 million votes in favor and 48.88 million against, with opposition exceeding 60%.

Many investors questioned the rationale behind "raising funds in Hong Kong despite not needing money," with some even calling it a "cash grab."

The annual report shows that in 2024, Anjoy had 2.779 billion yuan in cash, down 44.14% year-on-year, but this doesn’t indicate worsening financial health—the funds were redirected into wealth management products, with current financial assets growing 221.44% to 3.321 billion yuan. The company’s short-term loans were only 111 million yuan, with total current liabilities at 3.679 billion yuan and a current ratio of 2.81, indicating extremely strong cash flow.

Additionally, the 5.67 billion yuan raised in February 2022 remains partially unused. As of the end of 2024, 3.88 billion yuan had been invested, leaving 1.677 billion yuan idle in wealth management.

Raising funds despite not needing money is indeed puzzling.

After all this, is this IPO subscription worth it?

Let’s analyze the logic from an IPO subscription perspective.

1. Discount doesn’t equal opportunity

The maximum offer price is HK$66, which seems like a 20%+ discount compared to the current A-share price of around 76 yuan.

But note: Hong Kong’s valuation system inherently applies discounts, and not all "discounts" are arbitrage opportunities. For consumer manufacturing companies like Anjoy, lower valuations in Hong Kong are common, so discounts are normal.

Moreover, the final pricing isn’t set yet. If it’s priced near the high end, the discount will shrink, leaving little room for arbitrage.

2. IPOs without compelling narratives don’t attract market interest

The Hong Kong market currently favors specific themes: tech, healthcare, etc. Traditional food companies like this one don’t excite institutions much.

Having a growth story isn’t enough—the market must be willing to listen.

Anjoy’s current narrative is awkward: pre-made dishes are still unproven, To C brands haven’t gained traction, and international expansion is a long-term play. Expecting a hot debut based solely on its "fish ball leader" title? Unlikely.

3. Hong Kong IPO subscriptions are no longer a "sure win"

In recent years, people got used to making small profits from Hong Kong IPOs, but the environment has changed:

- Investor risk appetite has declined.

- New stocks frequently break issue prices.

- Without significant oversubscription or hot sectors, it’s hard to generate hype.

For example, recent consumer-sector IPOs have performed poorly, with even initial gains quickly fading. If Anjoy’s valuation isn’t cheap and lacks a standout feature, the risk of breaking the issue price is real.

In summary:

Anjoy Food has a stable foundation but lacks growth catalysts. While the Hong Kong IPO offers a discount, the opportunity is limited. Approach with caution and avoid expecting guaranteed profits.

$NVIDIA(NVDA.US) $Tesla(TSLA.US) $Circle(CRCL.US) $Coinbase(COIN.US) $AMD(AMD.US) $Apple(AAPL.US) $Coreweave(CRWV.US) $Alibaba(BABA.US) $XIAOMI-W(01810.HK)

The copyright of this article belongs to the original author/organization.

The views expressed herein are solely those of the author and do not reflect the stance of the platform. The content is intended for investment reference purposes only and shall not be considered as investment advice. Please contact us if you have any questions or suggestions regarding the content services provided by the platform.