Has the U.S. stock market's Santa Claus rally arrived? A complete analysis from liquidity, seasonal effects to sector rotation

Every December, U.S. stock investors mention a term: the Santa Rally. It refers to the systematic rise in U.S. stocks around Christmas, especially from Thanksgiving to New Year's Day, with the S&P and Nasdaq often showing steady upward trends. This pattern is not mysterious but the result of multi-dimensional structural forces.

The first layer is the "year-end performance push" driven by liquidity factors. From institutional funds to private wealth management, annual ranking mechanisms create strong momentum in December: either locking in profits to secure rankings or betting on year-end comebacks. Once a consensus forms toward an upward trend, year-end buying tends to chase highs rather than hedge risks.

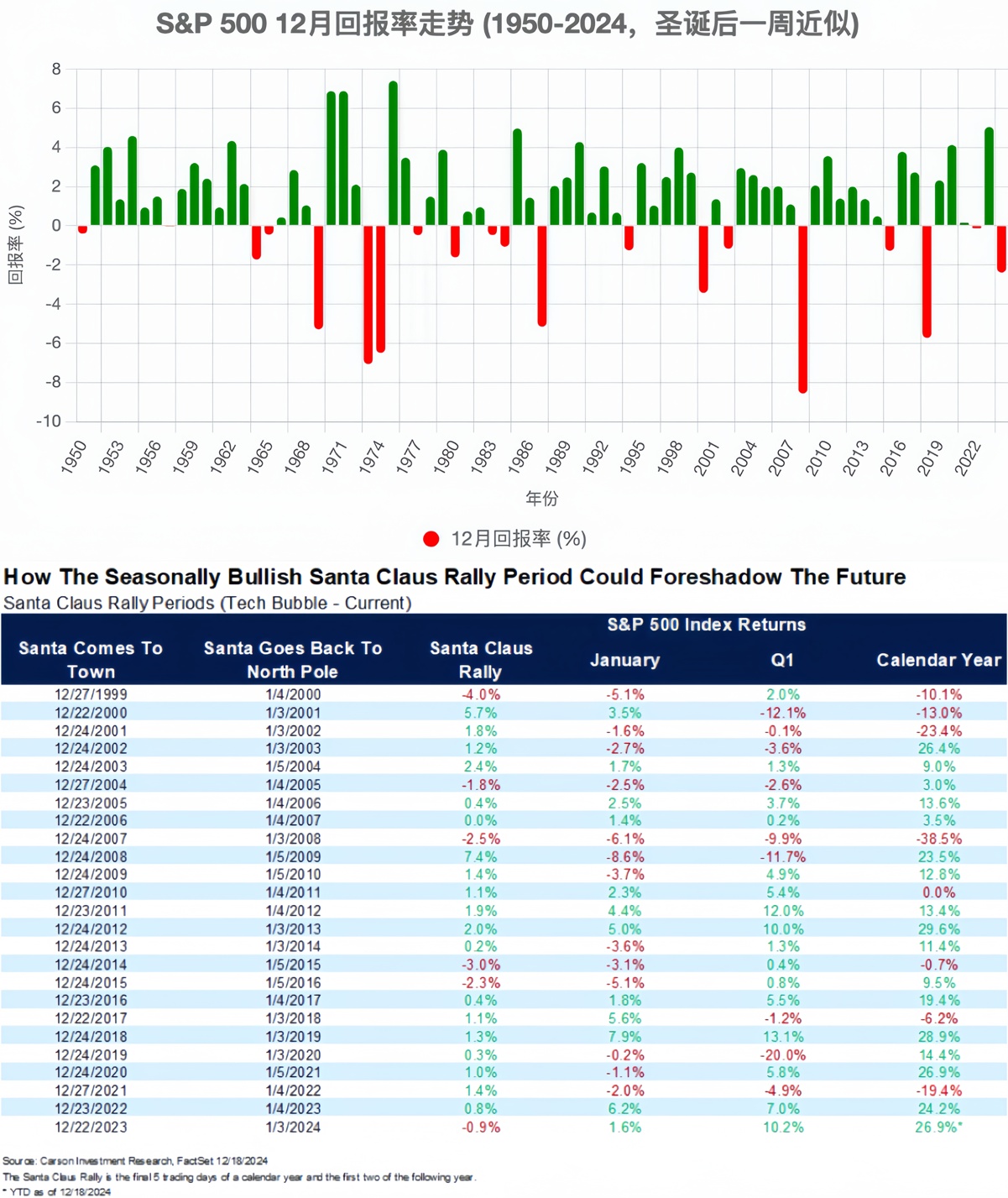

This "can't-lose psychology" directly leads to stronger market sentiment. Historical statistics show that since 1950, the S&P 500 has had a nearly 75% probability of rising in December, with an average gain of about 1.5%—ranking second for the year.

The second layer is the reduction in macroeconomic noise. After November's non-farm payrolls, December's CPI, and year-end fiscal negotiations, macroeconomic influences enter a low-frequency phase. Fed rate decisions, employment data, and geopolitical news fade during the Christmas holiday, and when macro impacts weaken, U.S. tech and growth stocks tend to show more upward elasticity.

Especially in years with strong policy certainty (e.g., confirmed rate cuts, clear election outcomes, improved corporate earnings expectations), December gains are often more pronounced.

The third layer is the structural advantage of capital flows. Against the backdrop of low holiday trading volumes, marginal buying power is amplified. For example, in the trading week of the 18th–22nd, volume often drops significantly, and short-selling declines, smoothing price trends and giving trend-following funds more influence.

Historical data shows that during Christmas week, the VIX volatility index drops by an average of 15%-20%, with a significantly better return-to-drawdown ratio than the annual average.

The fourth layer is sector attributes. The Santa Rally is not a broad-based rise; tech, consumer discretionary, semiconductors, and software services show more pronounced gains. They share two common traits: valuation reliance on expectations + seasonal demand strength.

Examples include e-commerce seasons, ad spending cycles, chip inventory demand, and year-end AI computing procurement. Meanwhile, financials, energy, and industrials often underperform due to low seasonal activity and weak pricing momentum.

But one thing must be clear—the Santa Rally is never a guaranteed rise. This year's key factors are:

(1) Fed rate direction: Whether early rate cuts are confirmed will significantly impact growth stocks;

(2) High U.S. stock valuations: The S&P's 2025 P/E ratio is above historical averages, and any earnings guidance downgrades will amplify negative sentiment;

(3) Risk appetite: Institutions have already locked in "excess returns" in the first half of the year; their willingness to take further risks depends on equity-bond yield expectations.

History also shows failures. Declines occurred in 2015, 2018, and 2022 due to high inflation, balance sheet reduction cycles, and policy uncertainty, proving the Santa Rally isn't mechanically applicable.

For this year's strategy, structural opportunities matter more than index movements:

First, the AI tech chain remains the biggest winner, including GPU servers, power-energy tech, data center REITs, and software subscriptions, as year-end budget releases often confirm their performance.

Second, consumer stocks may see short-term trading windows; if holiday shopping data beats expectations, e-retail platforms and luxury goods could spike.

Third, volatility and bond yields typically decline, offering little opportunity for short-bond ETFs like SGOV and SHY, but benefiting growth stock valuation models.

Fourth, watch for small-cap rebounds—if the Santa Rally holds, the Russell 2000 often surges in the last two weeks.

In short, the Santa Rally isn't about gut feelings but three signals:

(1) VIX falling below 15 with a downtrend;

(2) No downgrades to year-end corporate earnings expectations;

(3) The Fed maintains dovish communication.

If all three hold, the rally will likely continue. If any reverse, caution is needed, especially amid high valuations and structural divergence.

The true meaning of the U.S. stock Santa Rally is never short-term gains but the year-end concentration of market sentiment consensus. It's a mirror reflecting the U.S. economy, global capital flows, institutional risk appetite, and the direction of the AI cycle.

If stocks rise at Christmas, post-Lunar New Year performance likely won't be bad; if they weaken, it signals early defensive positioning—that's the real value to watch.

This is the full conclusion of the U.S. stock Santa Rally.

The copyright of this article belongs to the original author/organization.

The views expressed herein are solely those of the author and do not reflect the stance of the platform. The content is intended for investment reference purposes only and shall not be considered as investment advice. Please contact us if you have any questions or suggestions regarding the content services provided by the platform.