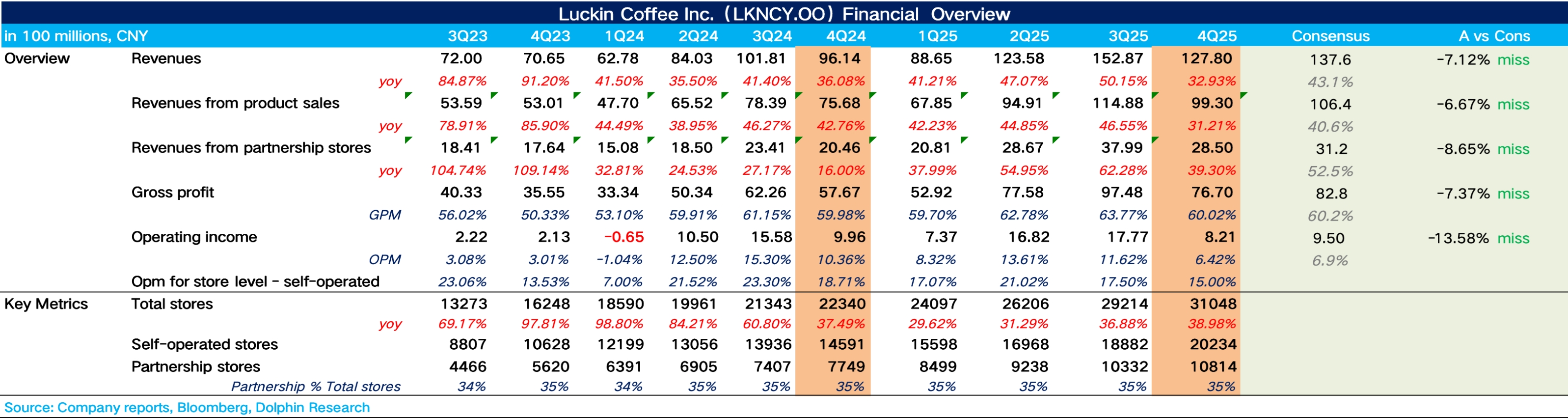

LKNCY 4Q25 First Take: Overall, growth slowed as delivery subsidies eased and Luckin pulled back its own subsidies. The ongoing 'delivery war' kept fulfillment costs elevated and continued to erode margins. As a result, revenue rose but profits did not, with results missing market expectations.

1) Q4 revenue growth was 32.9%, and same-store sales growth (SSSG) decelerated meaningfully QoQ vs. Q2–Q3. This points to a clear slowdown in underlying momentum.

With subsidies tightened and selective price hikes implemented, SSSG suggests pricing power remains limited as consumers are still highly price-sensitive. Cup volume fell short of expectations.

2) Store expansion: 1,884 net new stores were added in Q4, including 42 overseas, with the pace slowing notably. Expansion momentum was intentionally moderated.

Dolphin Research believes the 'delivery war' drove a spike in store fulfillment costs, compressing store-level margins. The company slowed openings to prioritize unit economics.

3) GPM remained broadly stable. On costs, apart from a higher delivery mix keeping the delivery expense ratio elevated, other opex lines were largely steady.

Non-GAAP OP came in at RMB 960 mn, down 13% YoY. $Luckin Coffee(LKNCY.US)

The copyright of this article belongs to the original author/organization.

The views expressed herein are solely those of the author and do not reflect the stance of the platform. The content is intended for investment reference purposes only and shall not be considered as investment advice. Please contact us if you have any questions or suggestions regarding the content services provided by the platform.