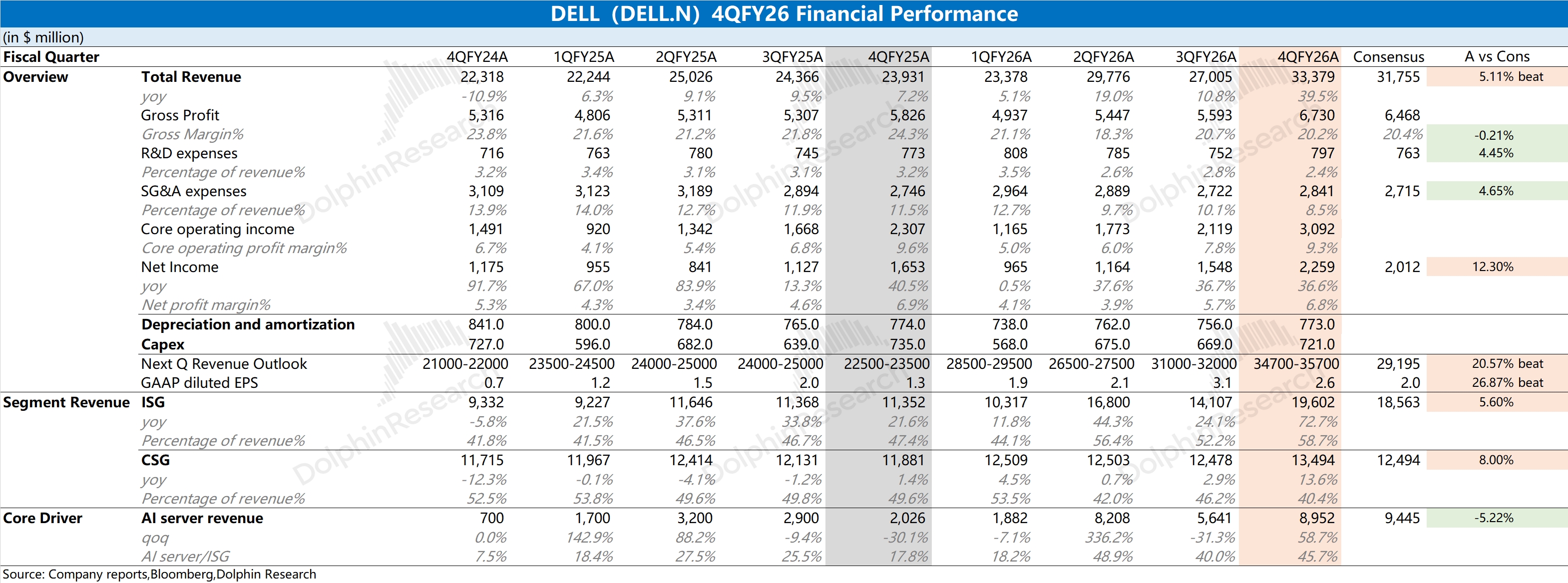

DELL First Take: Results were strong, with revenue up 39% YoY and growth starting to accelerate. This quarter’s expansion was driven by ISG (servers) shipments.

AI revenue reached $8.95bn, up $3.3bn QoQ. In addition, new AI orders hit a record $34.1bn, well ahead of the Street’s $10–11bn. Backlog increased by $43bn by quarter-end, laying the groundwork for sustained high growth ahead.

The outlook is the real surprise vs. this quarter’s prints. Mgmt guides next-quarter revenue to $34.7–35.7bn, with the midpoint up $2bn QoQ and well above the Street’s $31.8bn. Based on the order book, Dolphin Research estimates next-quarter AI revenue could top $11bn, implying QoQ growth of $2bn+.

DELL trades around 10x, a clear discount across the AI value chain, largely due to lower GPM and worries about persistent storage tightness. While storage constraints may pressure legacy biz., the surge in AI orders underpins faster growth in AI.

This eases market concerns to a degree, supporting both earnings and multiple expansion. For details, see Dolphin Research’s detailed take and Trans. $Dell Tech(DELL.US) $DELL 2X Long ETF(DLLL.US)

The copyright of this article belongs to the original author/organization.

The views expressed herein are solely those of the author and do not reflect the stance of the platform. The content is intended for investment reference purposes only and shall not be considered as investment advice. Please contact us if you have any questions or suggestions regarding the content services provided by the platform.