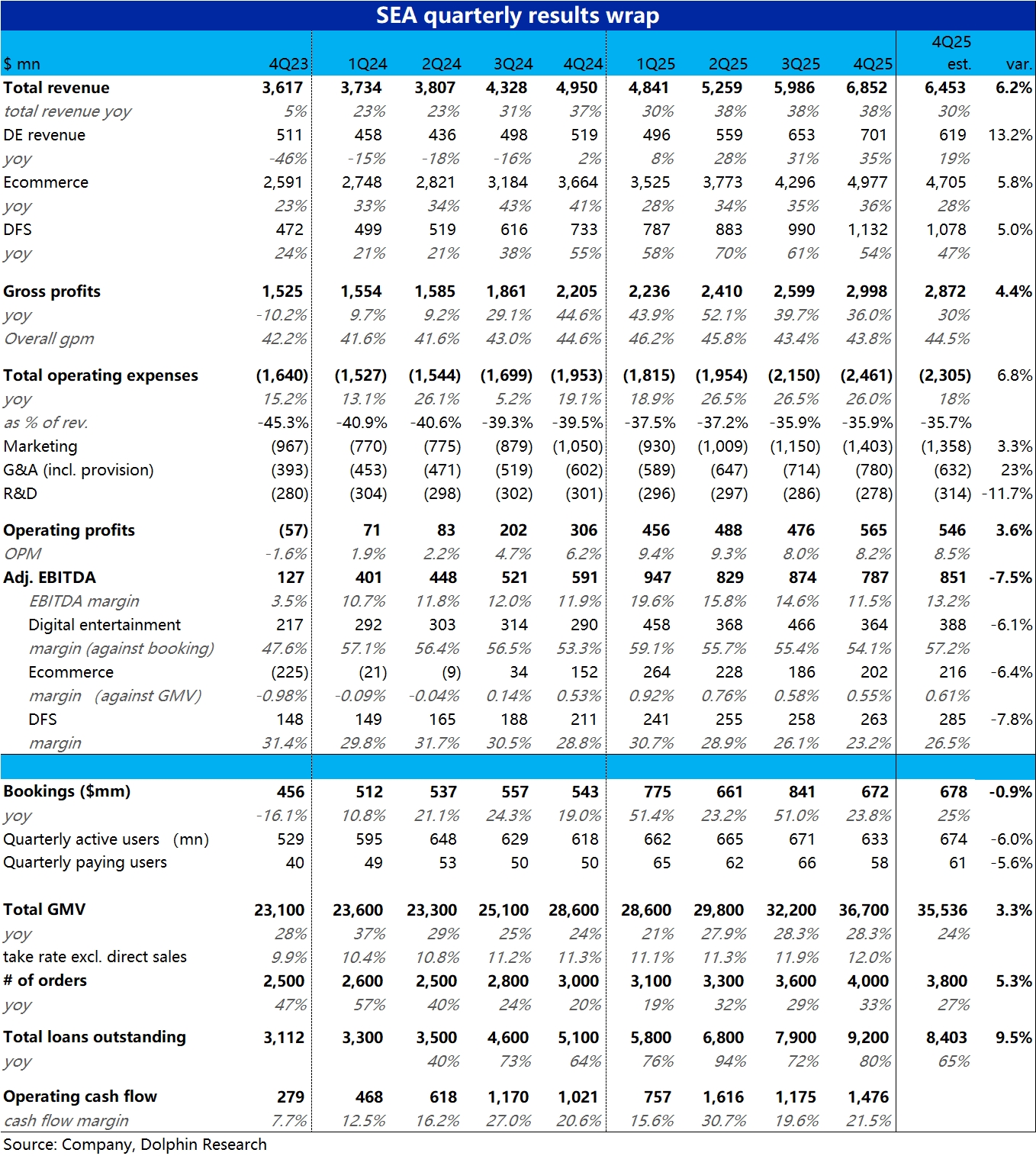

'Little Tencent' Sea 4Q25 First Take: Results showed the familiar split, with business metrics and revenue broadly beating estimates while profits lagged across segments due to heavier investment. The positives and negatives are clear; details as follows:

1) Excluding the less critical games segment, core e-commerce and fintech growth both came in well above expectations. In games, bookings rose Approx. 24% YoY, decelerated QoQ, and ran slightly below the ~25% growth expected.

2) In the most important e-commerce segment, order volume grew 33% YoY vs. 29% last qtr, materially ahead of estimates. Logistics build-out clearly lifted growth. For the first time, GMV and revenue also beat expectations.

3) In fintech, the key metric—outstanding loan balance—grew 80% YoY, re-accelerating vs. last qtr and far exceeding estimates. Revenue showed similarly strong growth.

4) The core issue was opex overshooting estimates by Approx. $50 mn, mainly dragged by a sharp increase in credit loss provisions. Marketing expense also rose ~34% YoY but was broadly in line.Logistics investment in e-commerce showed up in GPM contracting ~90 bps YoY. Together these factors pressured the key profit metric: Adj. EBITDA of Approx. $790 mn, missing by ~$60 mn (~8%), with all three segments below expectations. $Sea(SE.US)

The copyright of this article belongs to the original author/organization.

The views expressed herein are solely those of the author and do not reflect the stance of the platform. The content is intended for investment reference purposes only and shall not be considered as investment advice. Please contact us if you have any questions or suggestions regarding the content services provided by the platform.