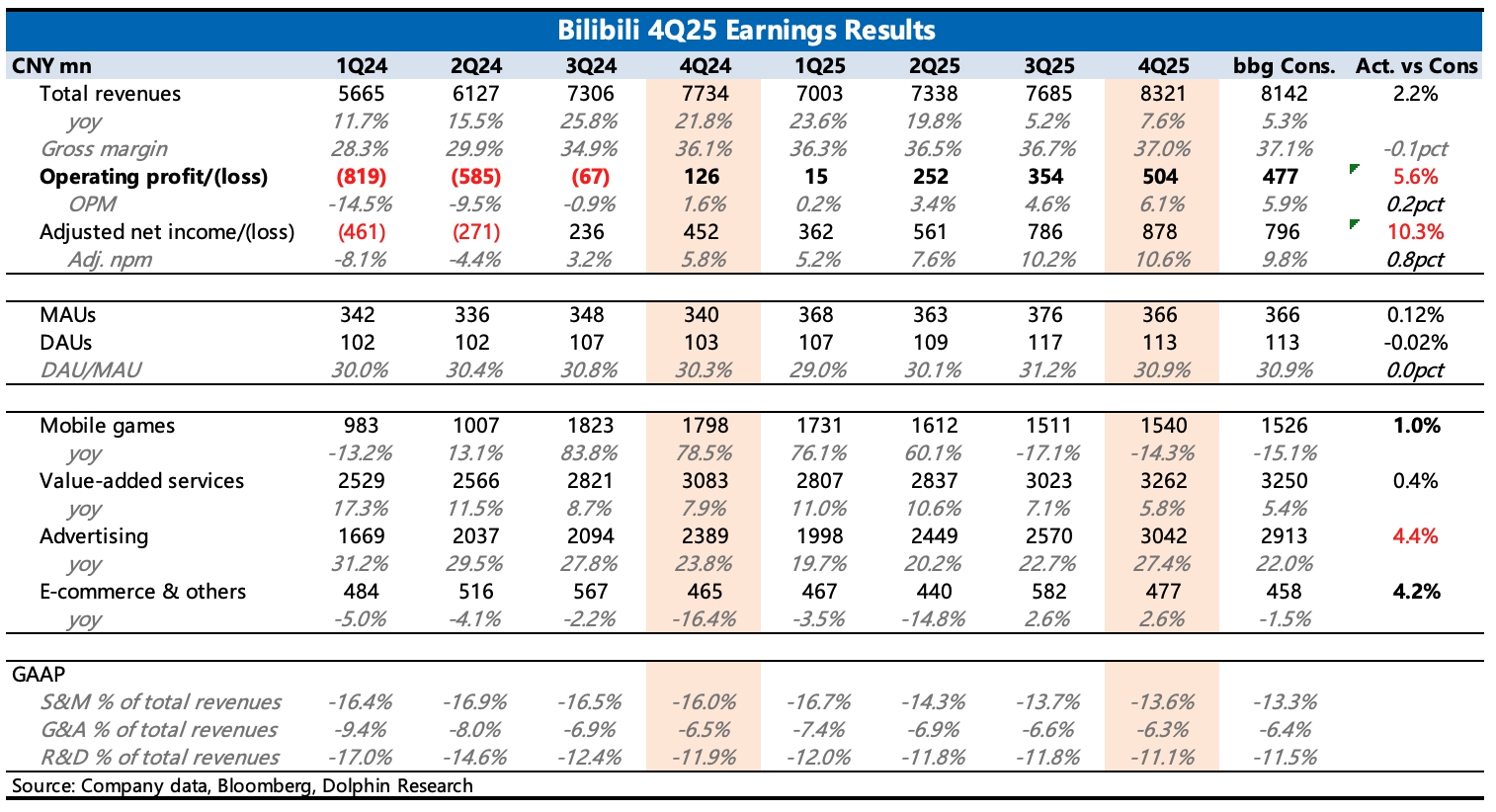

BILI 4Q25 First Take: Q4 results were decent, with ads as the clear bright spot. Other segments were mixed and broadly in line.

Ads grew fast and accelerated QoQ, slightly beating the Street. Beyond healthy ecosystem growth (users and creator content both expanding), gains also came from company-driven initiatives like higher ad load, better ad efficiency, and AIGC ad creation tools.

Tailwinds from short dramas, mini-games, and AI-led content, which fit well with Bilibili's user profile, also helped.

At the early-year marketing event, the company guided to further open up ad inventory in 2026 and to launch a one-stop ad buying platform. We think ad load still has room to rise, and the current ad base is not large vs. peers.

This supports continued high growth in the near to mid term.

With a thin game pipeline weighing on growth, the company kept tuning operating efficiency, driving the three operating expense ratios lower QoQ. Adj. profit reached 880 mn with a margin of 10.6%, up 40bps QoQ.

However, the pace of improvement slowed vs. Q3.

There is still room vs. the 10–15% mid-term margin target. As commercialization deepens this year and the game release cycle improves in H2, profit improvement should reaccelerate.$Bilibili(BILI.US) $BILIBILI-W(09626.HK)

The copyright of this article belongs to the original author/organization.

The views expressed herein are solely those of the author and do not reflect the stance of the platform. The content is intended for investment reference purposes only and shall not be considered as investment advice. Please contact us if you have any questions or suggestions regarding the content services provided by the platform.