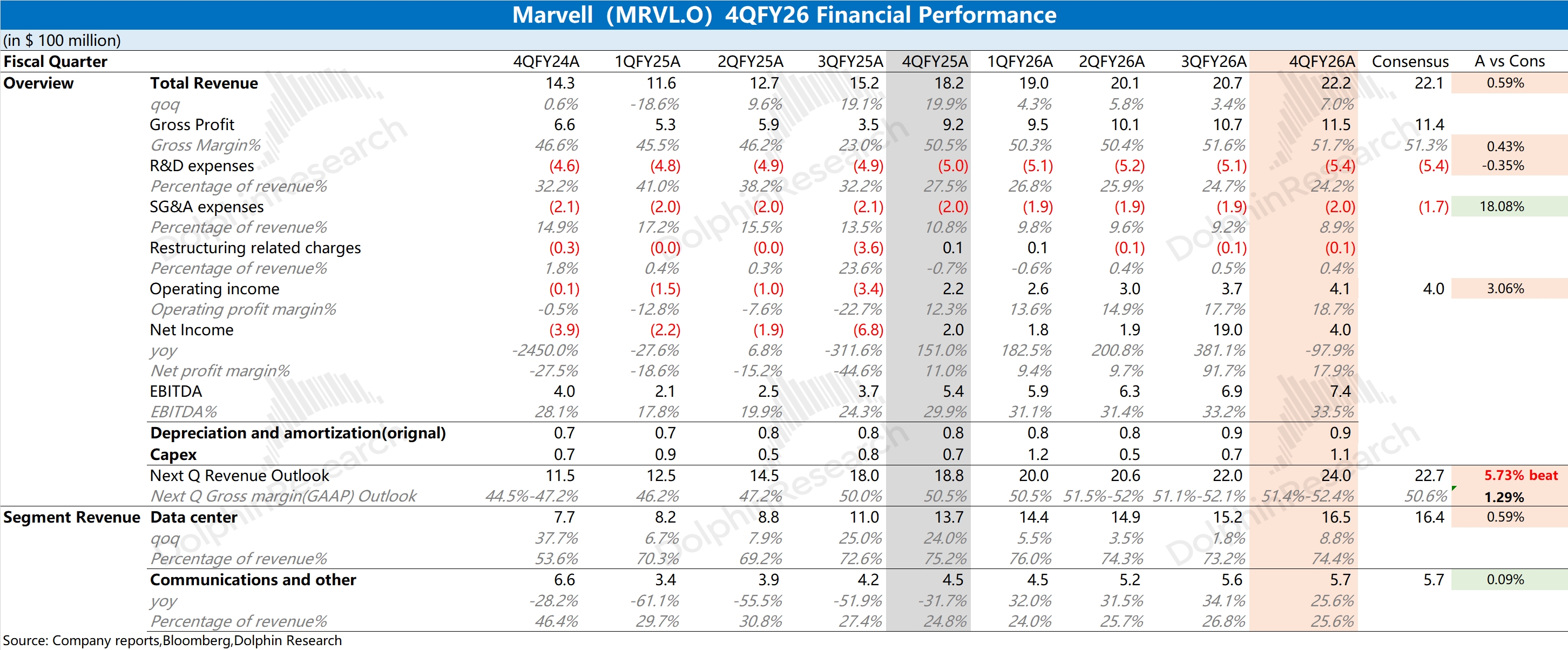

MRVL First Take: Results broadly in line with estimates, with growth largely driven by Data Center.

Adj. GPM at 58.5%, down 50bps QoQ, reflecting a mix shift toward lower-margin custom ASIC.

The company revised segment reporting this quarter, consolidating from five buckets to two (Data Center; Comm. & Other), underscoring Data Center's importance.

Data Center drove growth, up 8.8% QoQ. Dolphin Research estimates AI revenue at approx. $960 mn this quarter.

Beyond the print, guidance was 'quite good'.

MRVL guides next-quarter revenue to $2.4 bn (+8% QoQ), ahead of the Street's $2.27 bn, driven by optical module chips and custom ASIC.

Mgmt again lifted the LT outlook: FY2027 revenue to $11 bn (prev. $10 bn), +34% YoY; FY2028 to $15 bn, ~+40%, a further step-up.

Shares had lagged on worries that its ASIC biz could face intensified competition from Taiwan vendors, weighing on growth.

Guidance implies ASIC growth of just over 20% YoY, while interconnect products (optical module chips) should post strong momentum, underpinning faster top-line growth.

For more, follow Dolphin Research's upcoming notes and Trans. $Marvell Tech(MRVL.US) $MRVL 2X Long ETF(MVLL.US)

The copyright of this article belongs to the original author/organization.

The views expressed herein are solely those of the author and do not reflect the stance of the platform. The content is intended for investment reference purposes only and shall not be considered as investment advice. Please contact us if you have any questions or suggestions regarding the content services provided by the platform.