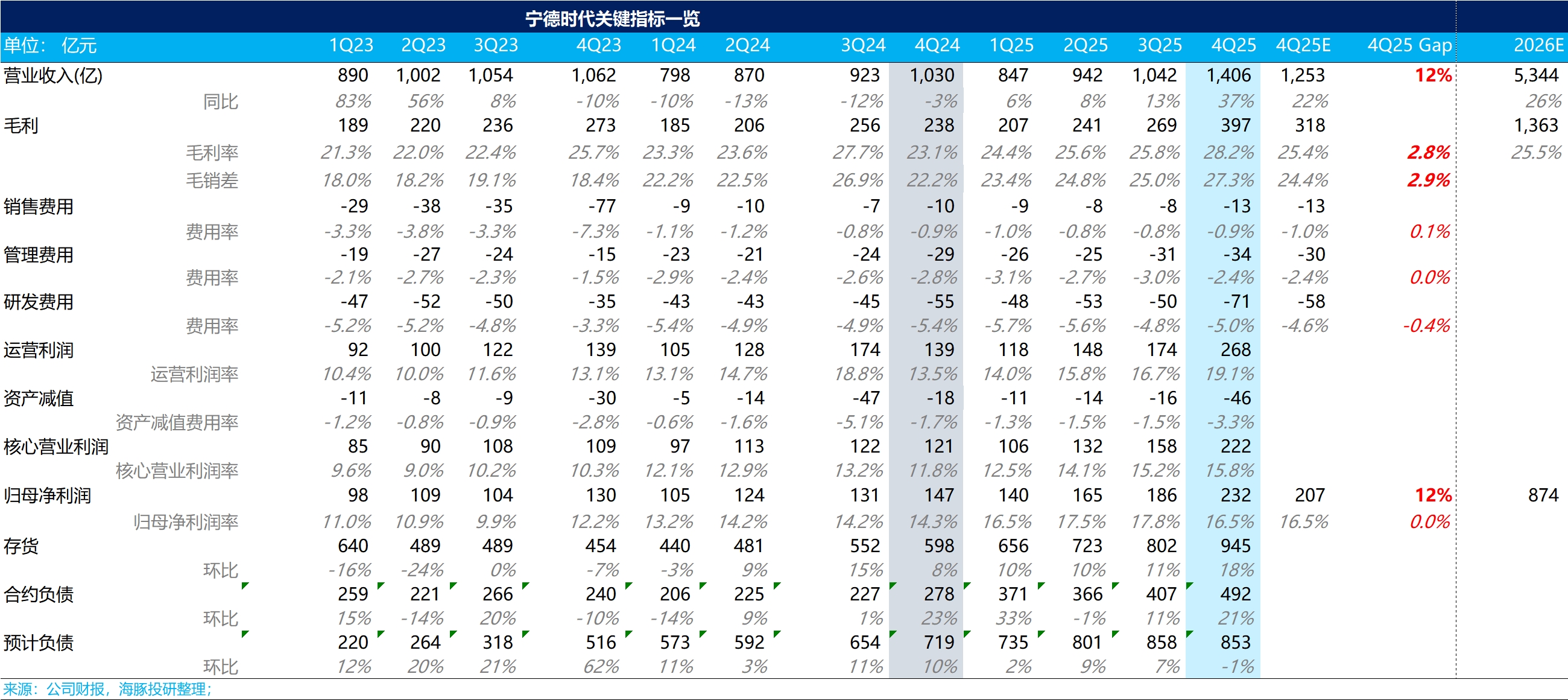

CATL 4Q25 First Take: Q4 was another major beat. It reaffirms the lithium battery sector has entered a new upcycle. Details below:

1) Top line: Q4 revenue was RMB 140.6bn vs. the street's RMB 125.3bn, up 37% YoY. The beat was volume-driven, with battery ASPs broadly flat QoQ.

Shipments reached 226 GWh in Q4, up 56% YoY. This was well ahead of the street's 176 GWh and even above Dolphin Research's read of bullish big-bank estimates at ~200 GWh.

By segment, EV battery shipments were the key upside. They reached 192 GWh in Q4, up 48% QoQ. With NEV unit growth slowing to 23% QoQ, battery growth still outpaced on OEM pre-stocking and higher kWh per vehicle QoQ.

2) GPM was 28.2%, well above the street's 25.4%. This validates CATL's ability to pass through upstream raw-material inflation downstream, easing margin concerns.

3) Running at full tilt. For 2025, capacity utilization reached 96.9%, up 20.6ppt vs. 76.3% in 2024. In 2H alone, utilization hit an eye-catching 102.6%, indicating operations essentially at full capacity.

4) Capex re-accelerated. Q4 capex was RMB 12.3bn, up from RMB 9.9bn in Q3 (+RMB 2.4bn QoQ). After several years of capex contraction, CATL has resumed broad-based capacity expansion.

5) Attributable net profit also beat. Q4 net profit to shareholders was RMB 23.2bn vs. the street's RMB 20.7bn, driven by stronger volumes lifting revenue and GP. The company stepped up R&D spend this quarter (up RMB 2.1bn QoQ to RMB 7.1bn, above the street's RMB 5.8bn) and increased asset impairments, weighing on net margin. Profit per Wh eased to RMB 0.10/Wh from RMB 0.11/Wh QoQ, but in an upcycle the market is likely to look through this small hiccup. $CATL(300750.SZ) $CATL(03750.HK)

---

The copyright of this article belongs to the original author/organization.

The views expressed herein are solely those of the author and do not reflect the stance of the platform. The content is intended for investment reference purposes only and shall not be considered as investment advice. Please contact us if you have any questions or suggestions regarding the content services provided by the platform.