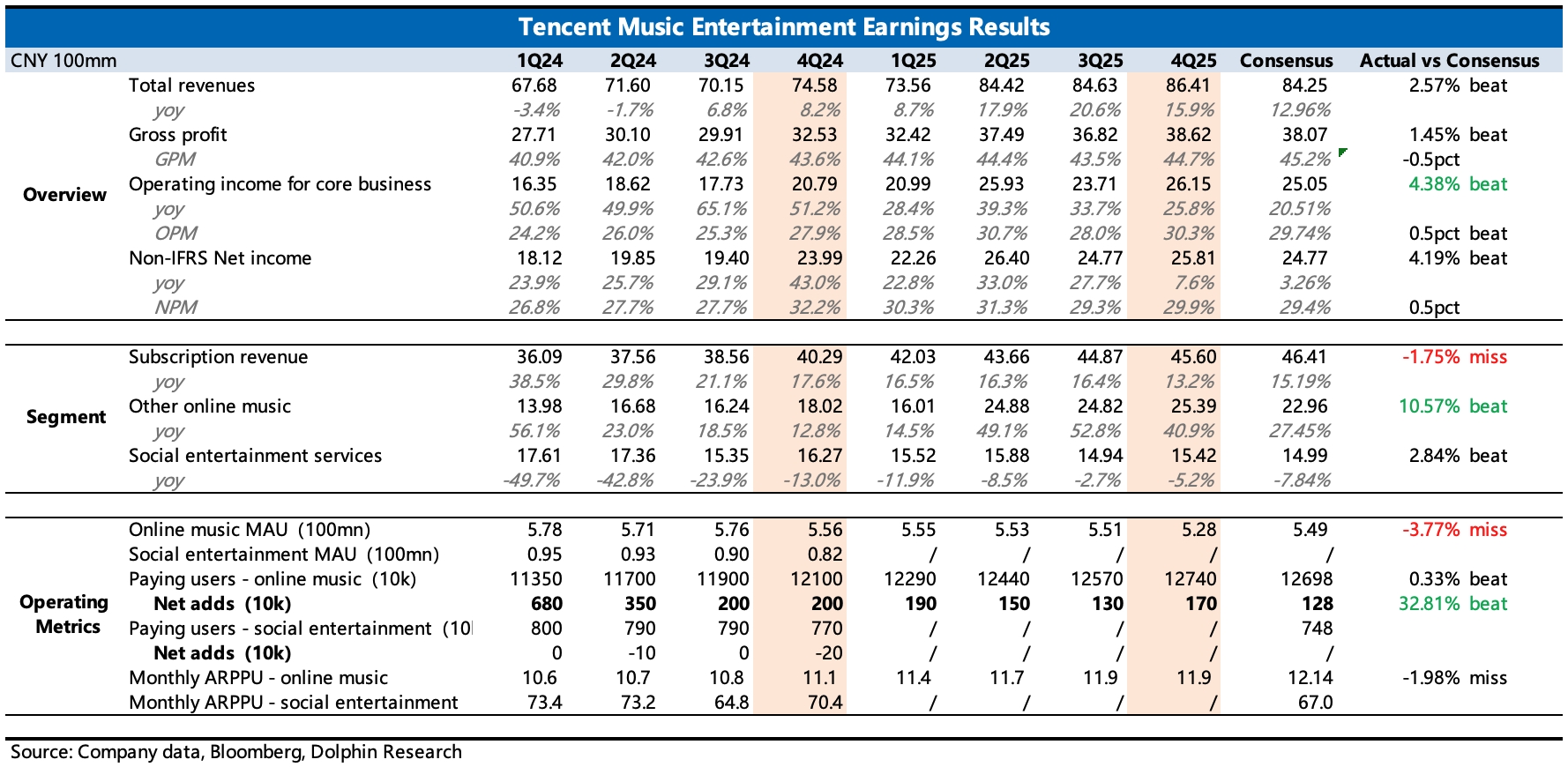

TME 4Q25 First Take: Q4 was mixed. The bright spot was non-subscription music adjacencies, which sustained high growth and helped revenue and profit come in slightly above estimates. That said, user metrics were shaky and subscription growth decelerated, leaving Dolphin Research with a cautious take.

1) User ecosystem: MAUs fell by 23 mn QoQ, a larger drop than typical seasonal churn. Over a longer horizon, the trend remains down, and we would not rule out higher spend to drive acquisition.

2) Subscription growth slowed: Subscription revenue growth eased to 13% in Q4 from 16% in Q3. Net adds were 1.7 mn, a bit higher QoQ. ARPU was flat QoQ.

3) Adjacencies delivered high growth: Other music adjacencies, mainly digital albums and offline concerts, rose 41% YoY. Growth remains robust and an important contributor.

4) Cost control: GPM improved slightly by ~100 bps YoY and QoQ, reflecting economies of scale. Core OP reached RMB 2.6 bn (+26%), slightly ahead of expectations. Opex stayed stable, and we are watching S&M closely as a signal of competitive posture.

For Q4 specifically, we did not see a notable ramp in marketing spend. Given ongoing MAU declines and aggressive moves by rivals, we would not rule out increased promo spend to boost acquisition and slow churn.

Look to management’s earnings call for the forward strategy, including whether they will stay focused or pursue fresh expansion. $Tencent Music(TME.US)

The copyright of this article belongs to the original author/organization.

The views expressed herein are solely those of the author and do not reflect the stance of the platform. The content is intended for investment reference purposes only and shall not be considered as investment advice. Please contact us if you have any questions or suggestions regarding the content services provided by the platform.