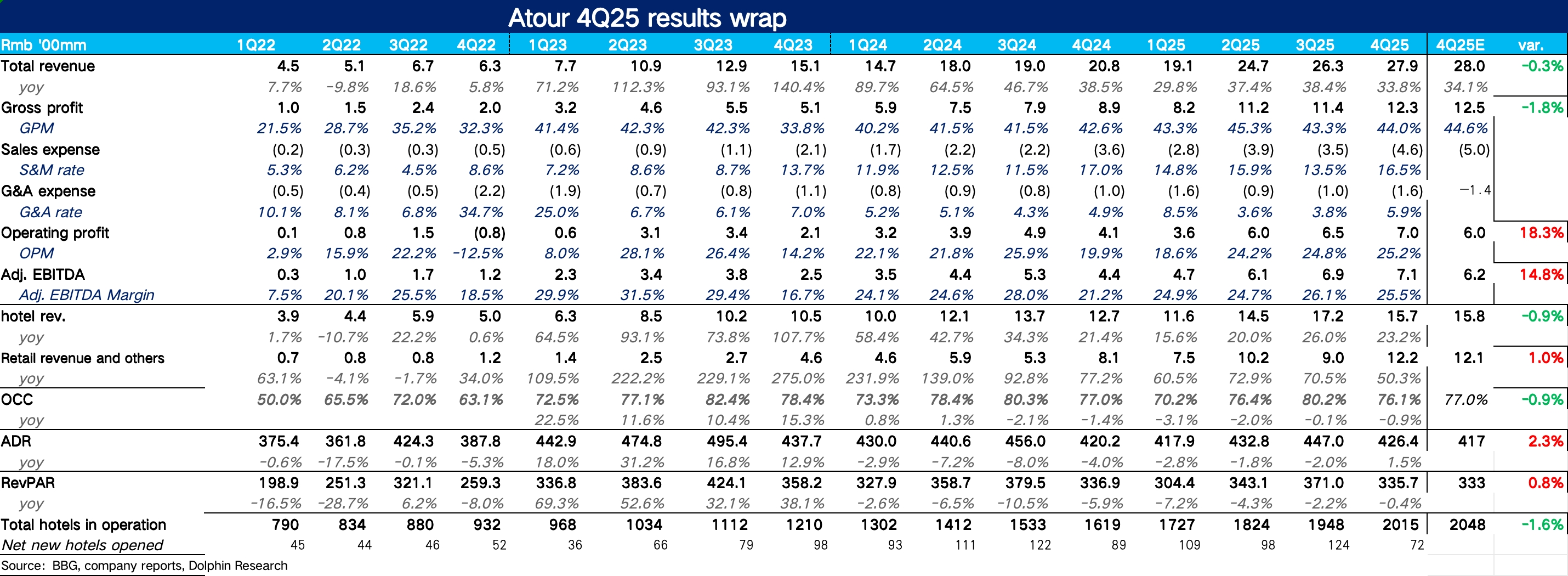

Atour 4Q25 First Take: Overall, a solid quarter. With revenue in line, rapid growth in retail and operating leverage drove a profit beat versus the Street. Specifically:

1) Hotel biz.: OCC fell seasonally in the off-peak quarter and was mediocre. With promotions scaled back and a higher mix of premium S/X lines, ADR turned positive after two years of declines, lifting RevPAR slightly above market expectations.

From the franchise expansion angle, implied net signings rebounded QoQ from Q3. Based on channel checks, Dolphin Research believes franchisees accelerated Atour 4.0 (见野) signings at year-end to capture next spring’s business-travel demand.

2) Retail biz.: Q4 retail grew 50% YoY. Channel checks indicate Atour Planet posted a record conversion rate on Douyin Live and Xiaohongshu, reaching a large non-guest audience. With Q4 being peak season for duvets and temperature-control quilts, we infer temp-control quilts took a larger share of retail GMV.

3) Profit: Fueled by strong sales of high-ticket, high-margin retail SKUs, Q4 GPM expanded 130bps YoY. S&M and G&A declined as operating leverage kicked in, and core OP reached RMB 700 mn (+71% YoY), beating market expectations.$Atour(ATAT.US)

The copyright of this article belongs to the original author/organization.

The views expressed herein are solely those of the author and do not reflect the stance of the platform. The content is intended for investment reference purposes only and shall not be considered as investment advice. Please contact us if you have any questions or suggestions regarding the content services provided by the platform.