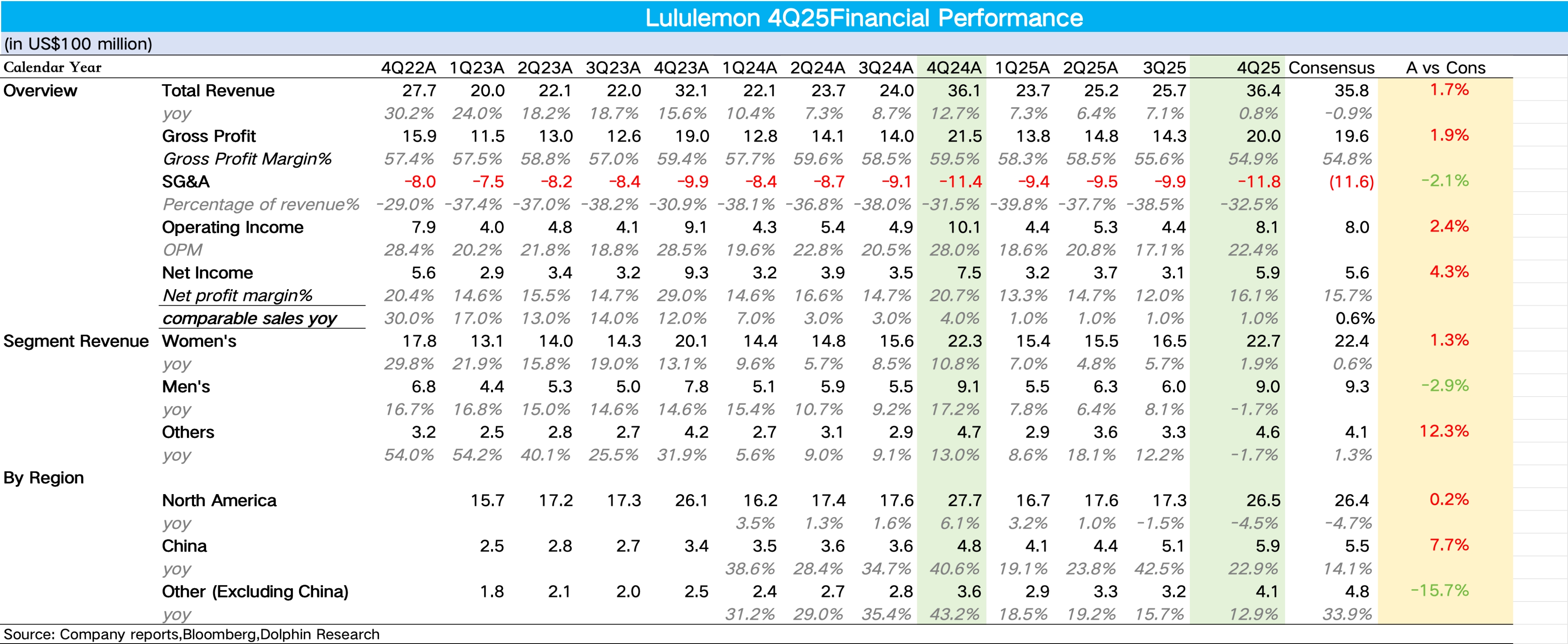

LULU Q4 FY25 First Take: Overall, performance met a low bar and was broadly in line with muted expectations, with key metrics still soft. The market had already baked in weak results after multiple guidance cuts. Revenue eked out positive growth and came in slightly above the company’s prior guide.

1) Revenue by category: Women’s delivered RMB 2.27 bn, up 1.9% YoY. Despite consumer fatigue in N. America and tougher competition from emerging brands, women’s remains the core revenue driver, but growth has slowed to the lowest single-quarter rate in three years.

Men’s came in at RMB 900 mn, down 1.7% YoY. This marks the first negative print, indicating limited traction.

By region, the largest issue is still in N. America, down 4.5% YoY. While the Thanksgiving shopping season was strong and Black Friday set a record for single-day online sales, momentum cooled notably afterward, and heavy discounting points to soft demand. China and other regions also slowed on a high base last year.

2) Margins: GPM fell 460 bps YoY, pressured by ongoing tariff headwinds and deeper discounting to clear inventory. The opex ratio rose ~100 bps on Intl expansion and investment in digital & supply chain. Dolphin Research estimates core OPM at 22.5%, down 560 bps. $Lululemon(LULU.US)

The copyright of this article belongs to the original author/organization.

The views expressed herein are solely those of the author and do not reflect the stance of the platform. The content is intended for investment reference purposes only and shall not be considered as investment advice. Please contact us if you have any questions or suggestions regarding the content services provided by the platform.