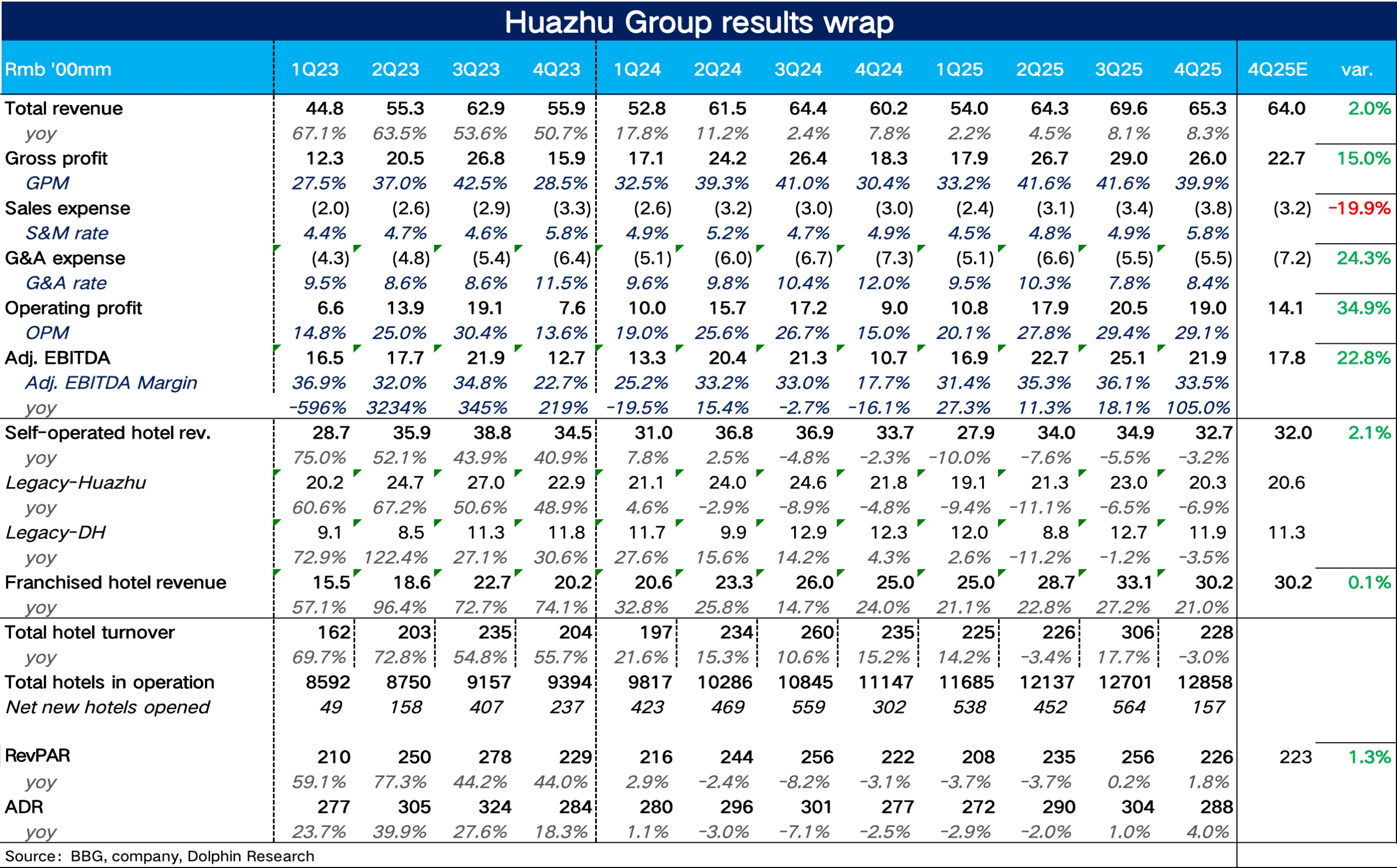

H World 4Q25 First Take: Overall, Q4 sustained the strong Q3 momentum, with revenue beating the top end of guidance. On profitability, a higher franchise mix and digital-driven efficiency lifted core OP well above market expectations.

1) Revenue: total revenue rose 8.3% YoY, exceeding the prior 2%–6% guide and showing a modest QoQ acceleration. From an expectations lens, the market already anticipated rapid franchise growth, so self-operated hotels were the key driver of the revenue beat. Dolphin Research believes Tier-1 business activity recovered, with higher ADR pushing RevPAR up sharply.

2) Profit: with franchise revenue mix up materially vs. last year, GPM expanded by 950bps. Q4 saw a tactical push to raise mid-to-upscale brand exposure via social media seeding and ads, lifting the sales expense ratio.

However, the rising franchise mix drove a sharp decline in the management expense ratio, and Adj. EBITDA came in well above market expectations.

3) Guidance: for 2026, the company guided revenue growth of 2%–6%. Franchise revenue is expected to grow 12%–16%, a step-down vs. 2025, but new openings are still brisk at 2,200–2,300. $HWORLD-S(01179.HK) $H World(HTHT.US)

The copyright of this article belongs to the original author/organization.

The views expressed herein are solely those of the author and do not reflect the stance of the platform. The content is intended for investment reference purposes only and shall not be considered as investment advice. Please contact us if you have any questions or suggestions regarding the content services provided by the platform.