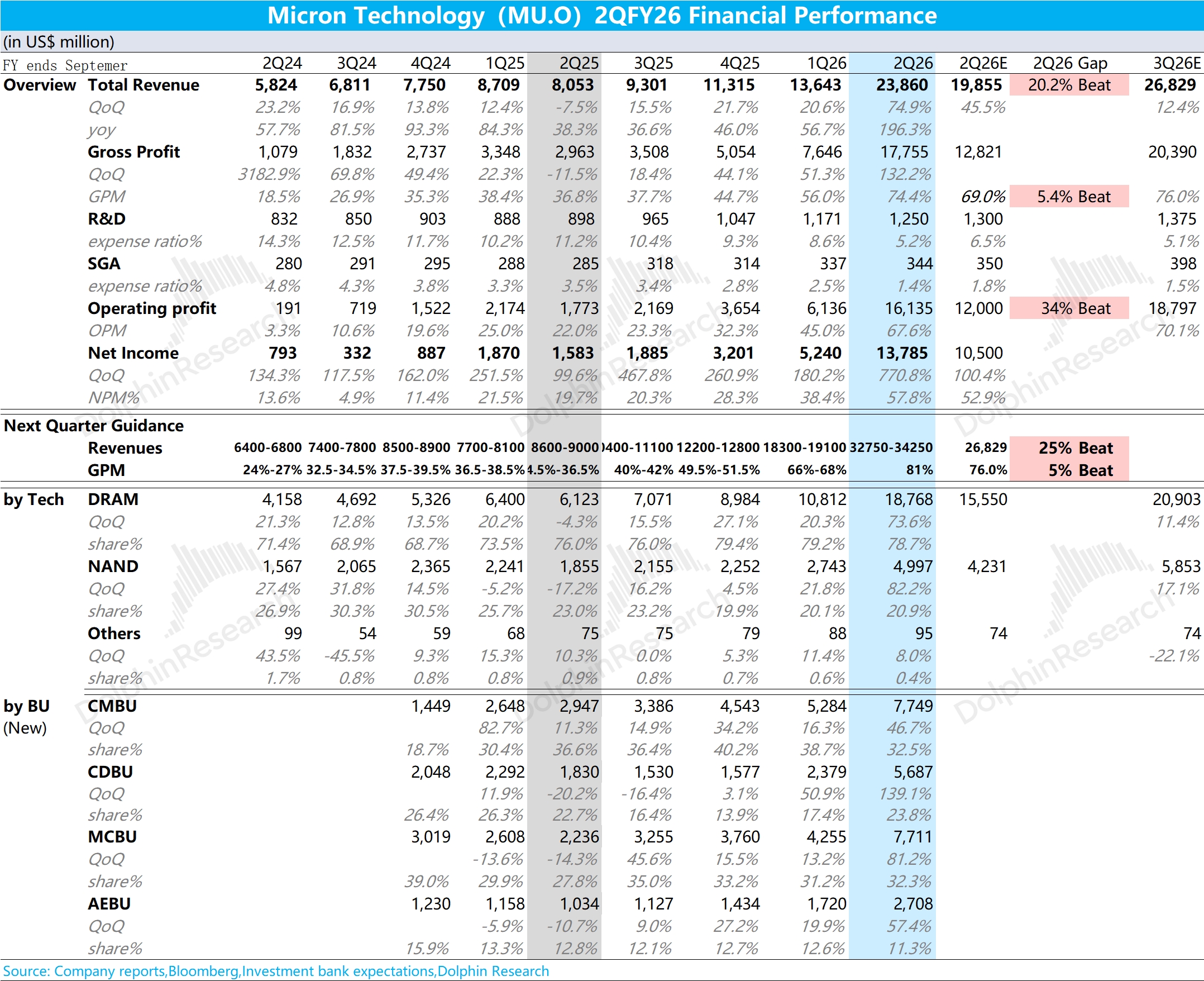

MU First Take: Revenue and GPM came in well above market expectations this quarter. With shipments up modestly, growth was driven primarily by steep increases in memory pricing. The company has resegmented its biz.; by unit:

Beyond faster growth in the Cloud Memory BU (CMBU), the Core Data Center BU (CDBU) and the Mobile & Client BU (MCBU) were the main growth drivers this quarter, supported by sharp price hikes in traditional memory products. Guidance for next quarter is well above consensus.

Micron guides next-quarter revenue of $33.5bn (±$750mn). QoQ growth of $9.6bn tops the market's $26.8bn expectation.

GPM is guided to ~81%, well above buy-side at 76%. This points to another major round of memory price hikes next quarter.

Based on current memory pricing, the near-term 'blowout' in results is largely priced in. In a broad memory upcycle, investors care more about 'sustainability' than the peak level of earnings.

Beyond the earnings beat, focus on management commentary around long-term contract orders and customer fulfillment. Also watch the demand outlook for 2027 and beyond.

If more customers are willing to lock in supply through long-term agreements, earnings durability improves. For details, follow Dolphin Research's upcoming commentary and Trans. $Micron Tech(MU.US) $MU 1X Short ETF(MUD.US) $MU 2X Long ETF(MUU.US)

The copyright of this article belongs to the original author/organization.

The views expressed herein are solely those of the author and do not reflect the stance of the platform. The content is intended for investment reference purposes only and shall not be considered as investment advice. Please contact us if you have any questions or suggestions regarding the content services provided by the platform.