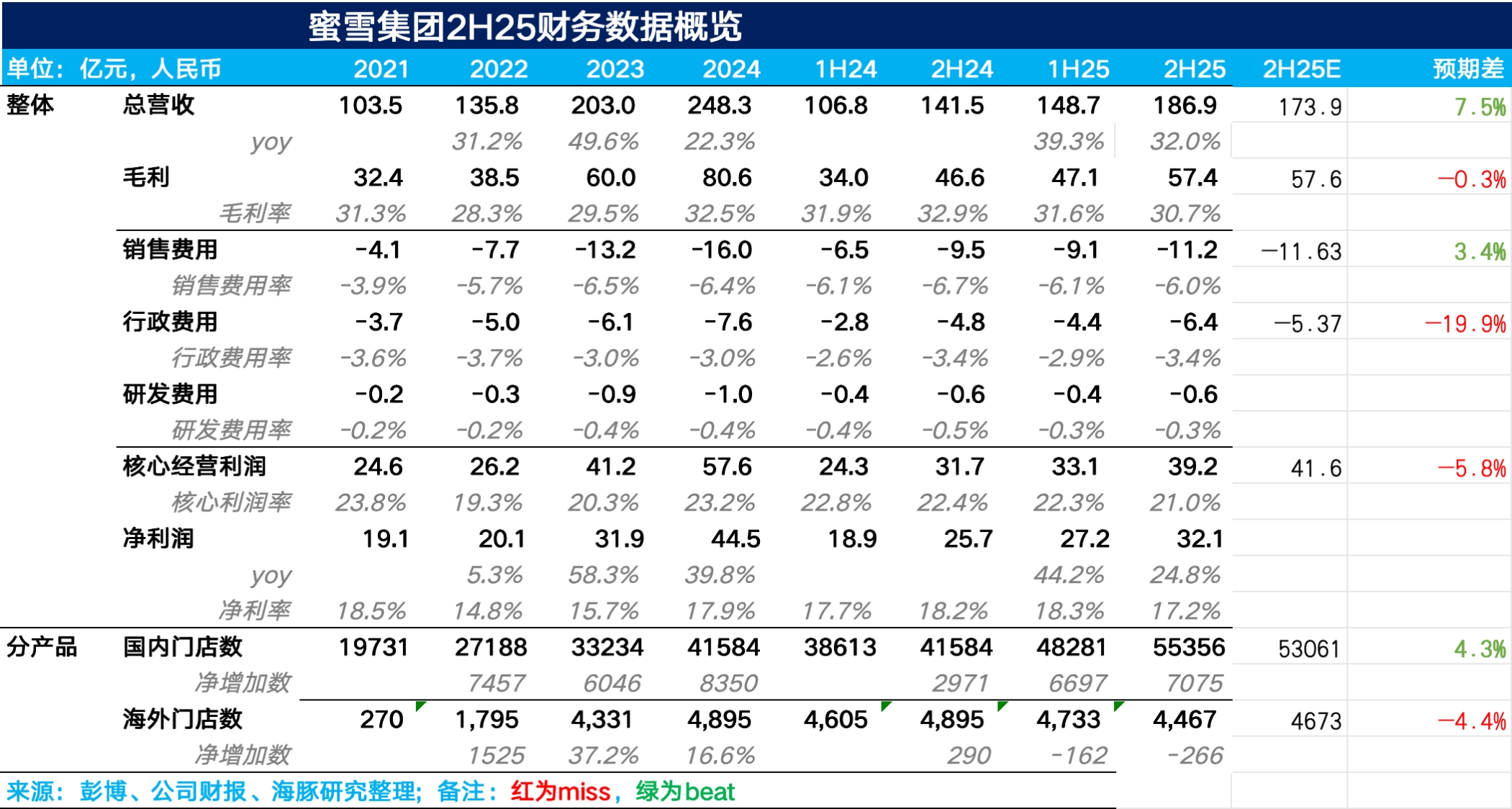

Mixue Group 2H25 First Take: Overall, second-half results were mixed, with revenue beating expectations. However, a lower GPM and higher admin expenses left core OP slightly below consensus.

1) Revenue: 2H25 revenue reached RMB 18.7bn (+32% YoY), and with store count up 33% YoY, growth was largely driven by expansion rather than same-store sales. With weaker delivery subsidies in 2H, Dolphin Research estimates low single-digit same-store revenue growth, driven by higher cup volume. The average selling price per cup was likely flat to slightly down.

2) Store openings: Mixue added 6,809 stores in 2H, accelerating vs. 1H. Growth skewed to lower-tier cities, while overseas store count fell by 266 vs. 1H. Dolphin Research believes the company continued pruning overlapping, underperforming, and less-compliant stores in Southeast Asia.

3) GPM: To protect franchisee economics amid slowing same-store growth, Mixue likely lowered supply prices on core inputs (e.g., milk base, jams) to franchisees. As a result, GPM fell 220bps to 30.7%.

Sales expenses benefited from the maturation of the Snow King IP, with low-cost social traffic substituting for traditional ads, bringing the sales expense ratio down 70bps to 6%. Admin expenses were temporarily elevated by one-off integration costs from the Oct acquisition of "鲜啤福鹿家".

Mixue delivered net profit of RMB 3.21bn (+25% YoY). For more details and our views, please follow Dolphin Research’s forthcoming earnings review and call transcript. $MIXUE GROUP(02097.HK)

The copyright of this article belongs to the original author/organization.

The views expressed herein are solely those of the author and do not reflect the stance of the platform. The content is intended for investment reference purposes only and shall not be considered as investment advice. Please contact us if you have any questions or suggestions regarding the content services provided by the platform.