Hesai 4Q25 First Take: Results again showed high shipment growth driven by price compression. The company protected margins via solid cost control and issued upbeat 2026 shipment guidance.

I. 4Q25 results: volumes up, prices down, profitability remained resilient

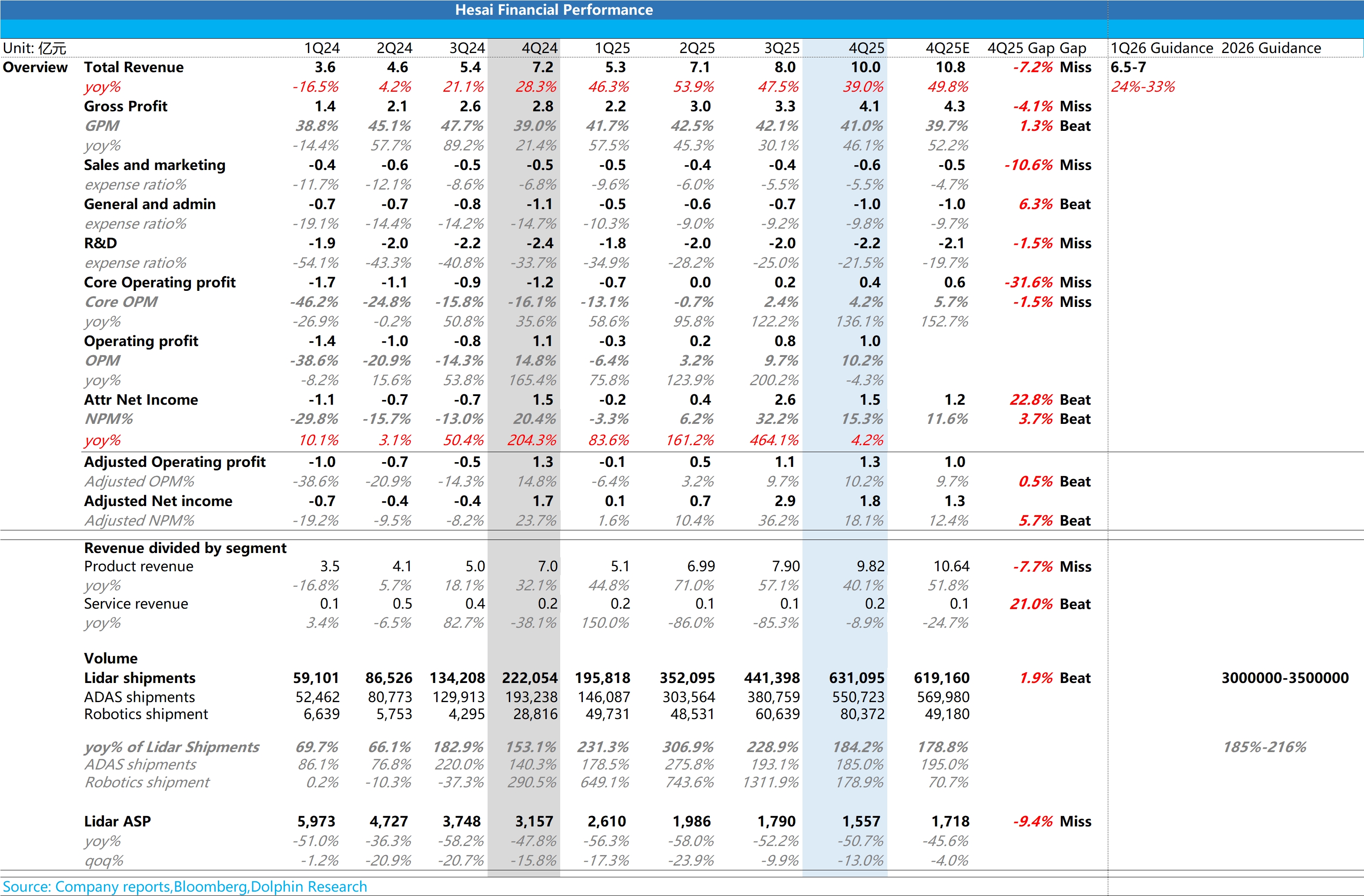

1) Revenue: RMB 1.0 bn, +39% YoY. This was at the low end of prior guidance (RMB 1.0–1.2 bn) and slightly below the RMB 1.08 bn consensus.

Shipments: 631k units, +184% YoY, beating guidance (600k) and the 619k consensus. Growth was driven by robot LiDAR (80k units, above the 50k expected) and the continued ramp of ADAS LiDAR (550k units).

ASP: RMB 1,557, down 51% YoY and 13% QoQ, well below the RMB 1,718 the market expected. This directly explains the revenue miss vs. consensus.

Dolphin Research sees three main drivers of the faster ASP decline:

a) Product mix shift: the low-priced 'thousand-yuan' ATX rose from 70% in Q3 to ~80% in Q4. It accelerated the replacement of the older AT128, which sells for multiples of that price.

b) Proactive discounts: to defend share, the co. offered ATX discounts to key customers in Q4. This weighed on blended pricing.

c) Robot mix: within robot shipments, the lower-priced JT series likely accounted for a higher share. This further dragged ASP.

2) Despite a sharp ASP decline, HSAI showed resilient profitability. Margin held up better than feared.

GPM: 41.0%. This was above the 39.7% consensus and the company's 40% guide.

We attribute this to scale benefits from higher volumes and ongoing cost downs from in-house ASICs, supply-chain optimization, and factory automation. These gains offset pricing pressure.

3) Net profit at the top end: GAAP net profit was RMB 150 mn, at the high end of guidance (RMB 70–170 mn). This was boosted by interest income and other gains (~RMB 120 mn). In Q4, HSAI received ~$6.4 mn (~RMB 45 mn) in IP arbitration compensation from Ouster.

Excluding these items, core OP was ~RMB 40 mn (GP minus core Opex), slightly below the RMB 60 mn expected, mainly due to higher R&D and S&M QoQ. Overall, expense control remained disciplined.

II. 2026 guidance: shipment targets raised materially

Mgmt is upbeat on 2026, guiding well above prior market expectations. The tone signals confidence in volume growth.

2026 shipment guide: 3.0–3.5 mn units (+185%–216% YoY). This is a major step-up from the prior 2.0–3.0 mn range and is well above the 2.66 mn street. To support this, the co. plans to double annual capacity to 4.0 mn units from 2.0 mn in 2025.

Q1 pricing likely stable to up: 2026 Q1 net revenue guidance is RMB 650–700 mn (+24%–33% YoY). Given Q1 is typically a seasonal trough for autos (about 12% of annual shipments historically), the midpoint of the full-year guide implies ~393k units in Q1.

Back-solving implies a blended Q1 ASP of ~RMB 1,675, slightly above 4Q25's RMB 1,557. We think this reflects slower passenger-car LiDAR shipments in Q1 and a higher mix of higher-priced robot/industrial LiDAR. $Hesai(HSAI.US) $HESAI-W(02525.HK)

The copyright of this article belongs to the original author/organization.

The views expressed herein are solely those of the author and do not reflect the stance of the platform. The content is intended for investment reference purposes only and shall not be considered as investment advice. Please contact us if you have any questions or suggestions regarding the content services provided by the platform.