$Unity Software(U.US) rallied after hours on a Q1 pre-announcement, with revenue and profit both topping prior guidance. It also said it will divest IronSource and Supersonic by end-Apr, effectively shedding the overpaid M&A overhang from the prior leadership team.

This will reduce revenue scale and narrow the footprint, diluting the once-aspirational end-to-end moat. For Unity, where operating efficiency has been middling, that may not be a bad trade-off. The carve-outs should sharpen focus, lower execution burden on mgmt, and preserve core strengths.

1、广告:轻装上阵、Vector 超预期

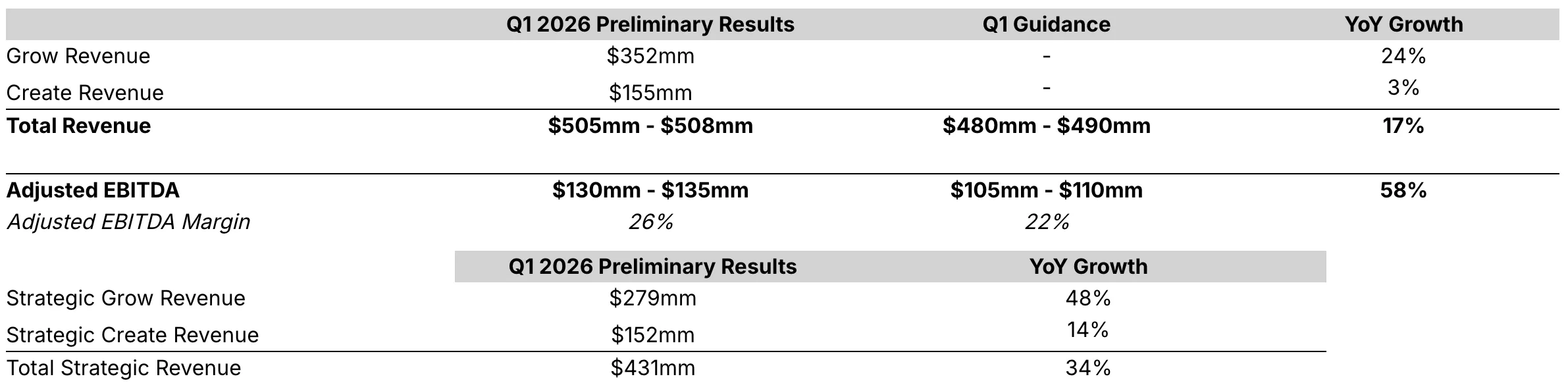

Grow rose 24% YoY; ex-IronSource and Supersonic, it was up 48% YoY. IronSource has been a drag for more than a quarter, so the key marginal driver here is Vector, which is guided to grow 15% QoQ vs. prior 10%.

IronSource is expected to contribute only 6% of Q1 Grow, so the divestiture’s impact should be limited, with core ad tech absorbed over the past three years. Integration between the two teams had frictions, and LevelPlay (the mediation platform), once separate from Unity, can partner more openly with Unity’s competitors.

2、引擎:核心业务稳定增长,继续关注 AI 侵蚀影响

Create grew 3% YoY; ex-Weta and professional services, the core engine was up 14% YoY (vs. 16% last quarter, with quarterly growth around 15% over the past year), in line with guidance. Divestiture effects continue to fade and the core engine is growing steadily, with no visible AI erosion yet.While Dolphin Research believes LLMs are unlikely to disrupt the Unity engine in the near to medium term (see《血洗游戏股,谷歌打出 ‘灭霸’ 响指》), there could be partial impact. Given the rapid pace of AI, we will keep watching developments.

3、利润:经营效率整体提升

Adj. EBITDA modestly beat in Q1, and margins should improve after the IronSource & Supersonic carve-outs. The goodwill and other amortization tied to the premium IronSource deal will be taken at disposal, and Supersonic’s lower margin vs. ads means post-spin profitability should converge toward ad-like levels.

Although investors mainly track adj. EBITDA, some funds will also watch GAAP margins. Intangible amortization expense is nearly 24% of total revenue, accounting for about half of total adjustments.

4、估值:当下仍定价了更多 AI 侵蚀的悲观预期

With the business reset, we update valuation accordingly. We assume a neutral case.

(1) Grow: neutral to slightly constructive. About 20% of Grow will be carved out in Q1; the remaining strategic core, primarily Unity Ads, is roughly $280mn. Vector was $190mn last quarter; +15% QoQ implies ~$220mn in Q1, already ~80% of the core.

Assuming Vector sustains ~10% QoQ growth through the year, FY revenue would be ~$1.01bn. Adding ~$240mn from other Grow (held flat at ~$60mn in Q1, annualized) and ~$73mn from IronSource & Supersonic yields total Grow of ~$1.32bn.

(2) Create: neutral stance with cautious valuation. At a 5% growth rate (with carve-out effects), FY revenue is ~$650mn.

(3) Grow at 6–7x P/S (raised from 5x to reflect segment adj. EBITDA margin moving from ~25% to 30%+) is worth ~$7.9–9.2bn. Create at 3–4x (cut from 7x to align with pressured top-tier SaaS and to price in some AI erosion) is worth ~$2.0–2.6bn.

Sum-of-the-parts is ~$9.9–11.8bn. Versus the current after-hours market cap of ~$8.4bn, there is still room, suggesting the market continues to price in heavier future AI erosion.

The copyright of this article belongs to the original author/organization.

The views expressed herein are solely those of the author and do not reflect the stance of the platform. The content is intended for investment reference purposes only and shall not be considered as investment advice. Please contact us if you have any questions or suggestions regarding the content services provided by the platform.