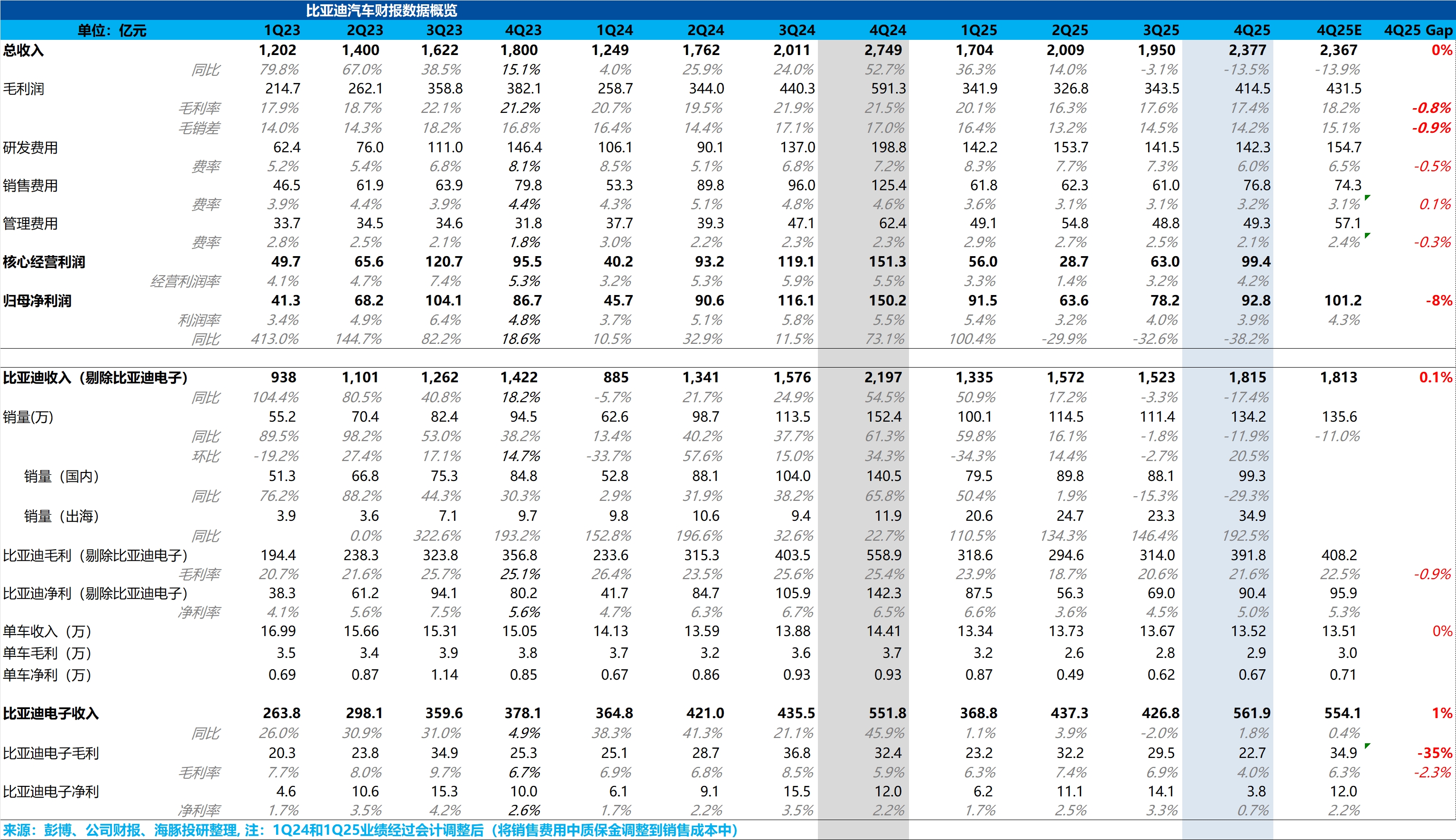

BYD 4Q25 First Take: Overall, Q4 results still missed expectations. Revenue beat, but the outperformance came mainly from the non-core BYD Electronics unit. As for the core auto biz:

① Q4 auto revenue was RMB 181.5bn, in line with the Street. However, ASPs continued to decline.

② Auto GPM and net profit per vehicle missed. The Street had expected at least a 200bps QoQ rebound in auto GPM to 22.5% on a cooler price war, Q4 scale benefits, and a stronger overseas mix. Net profit per vehicle was expected to recover to RMB 7.1k, still well below the ~RMB 9.0k run-rate in 2024.

However, auto GPM and net profit per vehicle still fell short, with net profit per vehicle at only RMB 6.7k. Insufficient unit-cost declines and a sharp QoQ jump in selling expenses constrained margin expansion. Domestic auto sales remained under heavy pressure in Q4. $BYD(002594.SZ) $BYD COMPANY(01211.HK)

The copyright of this article belongs to the original author/organization.

The views expressed herein are solely those of the author and do not reflect the stance of the platform. The content is intended for investment reference purposes only and shall not be considered as investment advice. Please contact us if you have any questions or suggestions regarding the content services provided by the platform.