Dongpeng Bev.: Energy Drinks Stall, Hydra in infant—Is Growth Story Over?

On the evening of Mar 30 Beijing time, Dongpeng Beverage (605499.SH) released its 4Q25 results. With the core energy drink business decelerating, overall performance was lukewarm, and multiple operating metrics missed the Street. Key takeaways are as follows: $EASTROC BEVERAGE(605499.SH) $EASTROC(09980.HK)

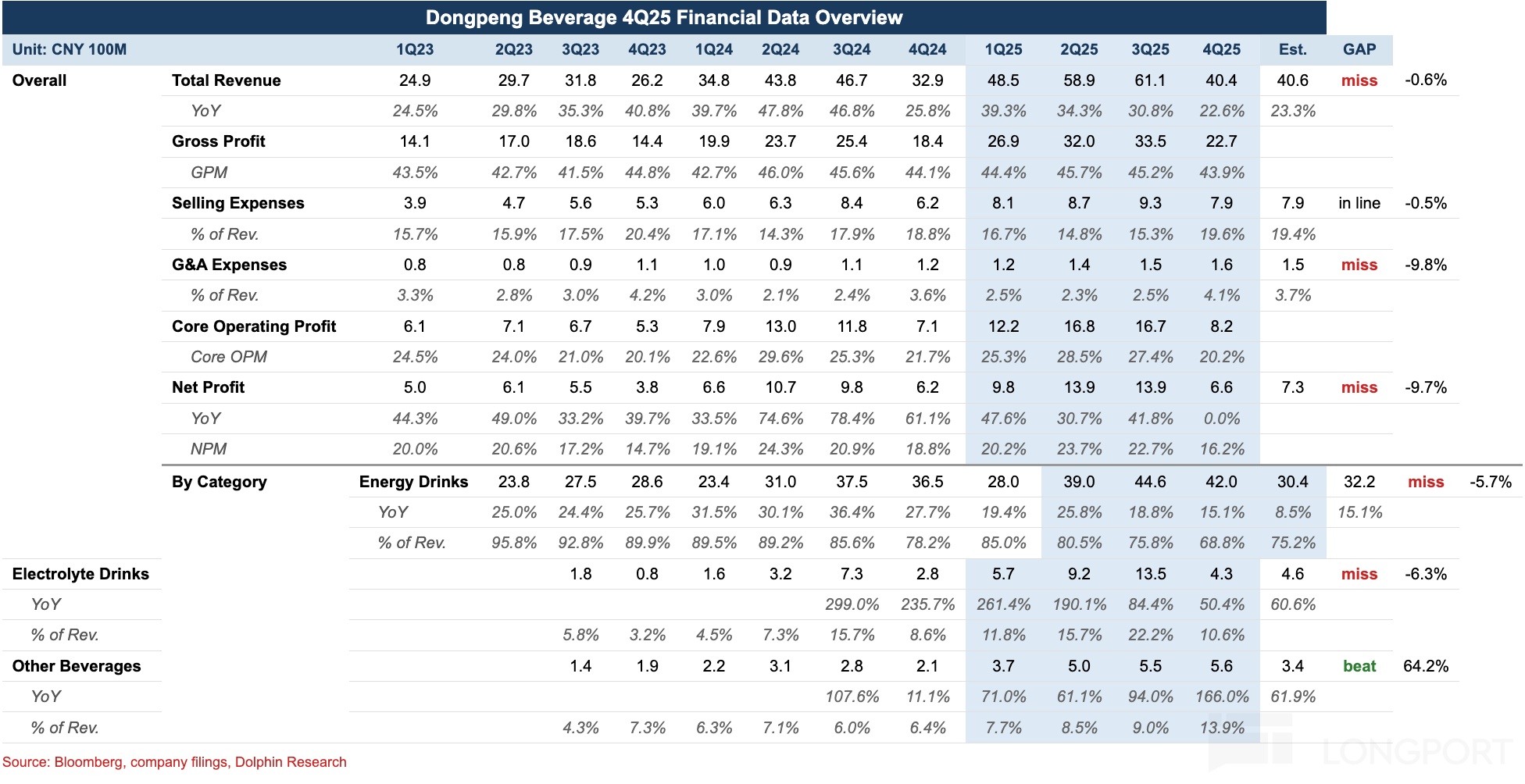

- Revenue growth kept slowing: In 4Q25, revenue reached RMB 4.04bn, up 22.6% YoY, but growth stepped down sequentially throughout the year starting in Q1.The core reason, as Dolphin Research has repeatedly emphasized, is that the flagship energy drink is hitting a growth ceiling while the 'second curve' is too small to backfill the slowdown, creating a growth gap.

- Energy drinks slowed to single-digit growth for the first time: By category, energy drinks delivered RMB 3.0bn revenue, up 8.5% YoY, a new quarterly low.Beyond natural deceleration, Dolphin Research believes the 4Q org restructuring and team ramp-up led the company to deliberately slow shipments. Electrolyte drinks posted RMB 430mn revenue, +50% YoY. It was not spectacular, but still met the RMB 3.0bn full-year sales target. The only upside surprise came from 'other beverages' at RMB 560mn, +166% YoY with sequential acceleration. Dolphin Research suspects products like Daka coffee and Fruit Tea are still in rapid channel rollout leveraging existing distribution.

- Home-base markets look saturated. By region, disclosure definitions changed (Guangdong was merged into South China), making comparisons tricky.Based on channel checks, the Guangxi–Guangdong area, where outlets are already highly mature, grew only in the low single digits. North China (Beijing–Tianjin–Hebei, Shandong–Henan) and West China (Sichuan–Chongqing, Northwest) still have much lower outlet density than the South, with penetration rising rapidly.

4) Higher spend in the near term; margin under pressure. On GPM, the mix shift toward lower-margin electrolyte water and other beverages dragged overall GPM down 20bps to 43.9%. On opex, the company stepped up cooler placements in 4Q, lifting the sales expense ratio by 50bps YoY, and management expenses also ticked up temporarily amid the 'five-war-zone' reorg. Core OP margin fell 150bps to 20.2%, below expectations.

5) Financial snapshot

Dolphin Research view:

Since the Q3 print, the stock has fallen over 25%. The core issue is that the results revealed a slowing base business in energy drinks, which had underpinned rapid growth in recent years, and other categories cannot yet fill the gap, triggering de-rating risk. The 4Q numbers further confirm this trend.

To address the growth dilemma, Dongpeng executed its largest-ever internal reorg in 4Q. In short, the former six biz. units under National Sales (Guangxi, Central China, East China, North China, Southwest, North) were carved out and, together with the Guangdong base, re-aggregated into five war zones by region: South, East, Central, North, and West China, reporting directly to HQ.

In Dolphin Research’s view, this marks a pivot from a single hero SKU-led, rough nationwide rollout to multi-category coordination and granular, region-led deep cultivation.

Versus the prior structure, two core changes stand out:

a) Greater financial and marketing decision rights for zone heads: Previously, provincial managers had limited authority, and major regional marketing activities, new product pushes, and channel spend required approval from National Sales or Shenzhen HQ, resulting in long decision cycles and slow market response.Under the five war zones, the company mapped regions by market size, consumption traits, and competition, and pushed down key decisions on HR, spending, and channel operations. Zones can now formulate and execute targeted marketing and ops strategies more quickly based on local competition, rival moves, and scenario differences.b) From energy drink-centric KPIs to full-portfolio KPIs: Instead of focusing on the single hero SKU, the five zones now run comprehensive KPIs across three lines: Dongpeng energy drink, 'Bushuilla' electrolyte water, and other new products. This is meant to shift teams from single-SKU drive to multi-category synergy and to accelerate the second and third growth curves.

Combining a) and b), Dongpeng is trying—under heavy growth pressure—to unleash frontline initiative by delegating authority and changing KPIs to break the single-SKU growth ceiling. It aims to leverage multi-category ops and new-consumption scenarios to broaden user reach, mine per-store and regional upside, and ultimately deepen nationwide penetration and deliver steady growth.

On valuation, assuming the reorg lifts per-outlet productivity, and 2026 sees +15% growth in energy drinks with electrolyte water and other beverages sustaining 50%+ growth off a low base, net profit of RMB 5.3bn in 2026 would imply ~24x. Against Dolphin Research’s 2026–2029 EPS CAGR est. of 21%, that still looks rich, so they prefer to wait for ~20x (~RMB 106bn mkt cap) for a better margin of safety.

Detailed earnings takeaways:

I. Revenue growth kept slowing

In 4Q25, Dongpeng posted revenue of RMB 4.04bn (+22.6% YoY) with sequential step-down since Q1.The key issue remains that the energy drink is hitting a growth bottleneck while the small 'second curve' cannot offset the slowdown, creating an interim gap.

II. Energy drink growth fell to single digits

By category, 4Q25 energy drink revenue was RMB 3.04bn, +8.5% YoY, another quarterly low.Beyond natural deceleration, Dolphin Research thinks the 4Q org reshuffle and team ramp-up led Dongpeng to slow shipment cadence.

On innovation, the 2025 launch of sugar-free Dongpeng (with L-α-glycerophosphorylcholine) successfully tapped health-conscious office and fitness use cases, broadening the energy drink consumer base.It also fits emerging venues such as gyms, e-sports centers, and co-working spaces. Overall, channel checks suggest sugar-free variants are growing meaningfully faster than the overall energy drink category.

Turning to the much-watched 'second curve' of electrolyte water, 4Q25 revenue reached RMB 430mn (+50.4% YoY).While not eye-popping, it still achieved the RMB 3.0bn full-year target.

Beyond incremental channel gains from outlet expansion, 'Bushuilla' growth relies more on scenario expansion and pack-size tailoring to different use cases:

Strategically, the positioning shifted from professional sports hydration to a high-frequency daily hydration drink.

For outdoor manual workers, Dongpeng deepened partnerships with Meituan, Ele.me, SF Express, and JD Logistics in 4Q, adding dedicated displays and coolers at depots. It also added more vending machines in ride-hailing driver charging/rest areas to cover the 'last 100 meters' more effectively.

For office workers, the company installed 20,000 office-building coolers with co-displays of energy drinks and small 'Bushuilla' packs labeled as 'workstation energy replenishment stations,' improving conversion.

For students, Dongpeng set up 'exam prep energy stations' at grad-exam sites and campus business districts. Through check-in interactions (QR code coupons, free trials) and give-away packs (energy drink + 'Bushuilla' + study materials), it targeted high-frequency mental-exertion scenarios while building private traffic and brand equity.

Though the company did not disclose specifics, channel checks indicate 380ml 'small hydration' is growing much faster than 555ml and 1L.This reflects incremental demand from daily-use scenarios.

Other beverages delivered RMB 560mn revenue, +166% YoY with sequential acceleration, beating expectations. A recent move: nationwide rollout of 500ml fruit tea began in Dec. Based on checks, by Dec it had reached 200–300k outlets, but sell-through was slower than the initial 1L launch, likely because consumers have built a strong value-for-money perception around large bottles.

III. Home-base markets reaching saturation

By region, disclosure changes merged Guangdong into South China, complicating comparisons.Dolphin Research’s checks suggest Guangxi–Guangdong achieved only low-single-digit growth with highly mature outlet coverage, while North China (Beijing–Tianjin–Hebei, Shandong–Henan) and West China (Sichuan–Chongqing, Northwest) are still in a rapid penetration phase given much lower outlet density.

Overseas, Dongpeng struck a deep partnership with Indonesia’s Salim Group in 4Q and formed a JV in Indonesia.This marks a shift from simply 'shipping' to distributors to local production and sales, which looks promising.

Finally, distributor counts fell in South and East China during the year.That suggests Dongpeng has moved past the distributor-led land-grab stage and now prioritizes distributor quality. Based on checks, the company is actively pruning distributors across regions, which should lift per-distributor productivity over time.

- Near-term spend up; margins under pressure

On GPM, the ramp of lower-margin electrolyte water and other beverages trimmed GPM by 20bps to 43.9%. On expenses, cooler deployment increased in 4Q and, based on checks post-reorg, Dongpeng raised sales staff compensation; sales expenses rose 27% YoY and the sales ratio increased 80bps to 19.6%.Management expense also rose temporarily amid the 'five-war-zone' reorg, up 50bps to 4.1%. Core OP margin fell 150bps to 20.2%, missing expectations.

<End here>

Dolphin Research past articles:

Deep dives:

Sep 23, 2025: Dongpeng Beverage: How did the local 'life elixir' beat Red Bull and Monster?

Oct 10, 2025: Dongpeng Beverage: What is the next RMB 10bn playbook after energy drinks?

Earnings notes:

Oct 24, 2025: Dongpeng Beverage: Energy drink slowdown, can the myth hold?

Risk disclosure and disclaimer: Dolphin Research Disclaimer & General Disclosures

The copyright of this article belongs to the original author/organization.

The views expressed herein are solely those of the author and do not reflect the stance of the platform. The content is intended for investment reference purposes only and shall not be considered as investment advice. Please contact us if you have any questions or suggestions regarding the content services provided by the platform.